Why this matters: Real estate agents and brokers in 2026 are observing another year of substandard home sales volume following the 2021 pandemic buying frenzy. Even as FRM rates dropped over 80 percentage points in 2025, additional buyers did not come forward. Meanwhile, inventories of property for sale grew, and will eventually build up with a vengeance.

Homes for sale meet depleted buyers

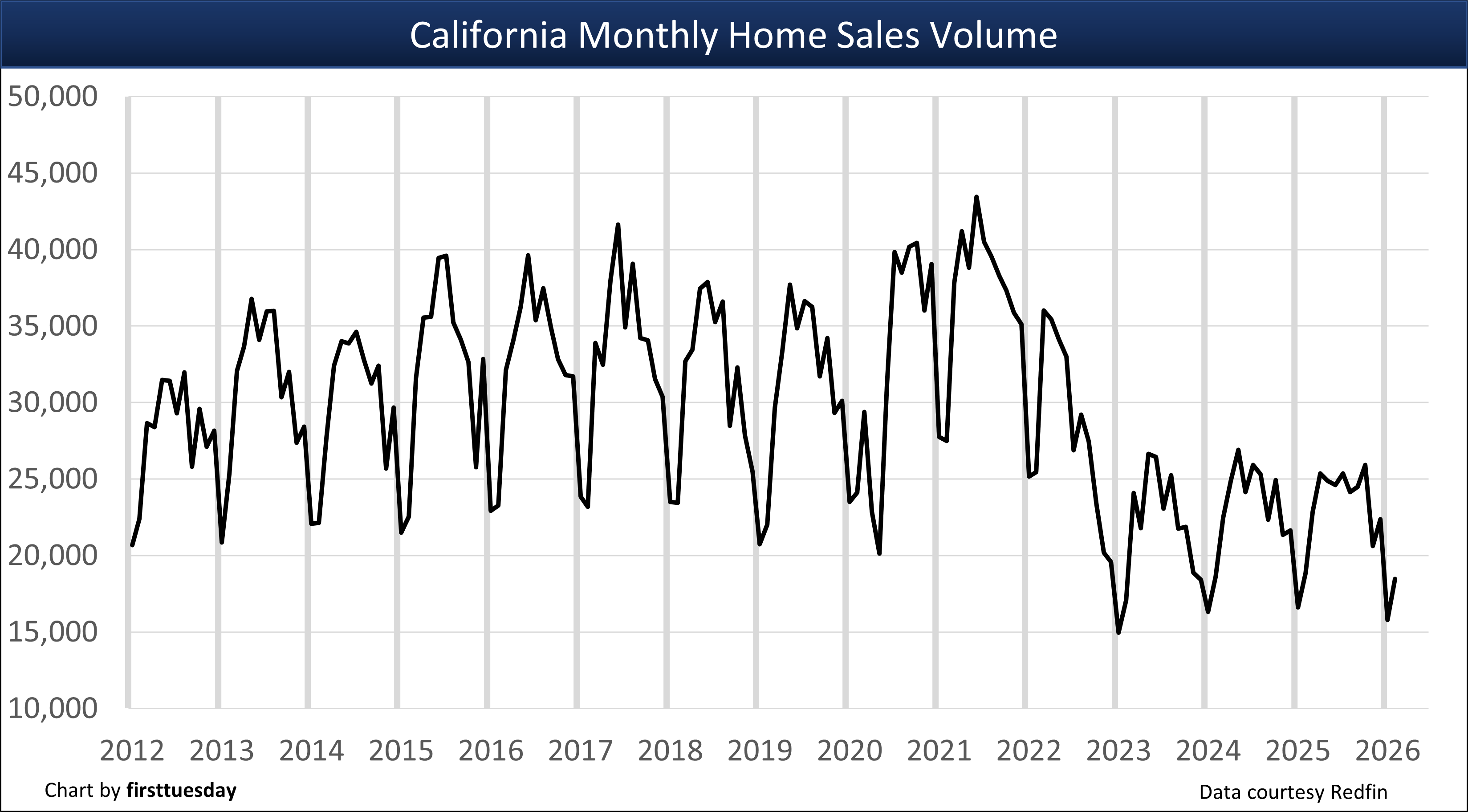

In February 2026, California saw 18,500 escrows close for new and resale home transactions. Sales volume in February dropped 1.9% below the same month one year earlier.

Importantly for trends, year-to-date (YTD) sales volume through February 2026 decreased 3.3% from the 2025 YTD sales figure. This starts off a fourth year of flat to weak sales volume, with aggressive consumer inflation and static property prices insufficient to attract more buyers – and now a war-borne rigor mortis freezing turnover.

Recent home sales trends

Consider that annual home sales experienced literally no change from 2024 to 2025. More critically, sales volume in 2025 matched 2024 at 27% below 2019 — the last year in the pre-pandemic sales cycle.

Today, buyers wait until they sense the decline in pricing has passed, evidenced when prices bottom and begin to rise. Be aware your typical homebuyer today knows their math for income-to-mortgage leveraging to set home pricing, thanks to readily available insight.

The developing public uncertainty about political upheaval, trade taxes and immigration hostilities — and now a war — tamps down owner and tenant turnover, and thus sales volume. The property sales volume will suffer from this status quo type rigor mortis until speculators turn to the real estate market and stop prices from dropping.

Sales volume strikes at pricing

Watch for home sales volume to trail off during 2026, as the likely trend of another disappointing spring season results from buyer caution around increasingly troubling employment conditions. More changes are underway. The U.S. is shifting into an economy not unlike the mid-1960s and mid-1980s stemming from a heightened focus on resetting the military-industrial complex for a war economy which instantly suppresses user turnover.

When home prices decline across all pricing tiers, not just the high tier now underway, recent homeowners with little down payment can only watch as the equity in their home slides underwater. This price-to-mortgage crossover event is not likely to begin until a nationwide economic recession brings on a further drop in the number of Californians employed. Also, keep an eye on the slow upward trend currently underway with mortgage foreclosures, a force compelling owners to sell.

Sales agents can expect the current real estate recession to eventually bring about a return of real estate speculators after prices drop to produce a “dead cat” bounce in both sales volume and pricing. Within 12 months following the speculator-driven market bounce, home prices historically slip as homebuyers wait and watch as prices bottom during that period. It is then that a sustainable sales volume and pricing recovery takes over with the return of end-user homebuyers — and temporarily lower mortgage rates for lack of investment opportunities.

Updated April 2026.

Chart 1

Chart update 4/2/26

Feb 2026 | Feb 2025 | YoY change | |

| California home sales volume | 18,500 | 18,800 | -1.9% |

Home sales fluctuate from month to month for a variety of reasons, all worth an agent taking time to consider. The most significant reason is the volatility of homebuyer demand. Several factors constantly at work moving the California homebuying market include:

- seasonal motivational differences, an annual cycle producing the spring bounce [see Chart 2];

- job market fluctuation;

- mortgage interest rate movement;

- homebuyer saving rates;

- home pricing sought by sellers;

- turnover rates for tenants and owners;

- negative equity property financials; and

- investor and speculator opportunity perceptions.

Seasonal differences in annual sales volume

It’s normal for home sales volume to rise in the first half of the year and fall after peaking around June.

Chart 2

Chart 2 shows average home sales volume experienced from 2011-2018, the recovery period following the Great Recession. As depicted, the month with the most homes sold monthly during the year close escrow in June. Another upturn takes place in December, as homebuyers seek to wrap up their financial activities before the end of the year.

Real estate agents need not fuss when they hear of falling month-to-month sales volume in the latter half of the year. It is the normal cycle of seasonal progression taking place. What to watch for is year-over sales, to compare recent months this year to the same months last year or compare another period such as year-to-date to best see a trend.

As a rule, current market activity, whether up or down, is reflected first in sales volume, followed in nine to 12 months by price adjustments in the same direction.

Chart 3

Chart update 1/26/26

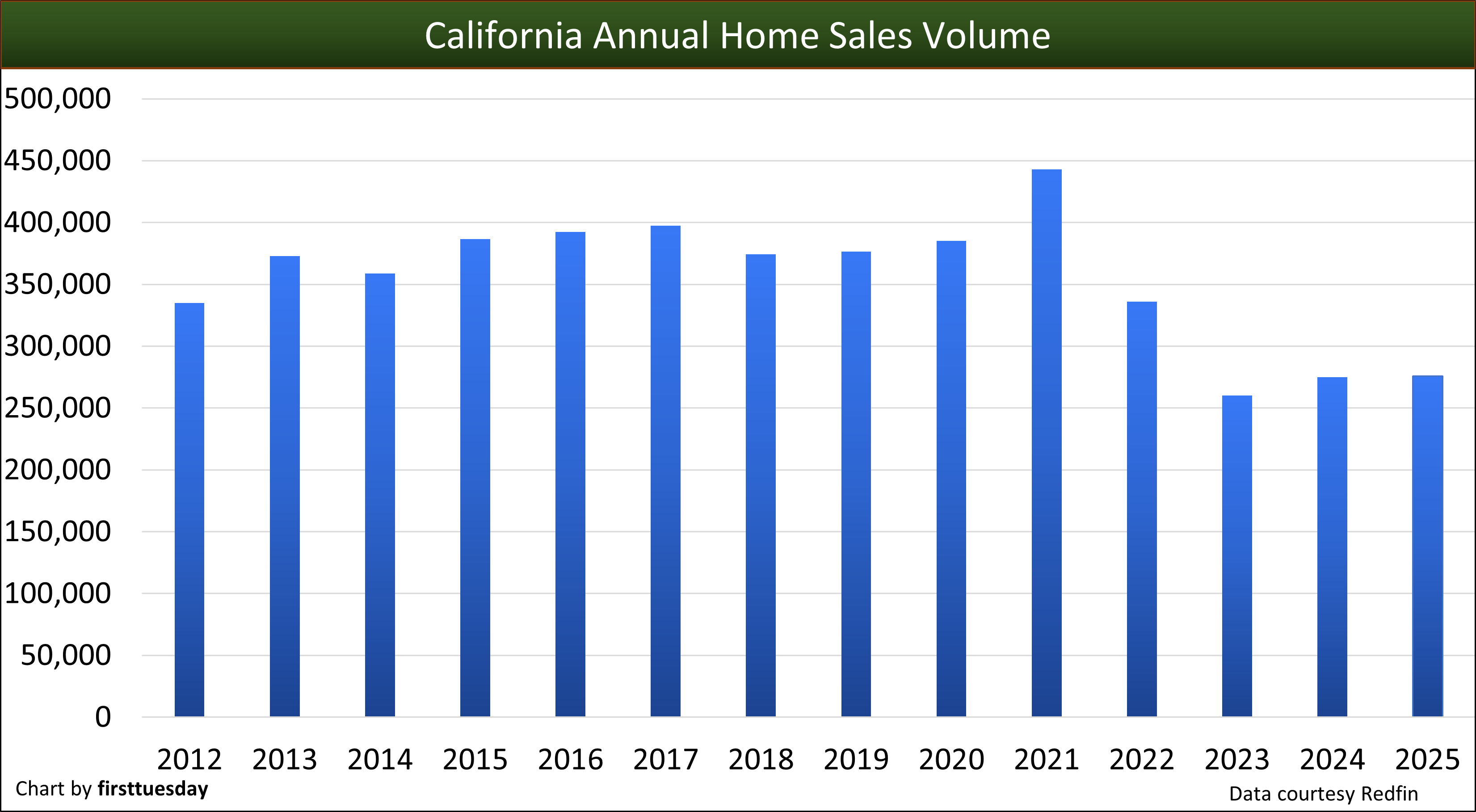

| 2025 | 2024 | 2023 | Annual change | |

| Annual home sales volume | 275,900 | 274,900 | 260,200 | +0.3% |

To set the stage for a forward look, a review of sales volume in the recent past is helpful:

- 2022 home sales volume peaked early in March and lost all ground gained in the pandemic year of 2021, ending the year 24% below 2021, but only 12% below 2019, the last “normal” year for home sales before the pandemic upended market dynamics;

- 2023 home sales volume lost a further 22% over the prior year, the consequence of buyers pulled forward to buy in 2021 using historically low mortgage rates for funding;

- 2024 home sales stabilized from the prior year, suggesting the end of the ripple effect from pandemic economics; and

- 2025 continued the stagnant sales trend of the prior two years.

Chart 4

Chart update 4/3/26

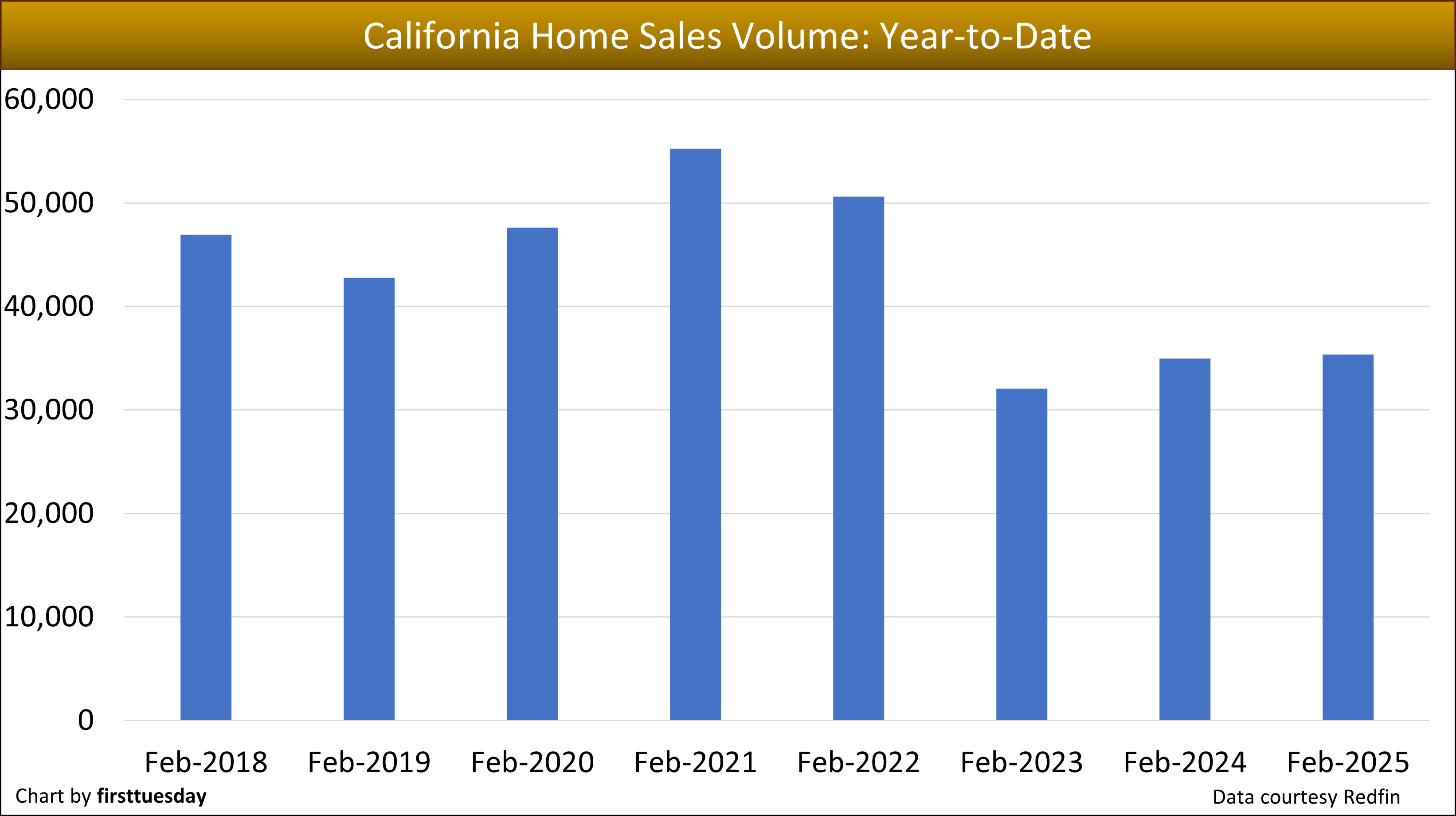

| Feb 2026 | Feb 2025 | Feb 2024 | |

| Home sales volume year-to-date | 34,400 | 35,400 | 34,900 |

Year-to-date (YTD) home sales volume through February 2026 was substantially the same as the year prior. As of February 2026, YTD home sales volume is 3.3% below a year earlier. Compared to 2019, home sales volume YTD is 20% lower in 2026 as of February. 2019 was the last “normal” year for property transactions before the pandemic economy took over. The present annual trend in sales volume is flat.

Home sales volume now in 2026 will remain weak as in 2025, due to:

- job uncertainty in the wake of federal shutdowns, the US-Iran War and a disjointed flat rate of job growth;

- high mortgage rates reducing homebuyer ability and willingness to pay seller asking prices;

- a consistent quantity of all-cash buyers undeterred by interest rates or asking prices;

- reluctance of sellers to reduce asking prices to offset high mortgage rates;

- buyer agent failure to advise buyers to disregard asking prices and make offers at prices they qualify to pay;

- a steadily increasing inventory of property available for sale across the state causing buyers to wait to make a selection; and

- the real estate recession, yet to be declared, but four years underway throughout California.

Home sales in the coming years

The forward trend in California home sales is one of caution and delay for both buyers and sellers. Homebuyer income is growing but only keeping up with inflation, much improved from the less-than-inflation pace during the decade preceding the pandemic.

While wage increases caught up with consumer inflation, they were nowhere near enough to catch up with pandemic-peak home prices and post pandemic mortgage rates. Home prices remain far above the mean price trendline but the gap is narrowing as property prices run flat and wages increase.

The necessary price adjustment required to bring buyers to the table will be especially resisted by sellers’ pricing stubbornness, known as the sticky pricing phenomenon. The likely result is continuing the post-2022 plateau of flat pricing that will meet up with the rise in the mean price trendline rather than prices dropping much in 2026.

firsttuesday forecasts annual home sales volume for 2026 will slip slightly from the level in 2025, as buyers continue to wait on the sidelines. The sales slump in 2026 will be the result of the tandem high levels of asking prices, mortgage rates and financial caution.

Sellers are also competing against the rising strain of buyers comparing the high monthly cost of ownership and lower, declining rent rates charged by landlords for similar housing — which reduces turnover and transactions.

The timeline for a real estate turnaround faces complications not experienced in recent decades. Government trade wars are raising the cost of both domestic and imported construction materials. Costs of owning real estate are compounded by the federal attack on the necessary migratory labor force for construction and maintenance of homes. And now another American war in the middle east.

The competitive broker

What’s a broker reliant on home sales to do until home sales volume provides abundance again?

SFR brokers and agents might consider adding transaction-related services to supplement their income in the present buyer’s market. Those who do add related services — provided only when the client signs a representation agreement — will restructure their practice as “all-service brokers.”

Transaction-related services originate primarily due to representing buyers, not sellers. When an office operation includes any of the services provided to buyers, their agents maintain a standard of living, remain solvent and position the office for eventual growth. Notary, anyone? MLO?

Related video:

{kind=link}

Thank you ft Journal for the California home sales volume statistics.

Realtors want you to think it’s all about supply and demand but it’s not. Over 75,000 homes in the bay area are already in pre forclosure stage. (Of course realtors don’t tell you this, as well as banks….. profit earnings) interest rates are also going up, healthcare costs going up as well as living in general. Sadly, people’s income is staying stagnant while everything else is in an upward trend. Also you need to realize that FHA loans cap out at $631k in California. Because the Feds don’t recognize California’s housing prices to be accurate at all. So they won’t lend more than the 631k threshold. We’re over 30-40% above the national average (way off balance) just like the made up valuations (pulled from thin air) of tech companies who sell nothing tangible…. the housing market is also smoke and mirrors. (Just got my MBA from Anderson @ UCLA and have been studying the market here for 2 years now)

I know you’re right. Why are the prices really so high?

Greedy Realtor-Builder-Banker Industrial Mobsters colluding and enslaving the nation.

REALTORS are the only culprits that property prices are going up, because we try to give the seller the highest gain ever. Why not stop and standardize prices?

Home buyers keep earning almost the same as 10 years ago.

So it’s happening with HOA’s collections now. How much will they pay in 20 more years?

The value of the houses are becoming unreachable for the community.

So expensive that there will be a terrible number of homes for sale without a chance of being sold.

Is there another big drop in the Real Estates market?

Hey Wokka i am trying to buy a house and i am already pre- approved but would it be smart to wait and see where the housing market goes?? Or you think is a good time to buy right now??

If you’re pre-approved, and you have a great rate locked in, I wouldn’t throw it away by waiting to see what happens with the market. Rates are going to rise, and when they do, you could end up qualifying for less than you are approved for now, if the rates go high enough.

You need to make a decision: If you think the housing market will keep going up for a little longer yet, then now would be a good time to buy, since it’ll be more expensive later. If you think a correction or even a crash is coming relatively soon, then waiting may be a good idea, but you will most likely get a much higher rate than you are approved for now, but you’ll be able to buy the same home, or better, with lower property values in play.

There’s no guarantee about which way the market will go in the near future.

If you want someone’s opinion, buy the house now if you can afford it.

Now is the best time to buy!

-NAR

Thanks so much for your input, I have been a lender for over 30 years and have been trying to time the market right to make smart investments. You are right Ca is over prized compared to national average but I believe we also have the big tech, movie, foreign money pouring in to say the least. Don’t forget out weather LOL. Anyways, what I have noticed being a lender is that these FHA loans that allows non occupying borrowers to help actual occupants qualify will be the first to have some type of financial hardship if they cant refi out of those high PMI payments. We have been getting a few calls for clients that are wanting to refinance but can’t because the market appreciation is slowing down. I am curious where you got the info about 75,000 homes in Pre-Foreclosure up in Northern Ca.? Good luck with your MBA, 1stInnovativefinance.com

Without taking into account that HOA have been increasing year by year.

Is there a California government office that will review HOA high fees? … Currently it is so expensive to buy a condomminium that payments are as high as buying a home.

Where will the poor people who live the heaviest and least paid jobs live?

Think about the next 20 years. Who can live in California and pay a mortgage without eating?

Great analysis. Right on. Most Bay area homes are really old and in case of any type of natural disasters, the cost of rebuilding is exorbitant.

Housing market in the Bay area is good for flippers, tech-rich investors and those who can sell it to other fools at the peak value.

Thank you for telling the truth. Really! I see whats going on myself. Don’t know if i should buy now.

Hey Wokka72,

I completely agree with your comment. I’m 34 yrs old and have been studying the trends of housing and how the economics of the Bay Area are. I feel like their is a bubble about to explode.( I call it the last hooraahh for the baby boomers to screw their kids).

Really? It’s called the free market for a reason. If people are willing to pay such high prices, then that’s the valuation. I have a Masters degree too, but way more market/business experience so I’m sorry but I don’t agree with you.

I am looking into purchasing my first home. My husband and I make about $130k a year combined and we are tired of paying over $2k a month on rent. We live in the Bay Area. We are a family of 4 plus my mother would move in with us and would financially contribute. Is it a good time to buy? Because people keep convincing me otherwise.

Thanks

Alex, If you are confident you can stay in the home for at least 10 years, it will be a good decision for you… even if we are at a peak and we have another decline. Rents always go up. Houses rented for $600 a month 30 years ago are renting for $3,000 a month today. The $2k rent you are paying today will be $6K 30 years from now… possibly higher. If you want to retire some day you just have to own your own home.

Or invest that money in some low fee stock indexes. The rate of return has been higher historically (even adjusting for inflation).

It’s a good idea to buy in areas that offer larger homes for lower prices. The Bay Area has higher end prices, and you get smaller and older built properties for your hard earned income. Price per s.f. is extremely high in those cases. Get more for your dollar, which is usually not so close to the center of Metropolitan Cities.

Yes – you are losing money every year due to constant increase in asking prices. You will be chasing the market, and have to keep saving to meet the down payment percentage your lender requires. If you are a first time buyer, some lenders have a 3% down conventional loan. Avoid FHA if you can, because Sellers place your file at the bottom of the heap. It’s a Seller’s market, which means we are receiving multiple offers and high down payment offers. Broker: vickismithbkr@msn.com

* CAll Me, I can help. :)

Yep. prices have been going up without any real support, but I think the election is slowing sales at this time. Many homes have been on the market in my area for the last 3 months, when most sold quickly in the first half of the year – just wait until December depending upon who wins!!

Question to the Author or any one else who wants to answer . First Thanks for the well written, and researched article. I am thinking about upgrading the size of my home I bought at rock bottom. I do not want to pay capital gains tax on the next house and am already watching my next moves housing market which i predict in 3years. Do are you confident this market will hold till 2019 ? I believe 3 years is the capital gain #?

I apologize for not editing this correctly

As long as you stay in the house owner/occupied for 2 out of 5 years (does not need to be back to back) you will not pay any capital gains.

Thanks for the update for 2016, these figures are pretty much what I tough they will be

Very well written and received. Much appreciated… finally, meat and potatoes I can digest. Thank you!

Century 21 is taking the approach of herding prospects into a large room and closing the sale before they leave. The postcards they are mass mailing talk about renting / buying and give the impression they are being aggressive about getting loans approved at low interst rates.

The prices are at the top again and no one can afford to buy or rent. We are clearly at the top and the bubble is going to have to burst AGAIN. It’s a cycle – we were here with houses 5-6 yrs ago, everyone was in foreclosure and now those houses are selling for 40-60% of their value 5 yrs ago. It’s insane and can’t be sustained. People making 6 figure+ incomes can’t afford to buy or rent. Something has to give – oh and the stock market bubble has burst so it’s going down. Don’t buy now – wait – the rental market will have to give as well because no one can afford the outrageous rents

I totally agree with you, first time home buyers will never be able to afford to buy with this market.

Not true. People making 6 figures can afford to buy, they just have to scale down their living. Peoples first home should be a modest home and grow from there. In the 1950s and 1970s people were happy and thinking they were living in luxury in a 1,000 square foot house. I make just under 100k and I am purchasing my sixth single family rental homes in one of the most expensive zip codes in Northern California as rentals in the past 2 years. It’s pretty easy to save and sweat some equity out with the rents. I drive an older car and buy my clothes on eBay, but heck, I have an excellent real estate portfolio and make high rents, because my places are clean and modern. And I spend a lot time working with contractors, accounting and working with my tenants. I am very hands on.

My husband makes over $100,000 a year and we are scraping by , maybe because you have rentals but sorry you have to make more then $100,000 to buy a home in CA. We live in San Diego and it’s outrageous. $400,000 gets you a ran down home in bad areas and under 1,000 square foot.

im 27yr old. and i make only $2600 a month. and i just bought my house at 2016 July for $225000 1200sqft house build 1970.house in very good condition . put down $20000. and im living in sacramento of CA. i just want to pass a message out…its not that difficult to own a house. u just need to watch your monthly spend, control it tight for 2 years. you will be good.

Nicole, I make half of what your husband makes, and I’m sitting in my 4bedroom/2 bath/1304 sq ft house that I purchased in 2009 for $179k. It’s far from a dump, and it’s clearly over 1,000 sq ft.I live in Suisun, in the North Bay, where people live and commute to SF, raising house prices here. Let go of the “woe is me, we make $100k and can’t buy a house because you “have to make more than 100k”. No you do not. You might need to lower your standards or move somewhere else in Ca, because houses in my city are selling for $370, or newer homes in the $400&500k range. I refuse to pay $365k for a home that sold for half that in 2009-2012, but they are out there for sale, and at $1700-1800 a month, including taxes,insurance, p&i, that’s LESS than rent out here.

Kelly, I apologize, but you have no idea what you are talking about. You cannot compare your geographic area to that of Nicole. I also live in San Diego, and this is in fact the case here. My 900 sq. ft., 1bedroom/1 bathroom apartment is $2,350/month. When I first started renting here 3 years ago, it was $1,630.

I recently got married, and have been searching for a home. The prices are absolutely outrageous here. If you want to live in any decent area, you need to spend $700,000+ for anything remotely nice. My business partner lives in a so-so area. His house is 2 bedroom/2 bathroom, and is around 1,500 sq. ft. He bought it 5 years ago for $400,000. It is now valued at $750,000.

Kelly, I live in Suisun City. It’s on it’s way up, back in 2009 I was just starting college and jobs were scarce. It’s going to get ridiculous for us who are just getting our first decent jobs to buy anything. Now the same homes folks purchased in 2009 are selling 400k and up.

I certainly cannot move to Sacramento, it would make my daily commute 4 to 6 hours long. We aren’t going to get anywhere either if everyone’s commuting at this rate my commute just gets worse every year as people move further inland. Let’s not forget employers are only giving a $0.50 raise or so each year if that, and that’s to folks with college degrees.

In Solano County, Zillow say we should expect housing costs to increase more than the rest of the bay area, I wonder why.

That’s how we do it too!

It is indeed insane. I saw a tiny condo that sold in 2012 for less than 100K in 2016 priced at 279,000. Yes someone bought it. The realtor said the prices higher are based upon high rents. No one can afford to buy or rent these days. A 2k month apt they are asking for 60k income. It is crazy. Something has to give. The powers that be are realizing that not everyone can even rent an apartment for they are asking you earn too much money, even if you are to rent for 3 months. They are trying to say we are not in a bubble, this is what is scary. Maybe it is simple demand, based upon the out of control immigration to this country….?

Immigration is a topic rarely discussed! The only way the state is increasing in population is due to immigration which fuels demand! Awesome points!

Awesome points! Immigration has a large factor in population and prices!

You’re right Michelle,

At this step we return again to 2002-2006 and we will make money again for 5 years and then we will starve the next 5.

REALTORS we must stop selling every day more expensive, because buyers are not making more money.

You’re right Michelle,

At this step we return again to 2002-2006 and we will make money again for 5 years and then we will starve the next 5.

REALTORS we must stop selling every day more expensive, because buyers are not making more money.

I agree with this statement. I’ve watched the market in California my whole life, and it’s definitely due to drop. It’s way over priced, and I really don’t see it going higher. It’s been rising and dropping every 10 years, and we’re right there again from 2008. I’m waiting to purchase, and feel like it would be very risky to purchase now.

Patti-I read we’re not actually at 2008 prices yet. I believe we’re in a bubble,and I’m TIRED of hearing “No Bubble, Simply low supply, high demand”. I purchased my home in 2009 for $179k, after it was foreclosed on someone who paid $399k in 2008. It was a dump in 2008, flipped in 2009, and I paid half of the 2008 price. Right now my house is “worth” $370, so we’re about $30k shy of 2008. Please do NOT purchase now. I’m not a realtor or expert of any kind. Just someone who in 2005,2006 said”I’ll never be able to buy a house here”, the watched the bottom drop out and was able to purchase a very affordable home. New roof, new heat&ac, new fence around the back yard, new sod and shrubs, new stoveµwave, new paint, carpet and dual pane windows. I literally can’t afford to rent. My mortgage is $1,000 a month. It was $863, but I rolled my Solar Panel loan into the mortgage, so when I decided to sell, there wouldn’t be a lien on the house. If I purchased today, I’d pay 50%more than I did in 2009, and I’d get 300 less sq ft, and 2 less bedrooms. Also, nothing new like windows, roof, etc, and no Solar Panels. I like to look at houses for sale on Zillow, because you can scroll down to the Pricing/Tax information, and it will show the previous sale dates and prices for the house. It truly makes you think”Do I want to pay $50% MORE for this house, that hasn’t been updated since it sold 5-7 years ago for half of what they’re asking? If I sold today and took my $145k in equity, I’d have to put most of it down on a “new” house, my payment would increase $500-$600 a month, my property taxes would double, and I’d be in a smaller,less nice house. I remember 2008 like it was yesterday. My credit card limits being cut to the balance because”I live in a high foreclosure area”. Not because I was in foreclosure lol. I was a renter. I believe “What goes up, must come down”. I don’t think rent prices will come down though, only homes. When the last bubble burst, rents increased because everyone who lost a home needed a place to stay. The apt I rented in 2009 rented for $825. Today it rents for $1695. NO IMPROVEMENTS MADE TO IT.They raised the rent by $100 a month yearly, and this year it seems it was raised twice. I don’t even want to own any longer, because of my neighbors and maintenance, but I can’t afford to rent and pay double my mortgage for a 2 bed apt. Good Luck :-)

What about getting a proposition passed banning foreign investors from purchasing residential real estate in California???? Austrailia and Norway are already doing so. Given the limited amount of housing the Bay Area has, I think this would be an excellent solution. Why are we selling the American dream of owning a home to foreign investors!? Would anyone vote for this ban???

I agree, but I just don’t know how much they impact this frenzy…I think it’s more in the tech over valuation. Once the stock cools down, it should bounce back.

Absolutely! It would take a LONG time to pass this type of legislation but if people in California push for it, it becomes possible! It’s got my vote anyway.

I agree but also disagree. Americans have purchased homes as well outside the US causing this effect in other countries. To me the root of the problem is we do not educate thus employ our own working force; depending on outside workers. One solution might be to add a foreign property tax to this ownership and spend the extra tax on college scholarships.

There should be a ban. When the last bubble burst, you heard about foreign investors, esp Chinese buying up just to buy, and the properties would then sit. If feels like we are being taken advantage of… I will just have to vote for the candidate who gets it.

Great friggen idea!!!!! Finally someone who gets it!

Typical California attitude. Believing that jobs are increasing. Did you even look at the jobs report they are all crappy jobs flooding the market and all the good jobs are leaving

Is it true you could buy a home if your credit is around 610. I have proof of rent for the last 3 years at 2600a month

Yes, with an FHA Loan

Tony

If you truly wish to purchase… there is a way… $2600 a month can buy you a decent home in a decent neighborhood with a realistic attitude.