This form is used by an agent or broker when analyzing the income and expenses they are likely to experience while employed by a broker, to estimate their entry or change-of-office costs and their anticipated annual gross income and expenses resulting from the employment.

Finding the talent you need

As a broker operating an office employing sales agents and broker-associates, your success depends in large part on the quality of the individuals you employ.

The path you take to recruit agents you employ in your brokerage office depends on your business model. Some brokers hire as many agents as they can squeeze into cubbies in their office. For them, it is a numbers game for blanketing the real estate markets, an MO sometime called a media broker. Others recruit only those agents and broker-associates with track records that exceed typical production standards. Still others focus on a niche market employing only licensees who practice in that sector.

But before you create a plan for hiring agents/broker-associates, your recruiting goal needs to be set. Only then can you plan just where you are going to find talent — and how you will solicit it.

To set recruitment goals, you need to decide:

- how many agents you want to hire;

- the personal qualities you are looking for in an agent;

- what categories of individuals are you going to solicit, such as:

- pre-licensed prospects;

- inactive licensees;

- newly licensed agents; or

- experienced agents; and

- how much time and staff you will commit to training and supervising these agents.

These different types of prospective hires have varying needs and skill levels. Thus, the time you are willing to commit to necessary training and supervision may well determine who you will focus your recruiting efforts on.

Meritocratic pre-screening for potential hires

Once you’ve located potential hires, they need to be vetted to gauge their individual potential. Before calling for an interview, fundamental information about the prospect is gathered to determine whether a face-to-face interview is merited.

To gather information, a broker hands prospective hires the Agent Interview Sheet published by RPI (Realty Publications, Inc.). The prospect prepares and submits it to the broker, providing the broker with information about the prospective employee. Before conducting a personal interview, the broker reviews the information contained in the interview sheet. [See RPI Form 500]

The form asks the prospect to enter information about their background, education and real estate-related activities. When they fill it out and return it, their conduct indicates they are legitimately interested in being hired. [See RPI Form 500]

The Agent Interview Sheet collects personal information on the prospect’s:

- real estate license status and background, including:

- California Department of Real Estate (DRE) license number and the date it was obtained [See RPI Form 500 §1.1];

- other professional licenses or endorsements they hold [See RPI Form 500 §1.2];

- any negative actions taken against the licensee or the existence of a criminal record [See RPI Form 500 §§1.3-1.5];

- professional affiliations [See RPI Form 500 §2];

- educational levels attained [See RPI Form 500 §3];

- real estate activity, including:

- real estate, mortgage or business opportunities the prospect has an interest in [See RPI Form 500 §4.1];

- a description of the types of real estate services previously rendered by the prospect [See RPI Form 500 §4.2];

- the identity of former brokers who employed the prospect, and the duration of those employments [See RPI Form 500 §4.3];

- a description of the real estate clientele the prospect has previously and presently worked with; and

- the reason the prospect wants to be employed with your brokerage;

- personal contacts of the prospect and the identification of unrelated individuals who may serve as a character reference for the prospect [See RPI Form 500 §5]; and

- conditions of employment, including:

- the prospect’s commitment to pay dues and fees to professional organizations designated by you[See RPI Form 500 §6];

- whether the prospect will be employed on a full-time or part-time basis [See RPI Form 500 §6.2];

- the prospect’s commitment to abide by the provisions of the attached employment agreement, if hired [See RPI Form 505and 506];

- the requirement that the broker be named as an additional insured by the prospect’s auto-insurance carrier; and

- when the prospect will be available to start work for you.

In the interview, discuss your observations about the information the prospect entered on this sheet in conjunction with the terms of employment set forth in the Broker-Agent Employee Agreement with your prospective hire. [See RPI Form 505 and 506]

Eventually, you need to discuss their personal finances and how their income under your employ fits into their cost-of-living picture. This discussion is critical to their long-term employment at your office. [See RPI Form 504]

Ask questions that will help you determine whether their characteristics are in line with the objectives you have set for the type of agent or broker-associate you seek to hire. Specifically, ask why they think they will be a good fit in your real estate brokerage operation.

The discussion allows both you and your prospective hire to make an informed decision about whether they will thrive at your brokerage.

Realistic financial expectations — set accurately and early

After a prospect has been pre-screened using the Agent Interview Sheet and a formal interview has been conducted, you and the prospect then need to establish the sales goals to be met for the first year of employment.

Potential hires often have unrealistic expectations about their production and earnings as an agent with a brokerage firm. A written presentation of expectations enables them to have a clearer insight into what income to anticipate when representing your company. This high degree of personalized data bonds the prospect to you — incentivizing them to hire on with your brokerage versus seeking employment elsewhere.

A potential hire needs to understand what their anticipated annual gross earning, expenses and net income will likely be during their first year as an agent employed under your license. Without an upfront analysis, an agent will only be guesstimating the annual net earnings they will likely earn with your brokerage.

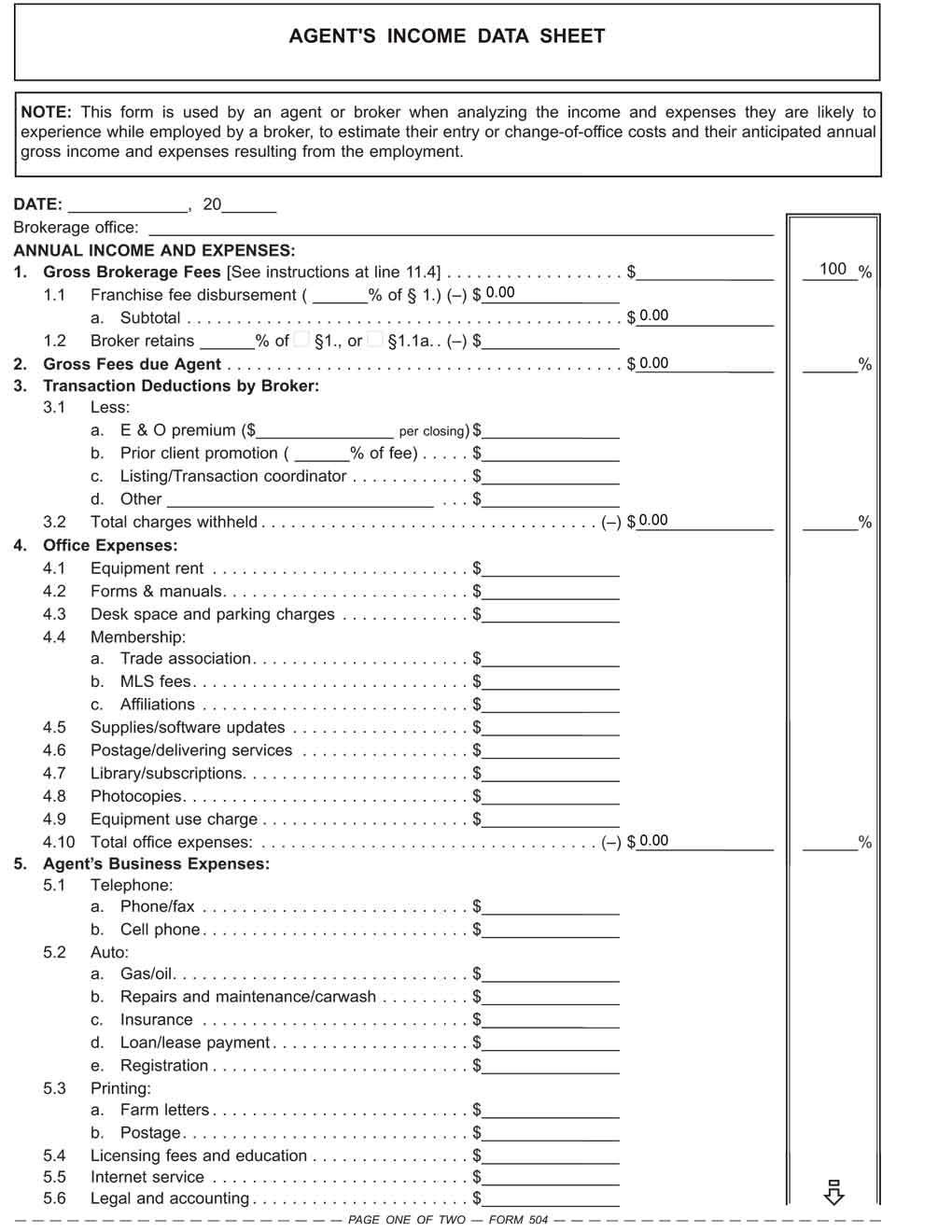

Employing brokers use the Agent’s Income Data Sheet published by RPI to present and help with the analysis of the income and expenses a potential hire is likely to experience while employed by the broker. Further, it is used to estimate the prospect’s entry or change-of-office costs and their anticipated annual gross income and expenses resulting from the new employment. [See RPI Form 504];

Costs and expenses a potential hire can expect to incur in their first year of employment as a real estate agent include such items as:

- gross fees they will receive from you as their broker [See RPI Form 504 §2];

- transaction deductions taken by you from their gross fees [See RPI Form 504 §3];

- office expense contributions they need to pay from their gross fees (equipment rentals, membership fees, library/subscription charges, etc.) [See RPI Form 504 §4];

- business expenses they will incur acting as an agent (auto, licensing fees and education, travel, insurance, etc.) [See RPI Form 504 §5]; and

- other marketing and sales expenses not covered by you as their employing broker. [See RPI Form 504 §6]

The likely gross fees the prospect will receive and the fee split charges are entered on the worksheet as part of the interview process. [See RPI Form 504 §§1 and 2]

Ultimately, the sales goal set between you and the potential hire is reflected in the amount of after-tax income the prospect seeks. [See RPI Form 504 §11]

Broker as the source of information

You, as the broker, are best able to anticipate the income and expenses a potential hire will incur. It is the broker — not the prospect — who is best able to draw a conclusion about a prospect’s future with your office.

Your primary objective when hiring an agent is to increase the gross broker fees received by the office without a disproportionate increase in operating expenses. Your full disclosure — upfront and prior to employment — about a prospect’s likely income and expenses leads to realistic expectations of income for both you and the prospect, arrived at mutually.

To be ready for an interview with a prospective agent, a proactive broker prepares an income data sheet by estimating the expenses a new hire will most likely incur. Also, the broker will estimate the initial cash investment a potential hire will be required to make to cover one-time, nonrecurring expenditures. Further, a potential hire will need to budget for cash reserves to cover personal carrying costs for a period of time necessary to produce closings and generate fees sufficient to sustain their standard of living without further resort to savings. [See RPI Form 504 §10]

Once the operating expenses, nonrecurring costs and carrying costs to be incurred have been established — based on your history with other similar agents you employ — there remains the difficult task of anticipating a potential hire’s gross fees from sales that will most likely close during the first year of employment.

Only you can estimate future fees

A new hire will not alone be able to accurately estimate the gross fees they will initially generate in your brokerage. Here, your first-hand experience is necessary.

A couple of approaches for estimating future fees are apparent. For one, you may project a range of gross broker fee amounts, varying from the earnings generated by a high producer to those of a low producer during their first year with the office.

Until the potential hire has been on the job working as an agent for you, you will not know at what level they can produce income. However, you can give the prospect a range of income earned from that of the weaker to that of stronger producers.

The various gross broker fee projections — ranging from low, medium to high — may be entered on separate copies of the income and expense worksheet. Thus, the prospect’s after-tax income can be calculated based on various levels of sales. [See RPI Form 504 §8]

An agent’s analytical use of the data sheet

A newly licensed agent can also independently use the data sheet for similar analytical and financial-planning purposes.

Before they look for an employing broker, they really need to set their own goal for the annual income they want to earn.

The volume of real estate sales they close during their first year in the business is essentially a “numbers game.” New agents will soon discover that only a fraction of all sales efforts come to fruition in the form of fees received from closings. Thus, to be successful, agents need an innate curiosity and the enthusiasm for estimating and forecasting income and expenses.

When an agent becomes discouraged or daunted by the exercise of completing the worksheet, they are not a prime candidate for employment in your office.

Setting realistic goals is the result of forethought and analysis with the addition of first-hand input from you — the broker who may employ them. Goals are known, quantifiable personal objectives. They are not to be left to somehow evolve after an agent starts work. Once set, goals are what an agent expects of themselves, and of you.

To figure out how much they will most likely earn in a particular aspect of real estate transactions – sales, type of property (SFRs, commercial, apartments), leasing or mortgage originations – potential hires often ask:

- What is the dollar range of the sales (leases and mortgages) I will work with?

- How many sales (leases or mortgages) will I likely close in my first year?

- What cash reserves will I need before my first transactions close?

- What business equipment and supplies will I need to provide?

- Is the model of my car sufficient for showing properties?

All this data, and more, is contained in the income sheet

To eliminate financial misunderstandings, brokers review the contents of the Agent’s Income Data sheet with prospective hires. When the prospects understand and demonstrate an awareness of the anticipated costs and expenses they will incur during their first year of employment with your company, they are more likely to succeed as an employee. [See RPI Form 504]

Editor’s note — An experienced agent also uses the income worksheet on their current operating conditions when either seeking to renegotiate their current employment arrangement with their existing broker, or before moving to another broker’s office. [See RPI Form 504]

Armed with the data on the worksheet, an agent is able to intelligently renegotiate fee splits and the allocation of expenses with their present employing broker, or competitively shop for another broker.

Document identification:

Editor’s note — Check and enter items throughout the agreement in each provision with boxes and blanks.

Date: Enter the date the agent’s income data sheet is prepared.

Brokerage office: Enter the name of the brokerage office and the branch location which is the subject of this income and expense review.

Annual income and expenses:

1. Gross brokerage fees: Enter the dollar amount of the fees it is estimated the broker will receive and share with the agent.

Editor’s note — To set the amount of the gross brokerage fees, see section 11.4.

1.1 Franchise fee: Enter the percentage figure and the dollar amount of the gross brokerage fees due a franchisor by the employing broker.

a. Subtotal: Enter the dollar amount remaining after deducting the franchise fee (section 1.1) from the gross brokerage fees (section 1).

1.2 Broker’s share of fee: Enter the percentage figure and check the appropriate box to indicate whether the percentage due the broker is taken from the gross brokerage fees at section 1 or from the subtotal remaining at section 1.1a after first deducting the franchisor’s fee. Enter the dollar amount the broker will retain.

2. Gross fees due agent: Enter the dollar amount remaining after deducting the amount of the fees retained by the broker at section 1.2 from the subtotal at section 1.1a.

3. Transactional deductions by broker: Enter the dollar amounts for each itemized deduction listed at section 3.1 which the broker will take from the agent’s share of the fees due the agent at section 2, calculated in dollars per closing or as a percentage of the agent’s share of the fees.

3.2 Total charges withheld: Enter the total dollar amount of all the figures entered in section 3.1, a through d.

4. Office expenses: Enter the dollar amount estimated to be incurred for each of the itemized expenses listed in sections 4.1 through 4.9.

4.10 Total office expenses: Enter the total dollar amount of all the amounts entered in sections 4.1 through 4.9.

Editor’s note — These office expenses will be incurred because the agent maintains a properly equipped office from which he can conduct business, maintain files and perform the clerical work required to service his clients’ needs.

5. Agent’s business expenses: Enter the dollar amount estimated to be incurred for each of the itemized expenses listed in sections 5.1 through 5.10.

5.11 Total business expenses: Enter the total dollar amount of all the amounts entered in sections 5.1 through 5.10.

6. Marketing and sales expenses: Enter the dollar amount estimated to be incurred for each of the itemized expenses listed in sections 6.1 through 6.7

6.8 Total marketing and sales expenses: Enter the total dollar amount of all the amounts entered in sections 6.1 through 6.7.

7. Agent’s net income: Enter the total dollar amount remaining after deducting the amounts in sections 3.2, 4.10, 5.11 and 6.8 from the gross fees to agent at section 2.

7.1 Income, social security and medicare taxes: Enter the dollar amount of taxes the agent will pay to the state and federal governments for income taxes (federal 15% to 35%; state 5% to 9%) plus fixed federal taxes for social security, medicare, etc. (15.3%). Thus, roughly 20% to 30% of the agent’s net income will be due the tax collection authorities.

8. Agent’s after-tax income: Enter the total dollar amount remaining after deducting the amount entered at section 7.1 from the amount of the agent’s net income at section 7.

9. Other income: Enter the dollar amount of the funds from sources other than fees earned on closed transactions which the agent can rely on as additional funds to cover on-going expenses not covered by brokerage fees the agent receives.

10. Cost-of-entry/Change-of-office: Enter the dollar amount it is anticipated the agent will incur for each of the itemized expenditures listed in sections 10.1 through 10.13 if the agent is a new entrant to the trade or is anticipating a change of offices.

10.14 Total entry/relocation costs: Enter the total dollar amount of all the amounts entered in sections 10.1 through 10.13. This sum represents the capital required for the agent to enter into employment with a new broker.

11. Gross brokerage fee projection/forecast: Provides for an analysis and calculation of the gross brokerage fees the agent must generate to achieve a desired after-tax income. To estimate the after-tax income, the agent (with the help of his broker or other experienced agents) calculates the number of closings in the price range for properties the agent will be handling, the percentage of the price received by the broker as the gross brokerage fee generated by the agent, and the gross brokerage fees for section 1 from which all expenses and taxes are deducted.

11.1 After-tax income desired: Enter the dollar amount the agent deems necessary as his spendable income for the following 12 months. The dollar amount is the sum desired to be attained at section 8.

11.2 After-tax income/percentage of gross: Enter as a decimal amount the percentage figure shown in the right hand column at section 8. By division of the annual after-tax income desired (section 11.1) by this decimal amount, the agent sets the dollar amount of gross brokerage fees (section 1) the agent needs to generate the desired spendable (after-tax) income.

11.3 Gross brokerage fees needed: Enter the dollar amount resulting from the division of the desired after-tax income (section 11.1) by the decimal of the percentage of after-tax income desired be to attained by the agent (section 8 and 11.2).

11.4 Source of income analysis: Enter, as on a worksheet, the price of the agent’s typical real estate transaction, the total fee the broker will receive on the typical transaction and the number of typical transactions the agent will need to close in order to generate the annual gross brokerage fees at section 1 which the agent needs to attain the desired annual income set at section 11.3.

Form updated 06-2017 to include the Form Description at the top, white header/footer convention and RPI branding.

Form navigation page published 09-2017. Updated 01-2026.

e-Book: Career Manual: Your Guide to Personal Branding and Income Enhancement

Article: An agent’s perception of riches

Brokerage Reminder: Recruiting agents – tools and techniques

Brokerage Reminder: Setting standards for recruiting agents

Brokerage Reminder: Recruit and retain for long term success

CalPaces for Recruiting: Interviewing prospective hires

Video: Interviewing an Agent