This form is used by a loan broker when arranging a loan made by a trust deed investor collateralized by an existing trust deed note held by the borrower to prepare an offer by the investor for the borrower’s acceptance stating the terms and conditions for making the collateralized loan.

Assignments of an existing note and trust deed

Brokers looking to expand their business need to consider arranging trust deed investments by soliciting cash-heavy individuals who invest in interest-bearing opportunities to consider trust deed note investments for greater annual earnings.

With higher yields than most corporate bonds and by setting low-risk LTV conditions, trust deed investors can invest directly in trust deed notes, sometimes called paper, rather than their purchase of lower yielding mortgage-backed bonds (MBBs). To invest in trust deed notes wholly independent of Wall Street’s MBB market, these investors need a trust deed broker to assist as an arranger of the trust deed investment:

- to make a loan evidenced by a note in favor of the investor and secured by a trust deed on real estate, a process called origination;

- to buy an existing trust deed note, called an absolute assignment [See RPI Form 241]; or

- to make a mortgage-backed loan (MBL) evidenced by a note in favor of the investor which is secured by the collateral assignment of an existing note and trust deed held by the borrower, called hypothecation. [See RPI Form 242]

Stages of any trust deed note investment

The brokerage stages for arranging a trust deed (TD) investor’s purchase of a trust deed note or making a loan collaterally secured by a trust deed note includes:

- due diligence investigations;

- entry into a trust deed purchase agreement or agreement to hypothecate [See RPI Form 241 and 242];

- mortgage escrow instructions, funding and closing; and

- servicing, reconveyance and foreclosure.

During the due diligence stage of any trust deed note investment, the TD investor and their broker need to document and analyze the risks connected with:

- the payment history on the trust deed note purchased or collaterally assigned;

- the real estate directly or indirectly securing the investment (physical, title profile, income, location and value);

- the borrower’s creditworthiness, and on a collateral loan, also the property owner’s;

- the principal balance on existing mortgages on the property, including the trust deed note being assigned; and

- title insurance for the assignment.

Also, a trust deed broker typically has an inventory of available trust deed notes listed and fully packaged for delivery of information to a TD investor under a transmittal letter for consideration. [See RPI Form 233]

The trust deed note as personal property

A negotiable instrument, such as a promissory note secured by a trust deed, contains an unconditional promise to pay a dollar amount as scheduled to the noteholder. A trust deed note is a negotiable instrument, and thus is either absolutely assigned – as in a purchase of a note – or collaterally assigned to a trust deed investor.

Buying or lending on a trust deed note, such as a seller carryback mortgage, is a reliable and profitable investment for trust deed investors, also called private money lenders or hard money lenders.

Comparable to a buyer of real estate entering into a purchase agreement with the advice and assistance of a competent transaction agent (TA), the trust deed investor buying a carryback note does so with the advice and assistance of their trust deed broker. [See RPI Form 241]

The investor’s broker gathers information provided by the noteholder prior to preparing an offer to purchase a trust deed note. Relevant information to be collected and reviewed with the investor includes:

- the terms in the trust deed note;

- the existing title policy insuring the trust deed (the collateral assignment is not insurable);

- the market value of the real estate securing the debt;

- a title profile on the real estate securing repayment of the note; and

- data on the real estate’s operating income and expenses when it is income-producing property.

Additional disclosures to be received and reviewed by the investor and their broker before closing include:

- a trustor’s offset statement from the owner of the secured property [See RPI Form 414]; and

- a beneficiary statement from each holder of trust deed notes encumbering the property. [See RPI Form 415]

When the mortgage being purchased is carryback paper, all the disclosures and agreements from the sale are also obtained from the seller and reviewed to determine both:

- the sufficiency of the property as security; and

- the quality of the note and trust deed.

Further, the investor and their trust deed broker review the hazard and title insurance policies which cover risks of loss and the conditions of title surrounding the existing trust deed. An appraisal of the property’s value is also appropriate to ensure it functions as sufficient security, as though the investment were the origination of a mortgage.

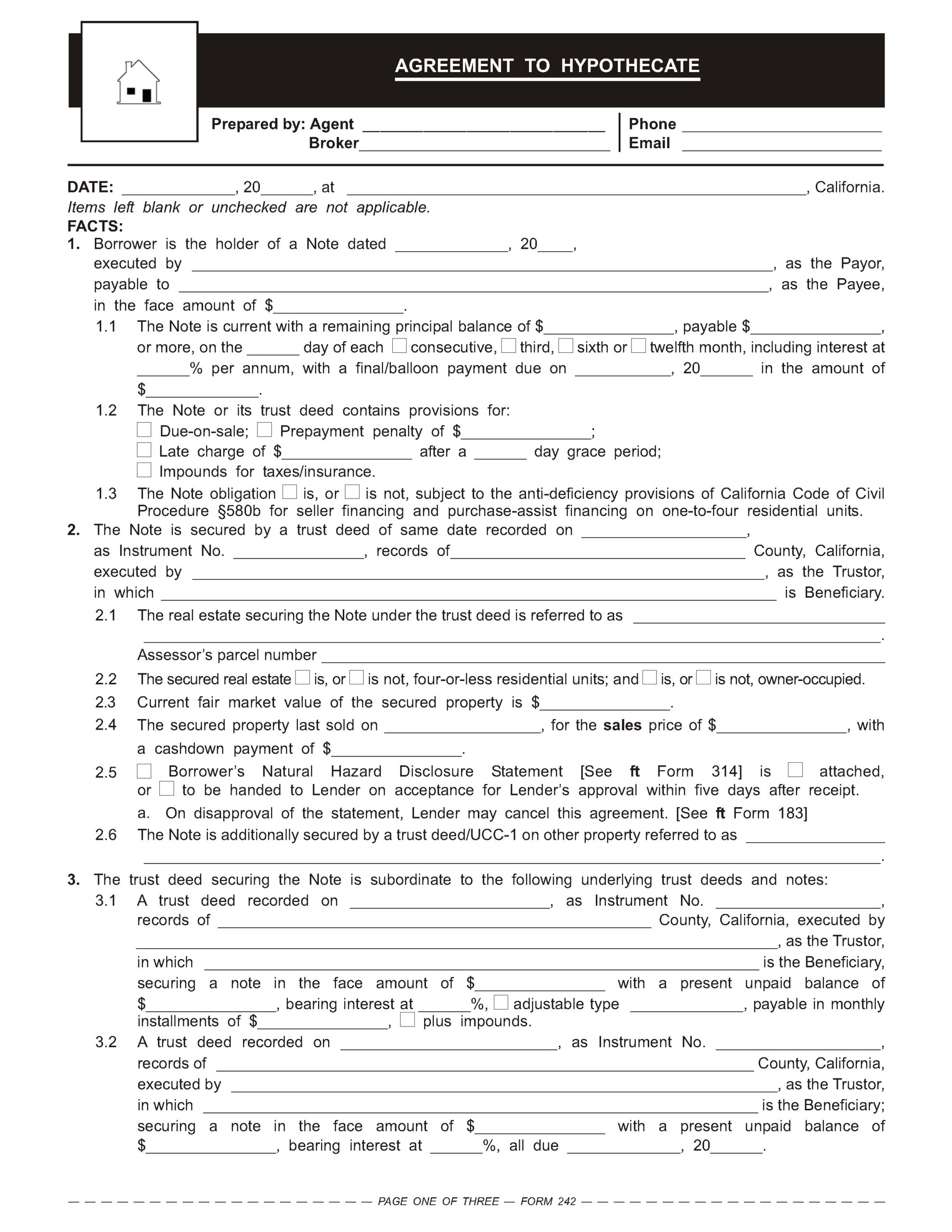

The agreement to hypothecate

A loan broker uses the Agreement to Hypothecate published by RPI when arranging a loan made by a trust deed investor collateralized by an existing trust deed note held by the borrower. The form allows the loan broker to prepare an offer by the investor for the borrower’s acceptance stating the terms and conditions for making the collateralized loan. [See RPI Form 242]

The Agreement to Hypothecate contains provisions describing:

- the existing trust deed note [See RPI Form 242 §§1 and 2];

- the real estate securing the note, including its current FMV, the type of property and whether it’s owner- or tenant-occupied [See RPI Form 242 §§2.1 through 2.6];

- senior encumbrances [See RPI Form 242 §3];

- the terms of the collateralization of the note, such as the purchase price [See RPI Form 242 §4];

- escrow details [See RPI Form 242 §§7 and 8];

- the title insurance company to be used [See RPI Form 242 §9];

- cancellation terms [See RPI Form 242 §16]; and

- the brokerage fee to be paid. [See RPI Form 242 §18]

Form navigation page published 01-2024. Updated 01-2026.

Form last revised 2011.

Form-of-the-Week: Purchase Agreement for Note and Trust Deed, and Agreement to Hypothecate — Forms 241 and 242

Form-of-the-Week: Trust Deed Listing – Exclusive Right to Sell a Note and Consent for Use of Electronic Documents and Digital Signatures – Forms 112 and 109

Article: Arranging hard money trust deed mortgages

Article: Escrowing a note and trust deed assignment

Article: Investing in trust deed notes