Limiting mortgage holder interference

Provisions of a trust deed allow private lenders and carryback sellers to contractually restrict as many aspects of ownership and possession of the liened property as they can control. Restrictions provide reasons, enforceable or not, for exacting further profits from the ownership of the encumbered property.

At first glance, the list of rights given to a private lender or carryback seller, also known as a mortgage holder, seems to authorize their use of tremendous discretionary powers over activity normally conducted and of concern only by owners holding the beneficial use of the liened real estate.

For example, trust deeds routinely purport to give the mortgage holder the unhindered ability to:

- automatically accelerate the balance of the mortgage on the transfer of any interest in the property, such as an owner’s sale, further encumbrance, lease for a term greater than three years or a lease couple with a purchase option, called a due-on clause;

- determine the allocation of eminent domain proceeds after a condemnation action;

- apply all fire insurance proceeds to the mortgage balance; and

- call the mortgage when it or any other loan between the parties is in default, called a dragnet clause.

Related reading:

Fortunately for owners of property encumbered with a trust deed lien, California law unequivocally curbs the mortgage holder’s ability to strictly enforce discretionary provisions, as well as many other clauses which appear in some trust deeds. [See RPI e-book Real Estate Finance, Chapter 13]

For a start in this review, trust deeds are recognized as adhesion contracts. Here, one person or participant (the lender) has superior bargaining power over a weaker person (the borrower), usually on a “take it or leave it” basis.

A prospective borrower typically has no power to negotiate better terms with any lender than to agree to the boilerplate provisions in regular trust deeds, with the lender adamant that “sorry – it’s my way or no way.” The printed terms of the trust deed without deletion will be adhered to by the borrower when arranging financing, no questioning of the provisions.

This distinct imbalance in bargaining power led California courts to develop special adhesion contract rules for interpreting rights and obligations under uniform trust deeds used exclusively throughout the mortgage banking industry. These special rules are a judicial step toward limiting the collective dominance of lender bargaining power and interference, always for extra profits. [Steven v. Fidelity and Casualty Company of New York (1962) 58 C2d 862]

Related video:

Trust deed provisions

Enforceable provisions found in a standard trust deed used to secure the performance of a note include:

- condition of property;

- hazard insurance;

- attorney fees;

- taxes and senior encumbrances;

- acts and advances to protect the security;

- assignment of damages;

- waiver;

- due-on-sale;

- assignment of rents;

- acceleration;

- trustee’s sale;

- trustor’s offset statement;

- special use agreements;

- reconveyance;

- successors, assigns and pledgees; and

- trustee’s foreclosure notices. [See RPI Form 450]

Related article:

Analyzing the trust deed

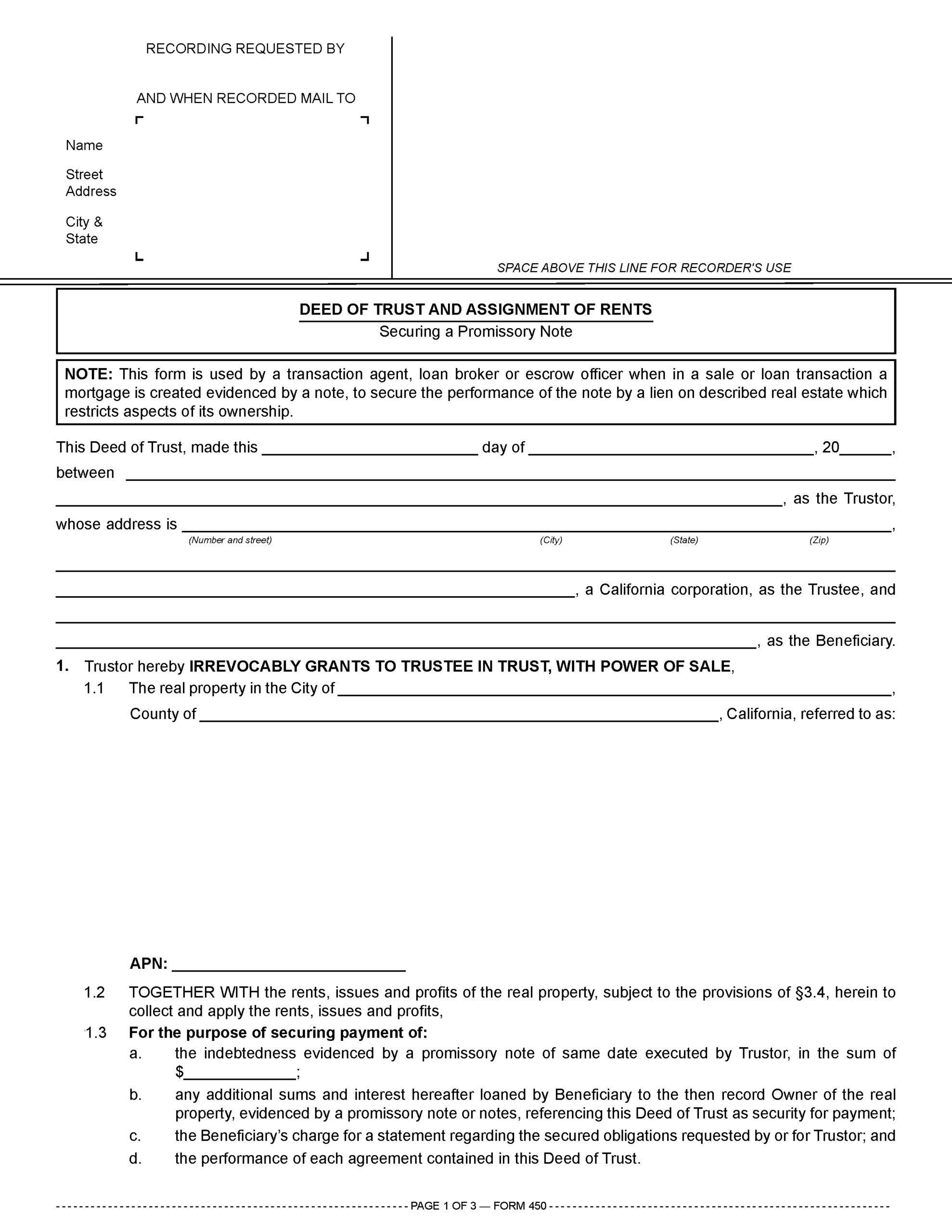

A transaction agent, loan broker or escrow officer uses the Deed of Trust and Assignment of Rents — Securing a Promissory Note published by Realty Publications, Inc. (RPI) when in a sale of property or a loan transaction a mortgage is created as a device to secure a debt evidenced by a note. The trust deed form describes the property securing the performance of the note which by its provisions restrict use of ownership rights in the property. [See RPI Form 450]

The Deed of Trust and Assignment of Rents — Securing a Promissory Note contains:

- the date, identities of the trustor, trustee and beneficiary and address affected by the trust deed [See RPI Form 450];

- the city, county and description of the real estate irrevocably granted to the trustee, and the amount of indebtedness [See RPI Form 450 §1];

- trustor agreements [See RPI Form 450 §2];

- mutual agreements [See RPI Form 450 §3];

- addenda, such as the owner-occupancy rider and all-inclusive trust deed addendum [See RPI Form 450§4; See RPI Form 202-3; See RPI Form 442 and 443];

- a reconveyance agreement [See RPI Form 450 §5];

- a successors, assigns and pledgees agreement which binds all participants and their heirs [See RPI Form 450 §6];

- trustee’s foreclosure notices certifying a notice of default and notice of sale will be mailed to the trustor at their listed address [See RPI Form 450 §7]; and

- the signature of the trustor. [See RPI Form 450]

A notary public then verifies the identity of the trustor and acknowledges the signature – notarizes – on the document so it can be recorded as acceptable by the County Recorder’s Office for public notice.

Related video:

The all-inclusive trust deed debt

An all-inclusive trust deed (AITD) secures a debt, evidenced by an AITD note a buyer executes in favor of a seller to evidence the amount remaining due on the purchase price after deducting the down payment. Occasionally, an owner and a local bank or private lender enter into an AITD financial arrangement for a loan. [See RPI e-book Creating Carryback Financing, Chapter 13]

The terms negotiated for payment of the sales price when the seller carries back an AITD Note include five variables:

- the down payment on the price;

- the principal amount of the AITD note;

- the interest rate;

- the periodic (monthly) payments; and

- the due date.

The characteristic distinguishing an all-inclusive note is its face amount. The face amount of the all-inclusive note is the entire balance of the sales price remaining after the down payment when an existing mortgage remains of record as a continuing obligation of the seller to pay. [See RPI Form 421]

At first glance, the total dollar amount of the debts secured by the underlying mortgage and the AITD appear to over-encumber the property, if you total them.

However, the amount of debt owed under the AITD note wraps around and thus includes the unpaid amount of the underlying mortgage referenced in the AITD addendum. Thus, the separate trust deed amounts cannot be added together to determine the total dollar amount of debt encumbering the property. The amount of the AITD is often the total of the amounts owed on all trust deed encumbrances on the property, and always the amounts of mortgage debt included as described in the AITD addendum.

Related video:

Repayment Variations: Graduated Payment Mortgage and All-Inclusive Trust Deed

AITD final payoff amounts for two variations

An AITD is always a junior mortgage, usually a second. Thus, an AITD is subordinate to one or more pre-existing, underlying mortgages. For lender enforcement and ownership rights, the AITD has the same function as a regular trust deed.

An AITD form is created by using a regular trust deed form with the addition of an AITD addendum. The AITD addendum provisions covers the structure and accounting for the financial aspects unique to an AITD. [See RPI Form 450, 442 and 443]

Two types of AITDs exist based on payoff at reconveyance:

- an equity payoff AITD [See RPI Form 442]; and

- a full payoff [See RPI Form 443]

With an equity payoff AITD, reconveyance occurs when the amount of the seller’s equity in the AITD — the principal amount of the AITD remaining after deducting the underlying mortgage balance — is paid, called satisfaction.

Once the seller receives the payoff for their net equity amount in their AITD and reconveys it, the buyer is left with the primary responsibility for future payments on the originally wrapped mortgage. With the equity payoff AITD, the underlying mortgage is not paid off and remains of record with the reconveyed AITD no longer encumbering the property. In this situation, the buyer originally took title subject to the underlying mortgage.

With a full payoff AITD, reconveyance occurs only when the buyer pays the entire balance remaining unpaid on the AITD note. In turn, the seller as holder of the full payoff AITD, pays off the amounts owed on the underlying mortgage concurrently with the buyer’s satisfaction of the AITD debt. Thus, both the AITD and the underlying mortgage are fully satisfied and reconveyed on the payoff of the AITD. For the buyer, the full payoff AITD is less financially flexible, leaving no alternative for payoff of the mortgages.

Tax-wise, the full payoff AITD is preferable for the seller. The full payoff AITD, without a contract collection provision, provides for no debt relief at any time during the life of the AITD. The buyer may never take over primary responsibility for the underlying mortgage, even on final payoff and reconveyance of the AITD. Thus, the full payoff AITD allows the seller to use the installment sales method of income tax reporting without the issue of debt relief ever arising.

Related article:

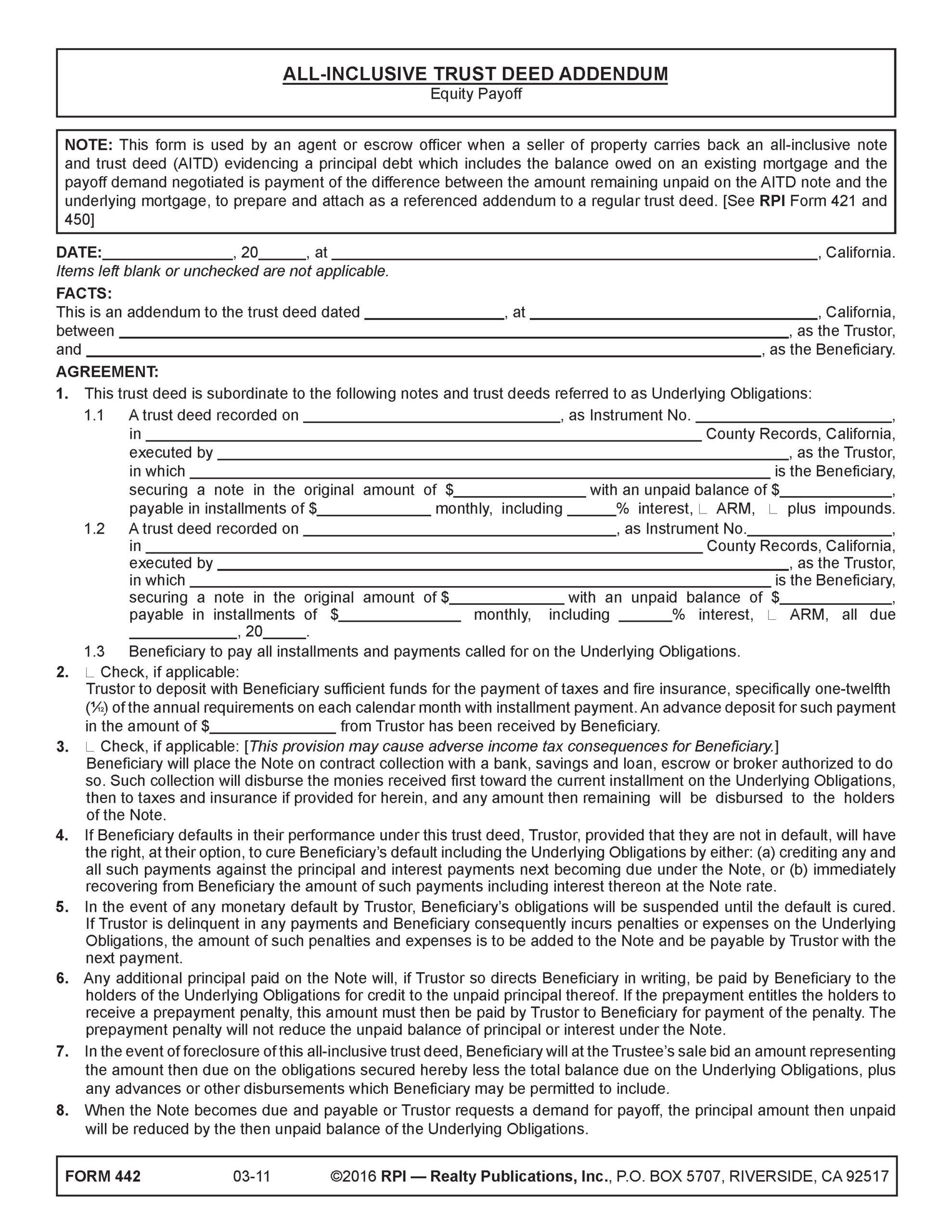

Analyzing the equity payoff AITD addendum

An agent or escrow officer uses the All-Inclusive Trust Deed Addendum — Equity Payoff published by RPI when a seller of property carries back an AITD note to evidence the debt owed, calculated as the portion of the price remaining after deducting the down payment. This debt includes the amount remaining on an existing “wrapped” mortgage.

The seller’s payoff demand for reconveyance of the equity payoff AITD will be the sum of the amount of the debt remaining unpaid on the AITD note minus the principal amount remaining on the existing mortgage which will remain of record. The AITD addendum form is attached to a regular trust deed form. [See RPI Form 442]

The equity payoff addendum for an AITD contains:

- existing financing information which identifies the existing encumbrances on the property, the principal amounts of each included in the all-inclusive note amount [See RPI Form 442§1];

- impounds for the agent to check when impounds will be paid to the seller by the buyer for property taxes and casualty insurance. When a wrapped mortgage is impounded, the AITD is also impounded [See RPI Form 442 §2];

- contract collection for the agent to check when the seller has agreed with the buyer to place the mortgage on contract collection with a third party [See RPI Form 442 §3];

- seller’s default/buyer’s remedies which state when the seller defaults on the underlying wrapped encumbrances, the buyer may cure the default and make payments directly on the delinquent underlying encumbrance [See RPI Form 442 §4];

- buyer’s default/seller remedies which state when the buyer fails to make payments on the AITD, the seller is no longer required to make payments on the underlying wrapped encumbrances unless the AITD is reinstated [See RPI Form 442 §5];

- a prepayment penalty pass-through provision which states a payoff of an underlying encumbrance caused by the buyer or made at the request of the buyer incurring a prepayment penalty places responsibility for payment of the penalty on the buyer [See RPI Form 442 §6];

- a foreclosure bid provision which states the seller’s demand on foreclosure of the AITD will be the amount of their equity in the AITD. The AITD equity is the difference between the balance remaining on an all-inclusive note and the balance(s) remaining on the underlying encumbrances. The buyer at the foreclosure sale takes the trustee’s deed subject to the underlying encumbrances [See RPI Form 442 §7]; and

- a payoff demand provision which states the payoff demand for reconveyance of the AITD. The payoff demand is the difference in the amounts remaining unpaid on the all-inclusive note and the underlying wrapped encumbrances. [See RPI Form 442 §8]

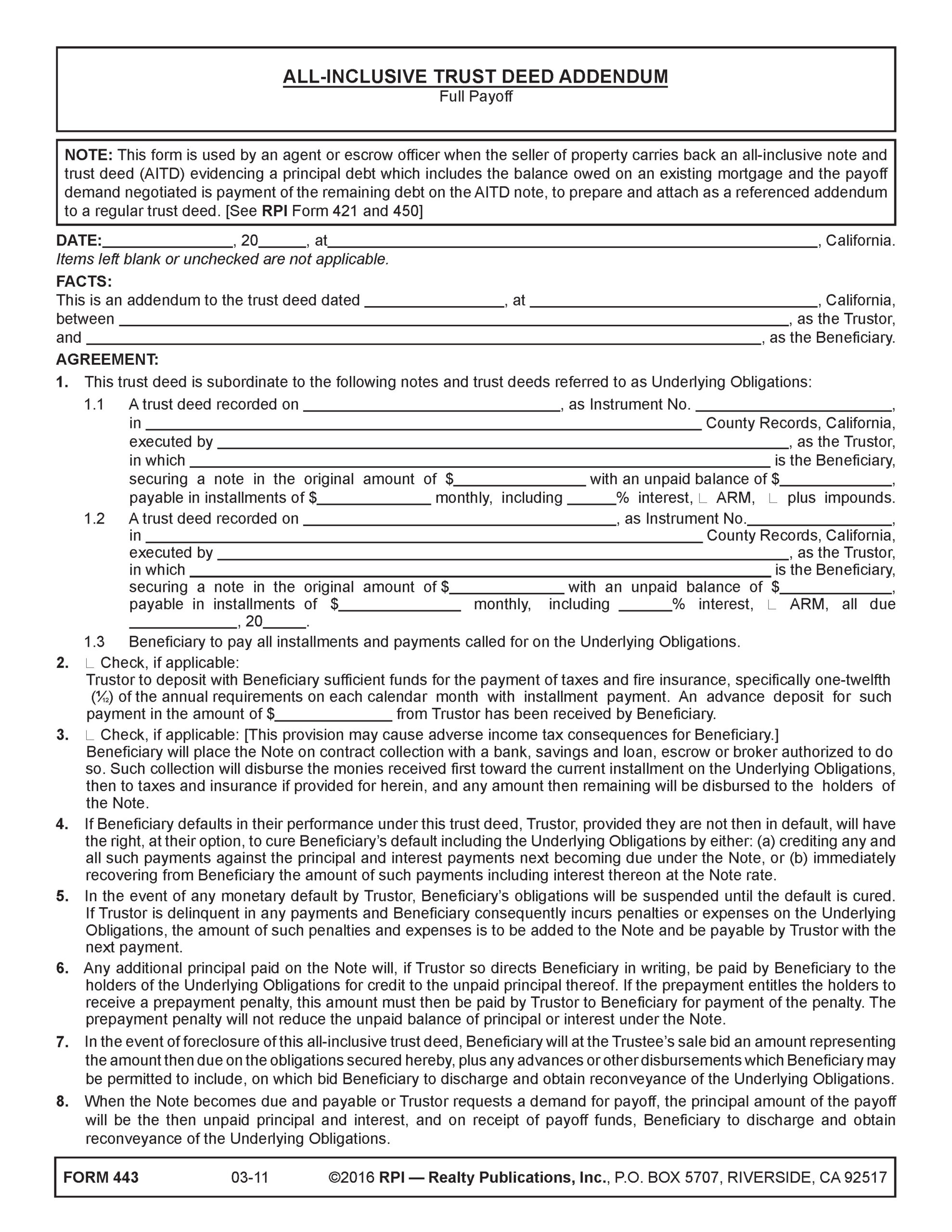

Analyzing the full payoff AITD addendum

An agent or escrow officer uses the All-Inclusive Trust Deed Addendum — Full Payoff published by RPI when the seller of property carries back an AITD note evidencing a debt in the amount of the purchase price remaining unpaid after deducting the down payment from the purchase price. The amount of the AITD note debt includes the balance owed on an existing mortgage.

The seller’s payoff demand for reconveyance of the AITD will be for the full amount of the debt remaining unpaid on the AITD note, which sum the seller will use to satisfy and reconvey the existing wrapped mortgage. The AITD addendum form is attached to a regular trust deed. [See RPI Form 443]

The full payoff addendum for an AITD contains much of the same terms as the equity payoff addendum, except for:

- a foreclosure bid provision states that on foreclosure under the AITD, the seller will demand and bid the entire balance of the all-inclusive note. Concurrent with the foreclosure sale, the seller will satisfy and obtain a reconveyance of the underlying encumbrance, unless the seller is the successful bidder and credits themselves for the amount of the underlying mortgage debt. [See RPI Form 443 §7]

Related article:

Want to learn more about receiving and splitting broker fees? Click the image below to download the RPI book cited in this article.

{kind=link}