Conflict and compromise

When a broker or their agent has a professional or personal bias which might hinder their ability to fulfill the fiduciary duties they have undertaken by acting on behalf of the client, a conflict of interest arises.

In a professional relationship, a broker’s primary objective is to solicit and receive compensation for services rendered. This of course is not a conflict of interest. Rather, it is an exchange of known quantities — brokerage services for an agreed fee. The client — whether a buyer or seller — is entitled to know the exact amount of compensation the broker expects to receive as a result of the employment relationship.

When a broker or agent receives fees and benefits related to the transaction from a participant other than the client, these need to be disclosed. Fees or benefits might include:

- professional courtesies such as referrals made by the broker or their agents;

- familial favors due to direct or indirect involvement of a relative of the broker or any of their agents in the client’s transaction; and

- preferential treatment having monetary value and given by others to the broker or agent. [See RPI Form 119]

A conflict of interest, however, addresses a broker or agent’s personal relationships that are potentially at odds with the agency duty of care and protection owed to the client. Thus, a conflict of interest creates a fundamental agency dilemma — it’s not a matter of compensation or business referral income. An undisclosed conflict of interest is a breach of the broker’s fiduciary duty of good faith, fair dealing and trust owed to the client.

Conflicts abound in everyday brokerage situations

A broker or agent is to disclose a possible conflict of interest as soon as possible after the conflict arises.

Typically, the conflict arises when:

- providing property information to a prospective buyer;

- taking a listing from a seller;

- commencing negotiations to enter into a transaction; or

- assisting in the client’s performance for closing.

Related video:

Disclosing personal or client conflicts creates transparency in the transaction. Here, the client may take the conflict of the broker’s bias into consideration in negotiations, called client consent.

However, consent does not neutralize the inherent bias disclosed. What is eliminated by disclosure and consent is the element of deceit which breaches a broker’s or agent’s fiduciary duty.

Potential conflicts of interest which need to be disclosed to the client include:

- the broker or their agent holds a direct or indirect ownership interest in the real estate involved in the transaction;

- the broker or their agent are directly or indirectly a buyer of the property in the transaction, including a partial ownership interest in a limited liability company (LLC) or other entity which owns or is buying, leasing, or lending on the property [Whitehead Gordon (1969) 2 CA3d 659];

- an individual related to the broker or one of their agents by blood or marriage holds a direct or indirect ownership interest in the property or is the buyer [Sierra Pacific Industries Carter (1980) 104 CA3d 579];

- an individual with whom the broker or a family member has a special pre-existing relationship, such as prior employment, significant past or present business dealings, or deep-rooted social ties, holds a direct or indirect ownership, leasehold, or security interest in the property or is the buyer;

- the broker’s or their agent’s concurrent representation of the opposing participant, referred to as a dual agency situation [See RPI Form 117]; or

- the unwillingness of the broker or their agent to work with the opposing participant, or their brokers or agents in a transaction.

At its most basic level, a conflict of interest arises when a pre-existing relationship exists between a broker or their agents and another person who may hinder the licensee’s ability to fully represent the needs of their client. Conflicts of interest may arise from:

- kinship;

- employment;

- partnership;

- common club membership;

- religious affiliation;

- civic ties; or

- any other socio-economic context.

To disclose or not to disclose

Legislation does not cover all instances in which a conflict of interest may arise and is required to be disclosed. Thus, the courts are left to ferret out these thorny situations.

Brokers and agents, in turn, are left to draw their own conclusions when conflicts of interest arise in the course of a transaction. In practice, licensees too often err on the side of nondisclosure, putting their fee and license at risk. [Calif. Business and Professions Code §10177(o)]

When a broker or agent even questions whether to disclose a potential conflict of interest to a client, the conflict ought to be disclosed as a matter of prudent practice — the very question indicates they should. By proactively disclosing a potential conflict of interest and obtaining consent, licensees reinforce their honest working relationships with clients — and protect themselves from liability.

When a licensee doesn’t timely disclose a conflict of interest, their client on discovery may file a complaint with the California Department of Real Estate (DRE). Depending on the extent breach, the broker or agent’s license may be suspended or revoked by the DRE. [Bus & P C §10177(o)]

Editor’s note — A broker or agent selling or buying property on their own behalf acts solely as the seller or buyer. Their licensee status is not a conflict since they are not acting on behalf of another person in the transaction. [Robinson v. Murphy (1979) 96 CA3d 763]

However, when a licensed broker or agent receives a fee on the sale or purchase of their own property, they are holding themselves out as a transaction agent and now take on a general duty which becomes owed to the other participant. Thus, they become subject to real estate agency requirements which do not arise when the individual acts solely as a principal. Additionally, taxes are incurred at ordinary income rates on the amount labeled a fee.

Preparing the Conflict of Interest Disclosure

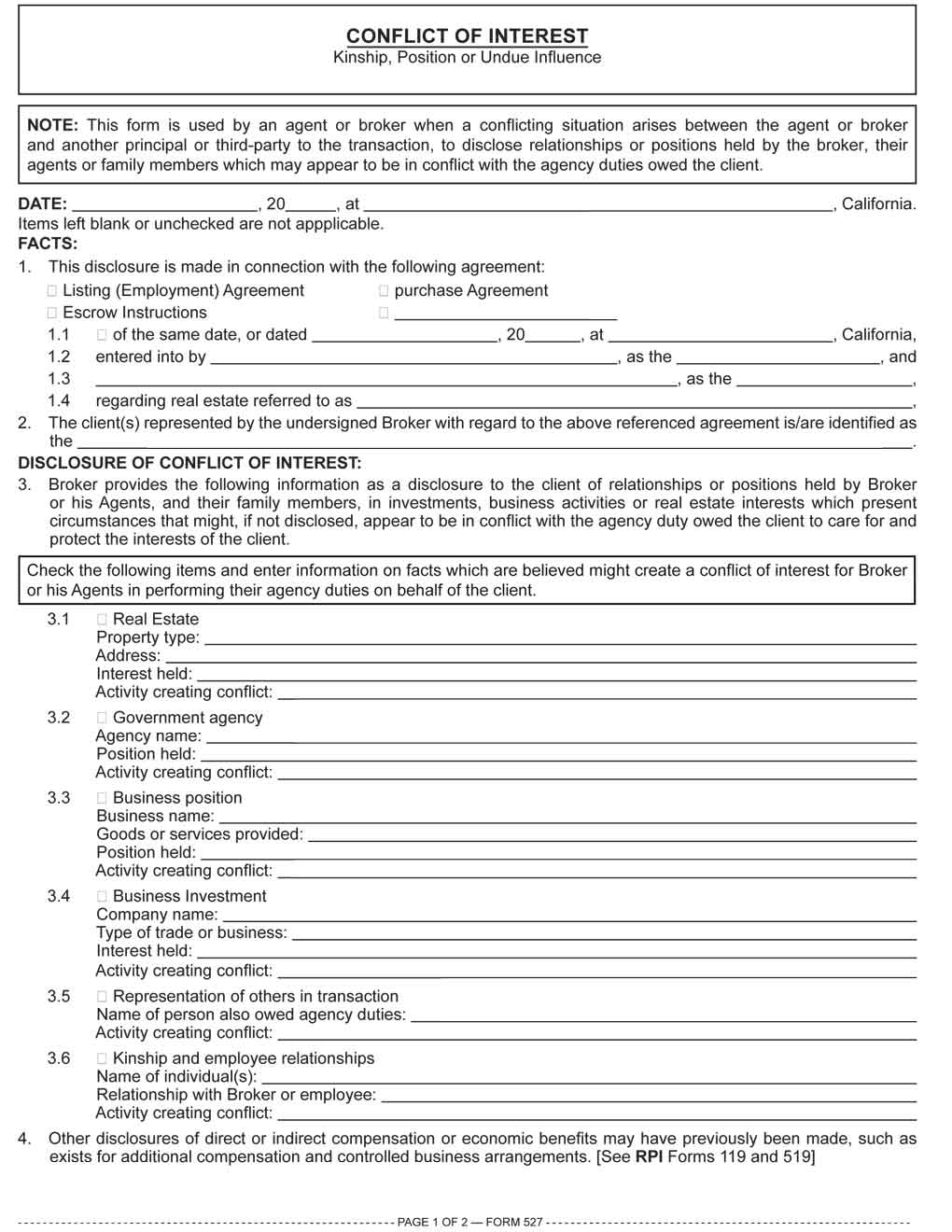

A licensee uses the Conflict of Interest Disclosure — Kinship, Position or Undue Influence form published by Realty Publications, Inc. (RPI) when a conflicting situation arises between the licensee and another principal or participant in the transaction, to disclose relationships or positions held by the broker, their agents or family members who may conflict with the agency duties owed the client. [See RPI Form 527]

The section of the form labeled “FACTS” is used to indicate:

- which type of agreement this disclosure is made in connection with, such as a listing agreement, purchase agreement or escrow instructions [See RPI Form 527 §1];

- whether the disclosure is made on the same date as the previously referenced agreement, or when different, the date disclosure is being make and city where it is being prepared [See RPI Form 527 §1.1];

- the names of the participants involved in the underlying transaction and what positions they hold under the agreement [See RPI Form 527 §1.2 – 1.3]; and

- the address of the real estate involved. [See RPI Form 527 §1.4]

The name(s) of the client(s) represented by the broker or agent making the disclosure with regard to the referenced agreement is noted at the end of the “FACTS” section. [See RPI Form 527 §2]

The body of the Conflict of Interest Disclosure is used to disclose to the broker’s client the specific relationships or positions held by the broker, their agents, family members, or business associates which may conflict with the agency duty owned to the client. [See RPI Form 527 §3]

Such items which may create a conflict of interest include:

- an ownership interest in the real estate held by the broker, their agents, their kin, or business associates [See RPI Form 527 §3.1];

- a position held in a government agency by the broker, their agents, their kin, or business associates [See RPI Form 527 §3.2];

- a business position held by the broker, their agents, their kin, or business associates [See RPI Form 527 §3.3];

- a business investment of the broker, their agents, their kin, or business associates [See RPI Form 527 §3.4];

- the broker’s or their agent’s representation of others in or servicing the transaction [See RPI Form 527 §3.5];

- a kinship or employee relationships between the broker, their agents, their kin, or business associates which many conflict with the client’s objectives. [See RPI Form 527 §3.6]

In each provision, space is provided to clarify the nature of the activity potentially creating a conflict, including identifying people, places or entities involved.

A broker needs to disclose direct or indirect compensation, but this does not constitute a conflict of interest. The Compensation Disclosure in a Real Estate Transaction form is used to disclose the amount, its form and the source of compensation, and the benefits the broker and their agents anticipate receiving for any other service they provide or from any other individual, company, or provider as a result of a participant’s entry into a real estate transaction in which the licensee is acting as a broker. [Bus & P C §10176(g); see RPI Form 119]

Similarly, when a broker listing a property or representing a buyer refers the owner or buyer to a business or service provider the broker owns or co-owns, the broker uses an Affiliated Business Arrangement Disclosure Statement to inform the participant of their ownership interest in that company. The disclosure enables the broker to indirectly benefit from the referral. When properly disclosed, income resulting from these referrals is not a conflict of interest. [See RPI Form 205 and 519]

Profit, not referral fee

In times of slowing real estate activity, residential brokers who list property or represent buyers may generate additional income by becoming full service brokers. Such brokers refer buyers and sellers to lenders and service providers they own or co-own. These business relationships, called affiliated business arrangements or controlled business arrangements, enable the broker to indirectly benefit by sharing in any profits from the referrals they make to these controlled businesses, and do not inherently constitute a conflict of interest. Of course, the controlled businesses need to actually perform all or significant aspects of the service provided.

However, when a consumer mortgage origination is involved in a transaction, a broker’s ability to profit from referrals is regulated by Section 8 of the federal Real Estate Settlement Procedures Act (RESPA).

RESPA was enacted to prohibit brokers and lenders from unnecessarily augmenting a buyer’s costs when negotiating a transaction involving the origination of a federally-related mortgage on a one-to-four unit residential property. These augmented costs for buyers and sellers frequently take the form of illegal referral fees.

Referral fees are paid by service providers, including brokers, for referring business to them so they can perform and be paid for services rendered in connection with a real estate purchase agreement or escrow to close a sales transaction.

Related video:

These service providers include:

- title and finance companies;

- credit reporting agencies;

- home inspection and pest control companies;

- hazard insurers; and

- escrow companies.

A broker who receives a fee for negotiating the sale or purchase of a one-to-four residential unit — when the transaction involves the origination of a mortgage funding the purchase — by a buyer-occupant may not receive a referral fee and a brokerage fee for the same transaction.

However, the broker can still profit from referring a buyer or seller to a service provider when the broker is an owner or co-owner of the service provider recommended, creating an affiliated business arrangement.

For the broker to meet the conditions to profit from an affiliated business arrangement in a sales transaction funded by a consumer mortgage, they need to:

- have an ownership interest greater than 1% in the business they are recommending to the client; and

- provide a written disclosure of the affiliation to the client referred to the controlled business. [See RPI Form 519 and 205]

The referral to an owned or co-owned service provider for profit is not subject to RESPA regulations. As an owner of the service provider, the benefit the broker receives from the referral is not the payment of a referral fee. Rather, the broker receives an indirect benefit from the referral through profits generated for the service provider.

An individual who accepts a referral fee or fails to disclose the existence of the affiliated relationship as prescribed by RESPA is subject to criminal penalties of $10,000, one year in jail, or both for each offense. Also, the person referred to the service provider may receive up to three times the amount of the improper referral fee received by the broker, plus attorney fees, in a civil suit. [12 United States Code §2607(a), 2607(c)(4)(a), 2607(d)]

Analyzing the Affiliated Business Arrangement Disclosure Statement

When a broker indirectly benefits from a transaction as the owner or co-owner of a service provider, the broker’s share of the provider’s profit is comparable to that of a stockholder in a corporation.

As a condition of the referral, the broker referring a seller or buyer to a service provider they own or co-own needs to disclose their ownership of the provider to the seller or buyer before or at the time they refer them to the provider. [24 Code of Federal Regulations §3500.15(b)(1)]

A broker uses the Affiliated Business Arrangement Disclosure Statement – Residential Broker published by RPI when referring a seller or buyer to others who provide services in real estate sales, leasing or mortgage transactions and whose earnings are shared with the broker, to disclose the business relationship and any benefit the broker may derive from the referral. [See RPI Form 519]

Similarly, the Affiliated Business Arrangement Disclosure Statement – Loan Broker form is used by a mortgage loan broker arranging financing when referring a borrower to providers of settlement services whose earnings are shared by the loan broker as a co-owner of the provider. [See RPI Form 205]

Editor’s note —Both versions of the form are identical — with the exception of the type of brokerage service — residential or loan — identified in the subtitle. These two versions exist to place the form in both the “office administration” and “loan brokerage” series of RPI forms. [See RPI Form 519 and 205]

Both versions of the Affiliated Business Arrangement Disclosure Statement reference the nature of the business relationship between the broker and the business providing the settlement services, including:

- the name of the service provider [See RPI Form 519 §2.1—2.3 and 205 §2.1—2.3];

- the percentage of ownership interest held by the referring broker [See RPI Form 519 §2.1—2.3 and 205 §2.1—2.3]; and

- a description of the relationship between the broker and the service provider. [See RPI Form 519 §2.1—2.3 and 205 §2.1—2.3]

The disclosure states:

- the broker may receive a financial or other benefit due to the relationships between the broker and provider [See RPI Form 519 §3 and 205 §3]; and

- the client has the right to shop around and is not required to use the listed providers as a condition of the purchase or sale of the subject property, or for the settlement of their loan. [See RPI Form 519 §4.1 and 205 §4.1]

In addition to providing information concerning the broker’s affiliated business, both versions of the disclosure form contain a list of three available competing settlement service providers which offer comparable services. [See RPI Form 519 §5.1—5.3 and 205 §5.1—5.3]

After the name and description of each competing service provider, space is provided for the broker to enter an estimate of the charges or range of charges offered by the non-required providers. This equips the buyer and seller with an understanding of the prevailing costs associated with the referenced services available in the open market. When they determine the costs charged by the affiliated business are not competitive, the buyer and seller have the opportunity to select any of the other providers to perform the settlement services without any detrimental effect to the underlying transaction. [See RPI Form 519 §5.1—5.3 and 205 §5.1—5.3]

Similar to the Conflict of Interest Disclosure, the Affiliated Business Arrangement Disclosure creates transparency in the transaction, cementing the honest working relationship between broker and client.

This article was originally posted in November 2017, and has been updated.

{kind=link}