As California loosens its strict shelter-in-place orders, many in the real estate industry are left wondering what the market will look like in the near future.

Although real estate brokers and agents may fit into the spectrum of essential workers, depending on their local guidance, their business depends on clients who are subject to coronavirus (COVID-19) shelter-in-place orders. As a result, the industry may well be irrevocably altered. From an emphasis on agents’ online presence to the ubiquity of virtual tours, stay-at-home orders have already changed the way agents do business, and many of these trends will stick around after the pandemic.

However, the more worrying effects will arrive as the 2020 recession sets in. Recession-inducing factors were already well underway by the time COVID-19 entered the scene, but that doesn’t make the news of the most severe U.S.-wide job losses since the Great Depression easier to swallow.

When it comes to the California real estate market, the most important information will be how buyers and sellers — the beating heart of the industry — react to the 2020 recession and financial crash.

Relist or remiss?

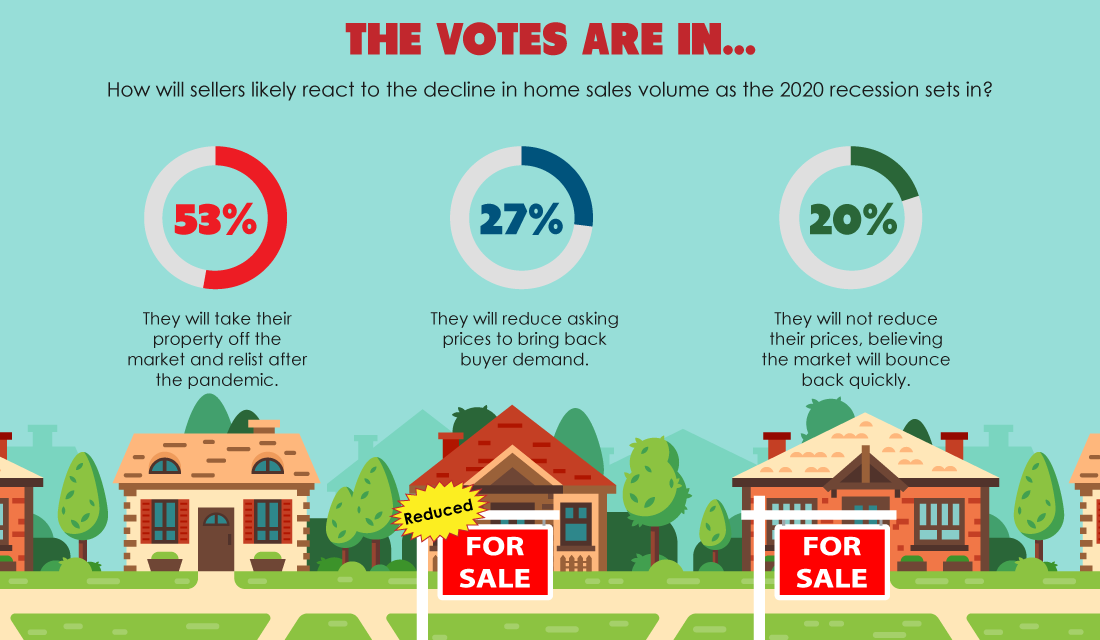

According to a recent poll regarding how sellers will react to declining home sales volume, 53% of respondents believe sellers will choose to cut their losses and take their property off the market to relist once the pandemic — and the recession as a whole — is behind us.

27% percent of respondents believe sellers will simply reduce asking prices in response to slowing sales volume.

Another 20% of respondents, however, are hedging their bets on the market’s resilience, arguing seller behavior will remain unchanged.

Related article:

While a clear majority exists, it’s worth asking which of these options makes the most sense, and how they factor into your practice.

In a vacuum, reducing asking prices might be enough to sway some buyers who might otherwise choose to postpone their purchase of property on account of the virus or the recession. The problem is that many prospective buyers who previously qualified for a mortgage have lost or will lose their jobs as the recession continues. Others no long qualify under the stricter standards set by lenders, which have tightened significantly as job losses have mounted. When buyers no longer qualify, it doesn’t matter how low sellers are willing to go.

Additionally, if declining home sales volume were solely the result of the COVID-19 pandemic, it might be that the market bounces back as rates of infection decrease. However, sales volume was already in decline before the pandemic hit California’s housing market — largely as a result of reduced multiple listing service (MLS) inventory, a lower rate of residential construction and a widening price-to-income gap. While COVID-19 undoubtedly exacerbated the problem, don’t count on the market bouncing back immediately as shelter-in-place restrictions loosen.

As sellers inevitably back away from the market, the wisdom of depending on them as a source of income grows flimsy. In other words, now is a good time to find ways to supplement your income in the midst of the recession, including:

- expanding into the investment property market;

- becoming a notary public; or

- becoming a mortgage loan originator (MLO).

Related article:

{kind=link}