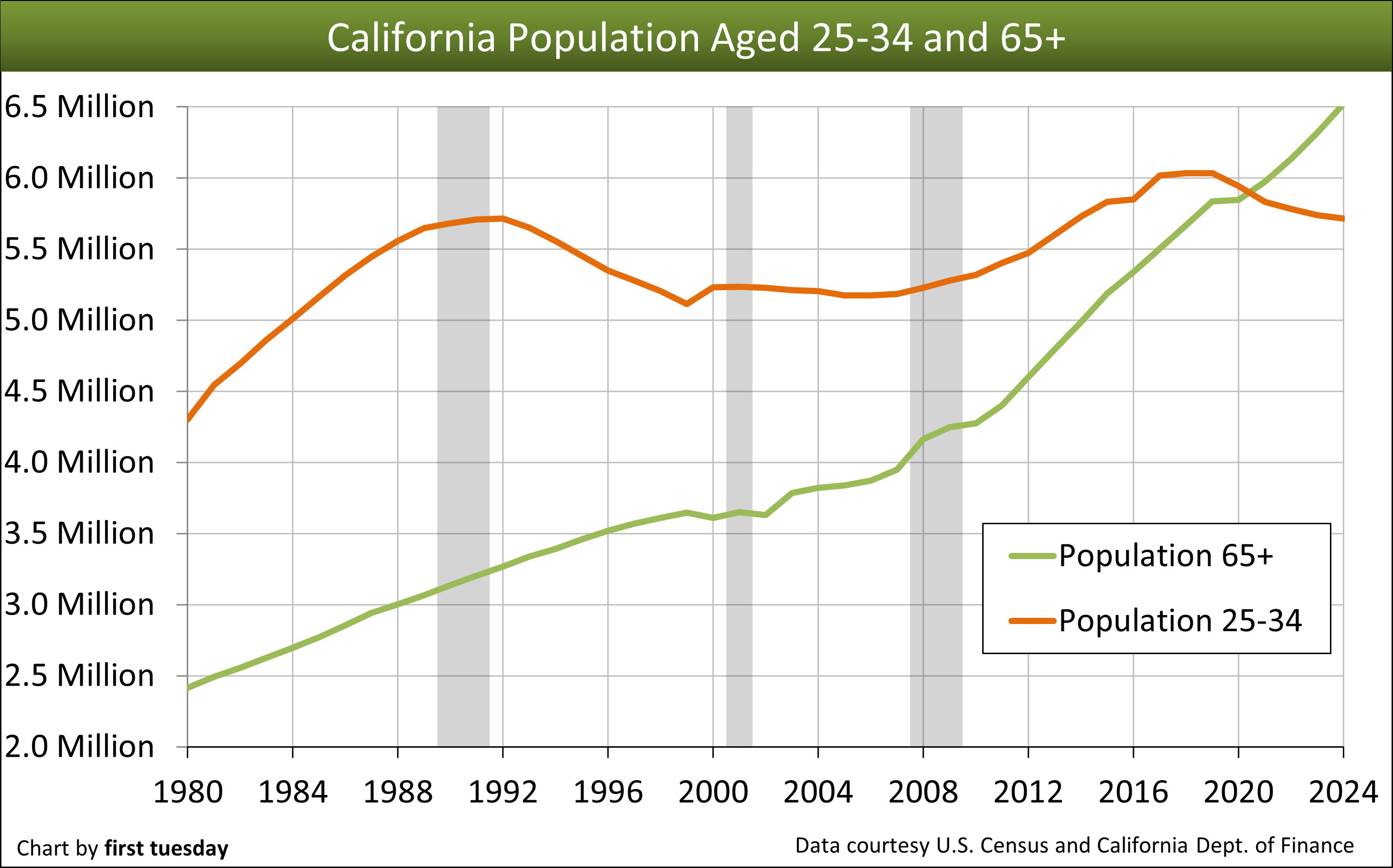

Older Californians are growing in number, at 16.5% of the state’s population in 2024. Further, the number of Californians 65 years of age and older increased 3.2% in 2024 alone.

Roughly three out of four Baby Boomers in the west, aged 65 and up, are homeowners today and will remain so in retirement. Most will sell and downsize, purchasing a replacement home of equal or lesser price. Many are expected to relocate from the suburbs to more convenient city-living.

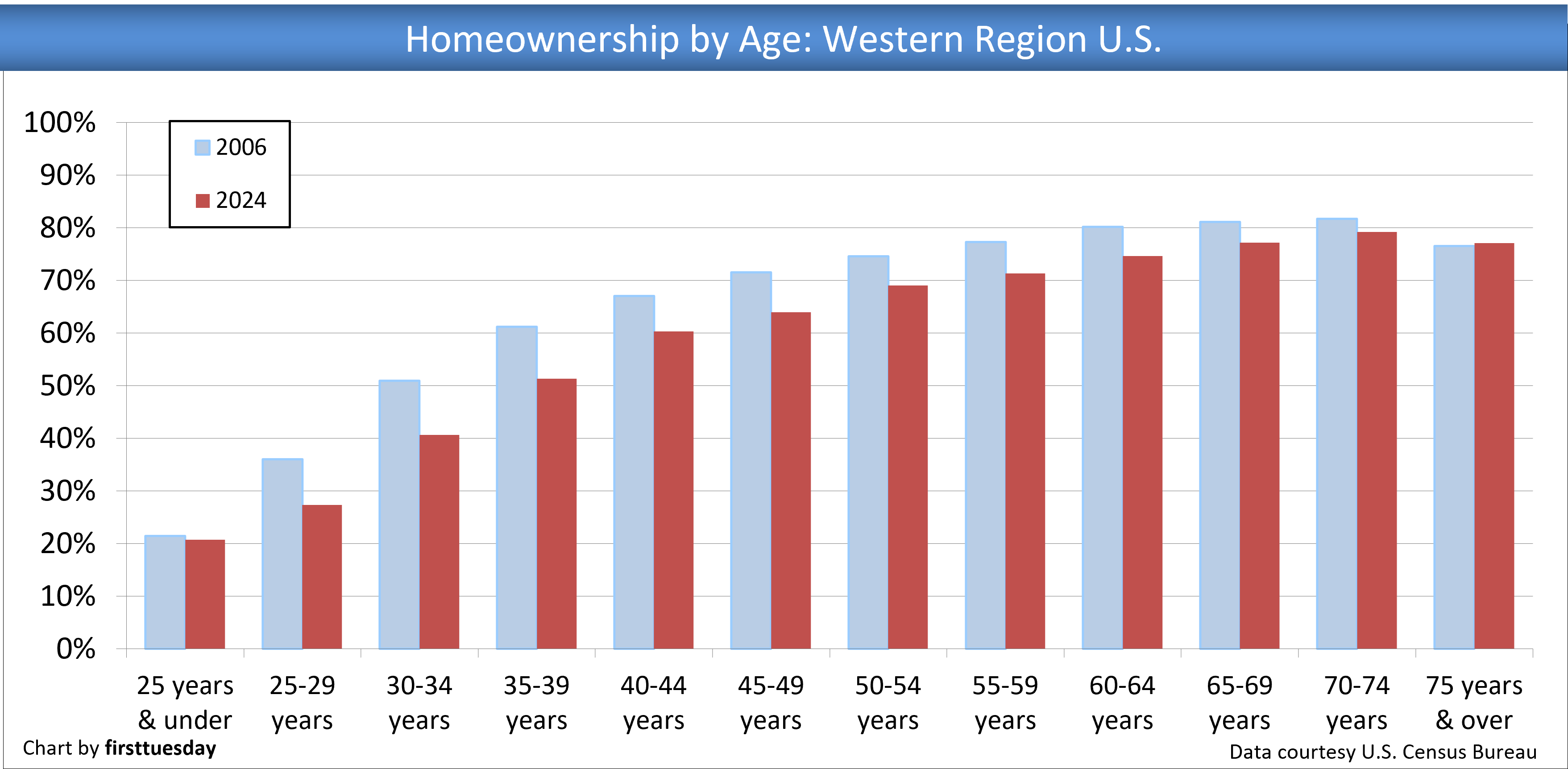

Among potential first-time homebuyers in the region aged 25-34, approximately 34% own a home, down from 43% in predatory mortgage days of 2006. While the population of 25-34-year-olds is growing slightly each year, expect the recent drop in their rate of homeownership to continue through 2028. Presently, they are slowly mustering savings for down payments in spite of education debt and grappling with the financial fallout from the recession – job loss and rent increases – which set in during 2022.

Updated October 6, 2025.

Chart update 10/2/25

Chart update 10/2/25

Chart update 10/2/25

Chart update 10/2/25

| 2024 | 2023 | 2022 | |

| CA Population Aged 65+ | 6,521,900 | 6,318,800 | 6,134,200 |

| CA Population Aged 25-34 | 5,716,100 | 5,738,900 | 5,781,500 |

The two charts above track homeownership by age in the western census region and California’s population of citizens aged 65 and over, respectively. In combination, these two charts tell us about the future direction of real estate ownership and sales transactions among the rapidly growing population of California’s senior citizens.

Retirees move real estate

At about the age of 65, most Californians stop working full time and begin consuming the benefits of social security, Medicare and their years of saving. The decision to retire is often swiftly followed by a series of lifestyle changes as retirees take advantage of their newly found liberty and accumulated financial power.

One of the most significant changes is the sale of the retiree’s current home, typically large for a family now mostly gone, and the corresponding move to a new, more compact and centrally located residence. The relocation will most likely be for a better year-round climate or closer proximity to family.

Where the grandkids are will be where the grandparents move. As California’s population continues to age, senior citizens will exert increasing influence over both the housing market and every other aspect of the California economy.

California citizens aged 65-75 are more likely to own property than any other age group, as displayed on the first of the above charts. The accumulated equity in their homes, combined with their savings from a lifetime’s employment, allows them to exert a disproportionately strong influence on the statewide housing market. When these elderly citizens begin to change their spending and living habits in retirement, they create new opportunities for agents who deal in the market of single family residential (SFRs) sales.

The massive Baby Boomer generation is defined by the U.S. Census Bureau as the generation born between 1946 and 1964 and is second largest in California to Millennials (1981-1996). While the chart above tracks younger Californians aged 25-34 as the typical first-time homebuyer, this age range has not attained prior homeownership levels after the 2008 housing crash brought on by permissive predatory mortgage debt.

As Boomers are now 62 to 80 years of age in 2025 and mostly retired (a process well underway with almost all on social security benefits), every aspect of the state’s economy is changing. The Boomers have spent the last 40 years accumulating their wealth (primarily in the form of stock – not cash) and generally living in large, suburban SFRs but not all are clear of mortgage debt.

Although the 2008 Great Recession wiped out some of their savings and put hundreds of thousands of SFRs on the market (or in foreclosure) before their time, the majority of the Boomers are making housing adjustments. With retirement, “dis-saving” is the collective act now practiced by Boomers.

They start to liquidate their stocks, sell their current homes and embark, unfettered, on the advanced stage of their lives. Others will stay with the home they own, encumbered with a reverse mortgage to extract a monthly income from its equity, the ATM effect at a significant cost.

Related article:

History repeats the hardships of the Boomer generation

The impending increase in suburban SFR home sales among senior citizens will keep housing prices in outlying bedroom communities depressed, limiting the gain Boomers take on a sale. This is a story of supply and demand economics that their generation knows all too well.

Some history: The Boomer wave began renting apartments simultaneously in the early 1980s, driving up rents which led to massive overbuilding of apartments. It took more than a decade for the market to digest the foreclosure and disposal of the inventory via the Resolution Trust. A similar problem rippled into SFR overbuilding going into the 1990s due to the same Boomer pipeline congestion. This Boomer pile on in homeownership also ended badly with house prices bursting when hit with the 1990 recession.

Related article:

In the late 1990s the Boomers began to invest their accumulating wealth in the stock market, which contributed greatly to a stock pricing bubble. The ensuing collapse wiped out much of their wealth stored in stock. Further, the current mid-2020s real estate recession has blatant overtones of the 2008 Great Recession.

Soon the Boomers will begin to sell off a considerable amount of the stock they still retain, and with a bit of luck sell before the current AI tech bubble bursts. Pulling needed cash by liquidating assets will continue with a vengeance for the next 15 years and kill any interesting movement in the stock market.

The price reduction of large suburban SFRs will result as Boomers sell their home during the buyer’s market now developing in the mid-2020s. Thus, suburban home prices are likely to return to their historical mean price trendline during this mid-2020s recession.

The ensuing market-wide price adjustment will undermine the Boomer population’s buying power with a contrary rise in the value of desirable replacement homes they collectively seek in urban centers. While no one can predict with certainty which properties will be involved or just where they will be in this Boomer relocation, historical and current trends give us some hints.

Relocation: where will they go?

Homeowners in California tend to remain in homeownership in retirement, as shown by the first chart above. For agents dealing in SFR transactions, they will experience a relocation event from most Boomers they represent to sell a home. The client’s relocation is a further service agents can offer for a fee under a buyer representation agreement. Moreover, the percentage of citizens owning homes over the age of 75 has remained steady since 2006, while 25-34-year-old’s homeownership rate dropped by 1/4th.

Homeownership is a well-entrenched habit among the Boomer generation, a fact not likely to change with increased age. However, this does not mean homeowners who retire remain stationary, except for those who choose to remain in the family home due to nearby family members and reverse mortgage income arrangements.

Many will relocate to a better climate or a home closer to other family members. With their accumulated savings and home equity, most will have the resources to do so with ease.

To complicate Boomer relocation to city centers, the better educated and more mobile younger generation is migrating with increasing frequency to the cities. There, employment of skilled workers with better pay is more plentiful than in rural areas.

Ironically, their boomer parents are simultaneously attracted to the same urban areas by the increased access to public transportation, the proximity to cultural and artistic institutions and, of primary importance, the closeness of their children and grandchildren.

Related article:

As retirees relocate, the most directly affected housing developments are those catering specifically to the needs of senior citizens. California law exempts seniors-only housing developments from ordinary restrictions on age discrimination. As the demand for senior housing increases, more developers and landlords will take advantage of this exemption. The range in pricing of high-density (high-rise) housing will also work to separate the wealthier retirees from the less wealthy younger generation.

Additional improvements to existing SFRs to accommodate family members as tenants is another phenomenon now fast evolving. Most SFR-improved parcels are now rezoned for the buildout of two-to-four-unit residential construction. California legislation has paved the way for the higher and better use of SFR zoned parcels allowing fill-in construction of more housing on each parcel.

Accessory dwelling units (ADUs) have also prompted a series of legislative changes to smooth the way for these additional casitas or granny flats; attached, freestanding or over-the-garage apartments with no direct access to the main house. A steady stream of Assembly and Senate Bills since 2016 have worked to remove local NIMBY interference with building more homes, loosen zoning laws and even allowed ADUs to be sold separately from the original SFR on a parcel of real estate.

These smaller residences are a tool in solving California’s inventory shortage and offer homeowners rental income and flexibility. Whether homeowners are looking to build for themselves or seeing the added value in purchasing a home with an ADU, these create more options for Boomers looking to downsize. Increased living density and efficiency are especially important in California’s desirable cities.

Related article:

Retirees influence California real estate

As retirees begin to relocate, opportunities will arise for real estate brokers and their agents to assist them in their transition. Farsighted hometown brokers will prepare for this migration now, offering relocation services to Boomers who sell and seek out a replacement property.

Many retirees have historically chosen to leave California for states with a lower cost of living and a more relaxed, “retirement-friendly” reputation. Foremost among these retirement states are Florida, Texas and Arizona. Those with lower retirement pensions may relocate to Mexico.

Agents need to offer their services to those relocating, not just limit services to representing them as sellers. They need to take the opportunity to review the seller’s preferences for a community for relocating and acquiring a replacement home. MLS inventory in the destination community is available instantly to the agent. Understanding the client’s needs for future housing leads to a discussion about the agent representing the seller of a home as a homebuyer in the new community.

Have the seller-client, now turned homebuyer, enter into a buyer representation agreement just like the client did for the agent to represent them marketing and selling their current home. [See RPI Form 103.1] Thus, as services rendered in California for an out-of-state property, the agent’s broker protects their fee when the buyer enters into a written representation agreement.

Related article:

{kind=link}

People who have seen the growth in the value of their home may discover that selling it may result in capital gain taxes of hundreds of thousands of dollars. In addition, their property taxes may rise substantially if they decide to purchase another home. This may cause them to rent rather than sell their existing home. If so, rents may not rise as fast as home purchase prices. This “Fall” in the relative price of rentals appears to already be taking place. . As an alternative, existing home owners may decide to wait until the death of their spouse so that their house can be sold on a stepped up basis. Has the above analysis considered all these factors. If so, when will the increased number of home sales take place? Projecting current trends may enable this to be determined.

It would be unfortunate if elderly people continue living in their homes even if doing so does not meet their needs. This deprives young families from buying a home for their families.

No place in California or anywhere in the nation outside a major city will be safe anymore. Currently, as of July 31, 2018 there are 17 fires going on in California and fire season hasn’t even begun yet. One of those fires is covering more than 120 square miles of more than 100,000 acres.

There are plenty of fires in major cities but they are quickly stopped from spreading throughout the city because major cities include dozens of fire stations with a time of less than five minutes for any firemen to get to a fire. Contrast that with fireman outside major cities which can take up to 30 or more minutes to arrive at a fire and often times only one or two fire stations. Then you have got nothing but dry grass and trees which sparked up is like having a home made bomb. And this has been going on for at least 5 years now as the weather has changed. After you get burned out twice, as some of my friends have, you no longer ever want to live outside a major city.

You move outside a major city at your own risk and do not plan on keeping any valuable or personal possessions inside a home when you live somewhere in the boondocks and be prepared to get the hell out of there at a moments notice even at 3 a.m. or a fire could be right on top of you in minutes with no escape.

Retires are going to realize that they may not be living in the most ideal place in a city but it is a lot more secure and so they will not move.

Yea, live in the crime-free cities in California. LA, SanFrancisco, SanDiego. Do you not read the real news or just receive the fake news given out by communists/democrats. I’ll sit where I am in the country any day. Don’t lock my doors leave the keys in the car and forget to close the garage doors. Also, know all my neighbors for at least a 2-mile radius. We also all help each other out and share bread with one another. Try finding that in your crime-free City.

After 53 years in California, my wife and I retired and moved to Las Cruces, New Mexico. We sold our house in California, paid off the existing mortgage, purchased a brand new home in Las Cruces, and still have nearly $50k left over to buy new furniture, etc.

Of course, I have a monthly pension that will pay all the bills and continue to grow our IRA nest egg which is a healthy and considerable sum. In three years, I will be able to collect social security and increase our annual income to approximately $50k a year, debt free. We plan to travel and invest in rental properties using a self-directed IRA to diversify our investment portfolio away from the volatile stock market. We don’t need to grow our savings as much as we’d like to shelter our investments from the sudden collapse of a bear market. Our 401k was devastated by the 2007/2008 real estate bubble burst.

Those thinking of moving from California to Oregon to retire should take a hard look at Las Cruces, New Mexico. I’m glad we did.

This is why Proposition 13 works and how it is meant to work. Retired folks who choose to stay in their homes aren’t forced out by higher and higher property taxes (higher State taxes may force them to leave, but that’s another debate). When the retiree sells their home the property taxes automatically adjusts to the current property value. The cycle starts over and the new buyers are aware of what their housing costs are and will be for the foreseeable future (depending on their mortgage of choice).

California is part of a world wide economy and not a closed economy. The effect of the “boomers” in the grand scheme of things is not near as great as the parochial author implies.

I see retiring boomers moving out of California, I have people I know doing just that. With the ever higher taxes and government intrusion of this states government, leaving is a very good option. What is happening is the tax payers leaving and tax users staying or moving in. A boomer cashing out of their house in California can leave buy a much nicer home and still have a lot of money left over for retirement.

As a born and bred city dweller I am also convinced the majority of people will continue to live in the cities, but I also believe that resort areas will pull many out to the country to enjoy the peace and serenity found only in the country. With modern conveniences now prevalent among today’s rural communities, satellite TV, internet services, e-readers these rural areas now offer the benefits of both worlds. Also, today’s seniors are much more active than earlier generations and can benefit more fully in the outdoor activities available in modern day resort areas. With urban environments becoming more dense and polluted the escape to the lifestyle country living provides will encourage more people to get out of the cities.

The above article gives a very analytical summary of what is currently transpiring in our state and is quite thorough. Seniors not only exert a powerful influence on the housing market but also exert a strong political influence, especially on the local level.

Currently we find ourselves in the midst of a monumental international struggle, as the minions of the Banking Cabal which controls certain Western capitals and exerts its power in New York and Los Angeles in its financial and media empires, is locked in a life-and-death struggle to maintain its grip on power.

Opposing this Cabal is the growing power of the BRICS alliance, led by Russia and China. Vladimir Putin knows full well the goal of his adversary is the destruction of Russia, and one main weapon towards that end is the collapsing of oil prices.

Putin has vowed to weather the storm and continues to stand for Christianity, morality, decency, and order while being opposed by those who are trying to throw the world into chaos.

Who knows better than the “baby boomers” what the ravages of war can do—world war. They grew up hearing stories from their fathers who fought the last world war, and who themselves grew up during the Great Depression.

Within the minds and hearts of the baby boomers are the memories (history) of what this nation and this world endured during those dark years from 1929-1945. They, perhaps more than any, know what a third world war would do to the planet and its people.

The baby boomers are among the first to awaken to the realities of the current grave situation and see things in a “truer” light. As the controlled media continues to spread its half-truths and untruths, it befalls the boomers to keep an eye to the past for perspective as they help shape what we all hope will be a future free of the negative influences currently present in the halls of power.

Overlaying the mass retirements of the baby boomers is the hovering crisis of the currency. Is the dollar about to lose its world reserve currency status? That seems inevitable due to the weighty debts crushing the nation, thanks to the Federal Reserve. What will replace it? Will the US begin issuing Treasury notes in lieu of Federal Reserve notes?

Since it is the baby boomers who hold most of the cash in America, it is they who would be most affected by any currency devaluation or collapse. It behooves all conscious persons to watch closely now what is happening on the geopolitical scene. That WILL impact us all……………..whether you believe it or not.

The future may belong to the young, but for now, it is the baby boomers who are still shaping it, as many of them remain in positions of influence. May they chose wisely when the time comes.

Good article. But, I am not sure baby boomers will move out

of big cities. Many retirement areas like Hemet have gone down hill.

I see the boomers cashing out 401k’s and pensions and buying other homes

to rent. With huge lump sum cash out of pensions, there is no

longer a need to downsize.

Appreciate your insights and education.

I have been a long time reader and now subscriber. I follow your articles and opinions and find the almost

always you are “right on” Keep up the good work.