Funding off-site improvements

A subdivider’s financing scheme to separately fund off-site improvements is called Mello-Roos. The scheme is deceptively entitled a special tax. It is a mortgage subject to judicial foreclosure rules, not a tax with its statutory penalties and a five-year redemption period.

Worse, the deception is perpetuated through the collection of annual payments. Interestingly, the task of collecting payments is assigned to the county tax collection authority for each county, acting on behalf of the improvement district. Further, the annual installment of principal and interest is called an “assessment,” a fabricated misnomer for borrowed funds.

The annual installments are due over a 20-year amortized payoff period. The owner of the property securing the Mello-Roos bonds pays them. Each property is allocated, called an assessment, its share of the total borrowings to pay the cost of the district’s off-site improvements. The debt accrues interest charges like a note for any mortgage obligation. [Calif. Government Code §§53311 et seq.]

The Mello-Roos debt, as allocated, separately encumbers each parcel in the improvement district with a fixed principal amount. The debt remains due and unpaid until it is prepaid or fully amortized. The interest rate accrues at an annual rate on the remaining principal. The rate is based on the rate charged on the bonds the lien secures on each property in the improvement district. At any time, the owner or a junior lienholder may pay off the lien for the improvement bonds and the lien released from title to the parcel.

These infrastructure improvement bond liens are junior to annual property taxes. An improvement district bonding scheme for adding improvements to the right-of-way infrastructure of an existing neighborhood, or in several adjoining neighborhoods, is authorized by the Improvement Bond Act of 1915.

Further, the 1915 Improvement Act provides a financing arrangement available to current parcel owners in an existing subdivision to fund new off-site improvements. These neighborhood upgrades increase the quality of the neighborhood, and with it the value of the properties benefiting from the improvements.

Related Client Q&A:

Client Q&A: What are special assessments and Mello-Roos bond payments?

Mello-Roos tax deductible status

Mello-Roos debt is not an ad valorem tax. Ad valorem taxes are property taxes based on the assessed value of the land and improvements set by the County Assessor. Mello-Roos bond liability is not based on the value of a property but based on each property’s benefit from the improvements the bonds fund.

Mello-Roos payments are not tax deductible on income tax returns in California. Mello-Roos annual payments are not based on the assessed value of the property. [California State Board of Equalization]

Mello-Roos may not be written off on federal tax returns either. Here too, property taxes are only deductible when based on the value of the property, which Mello-Roos aren’t. Further, taxpayers may not deduct the payment for improvements, just depreciation when permitted, according to the Internal Revenue Service (IRS).

Notice of Assessment, obtained and disclosed as mandated

The marketing for sale of one-to-four residential units encumbered by a Mello-Roos or other 1915 Act improvement bond requires the seller to disclose the existence and terms of the bonded indebtedness. To comply, sellers need to obtain and deliver to prospective buyers a notice prepared by the improvement district office entitled either Notice of Assessment or Notice of Special Tax. [Calif. Civil Code §1102.6b]

Anyone may request a Notice of Assessment from the office of the improvement district at any time, including both the seller agent and the buyer agent. No particular manner of request is required since it may be an oral or written request. The maximum charge for the service is $10. [Gov C §58754(b)]

However, a seller of property has the primary obligation to request the notice and deliver it to prospective buyers as soon as practicable (ASAP) on initial inquiry into further property information. This owner obligation owed to a buyer triggers the seller agent to advise their seller to request the notice. The seller broker obtains the request when entering into a representation agreement, formerly called a listing agreement, authorizing the broker to locate a buyer for the property. [See RPI Form 137]

The seller agent may request the Notice of Assessment themselves when the seller refuses to assist the seller agent with the seller’s statutory duty to disclose the lien. However requested, the agent includes the Mello-Roos notice in the marketing package prepared to inform prospective buyers about significant relevant property information. Information presented in a marketing package is either mandated, as is the case with assessment bonds, or known to the seller and seller agent to exist. [See RPI e-book Due Diligence and Disclosures, Chapter 19]

However, when the seller enters into a purchase agreement with a prospective buyer before the buyer receives the Notice of Assessment, the buyer has a statutory contingency allowing the buyer to cancel the purchase agreement. The buyer has three calendar days after a tardy hand delivery of the Notice of Assessment (five days after posting it by mail) to cancel the purchase agreement. The cancellation is delivered to the seller or the seller agent, not escrow, using a Notice of Cancellation. [Gov C §53754(c); See RPI Form 183]

Related article:

Mello-Roos liens, a tax or a mortgage

The owner of a property within a Mello-Roos Community Facilities District pays bond annual installments on the Mello-Roos with payment of their regular property tax bill.

When selling a property encumbered with a Mello-Roos lien, any delinquent payments or the entire debt needs to be paid, unless otherwise agreed. The Community Facilities District who holds a delinquent Mello-Roos lien may commence judicial foreclosure to force a sales auction to collect the Mello-Roos debt.

Some purchase agreement forms contain a purchase price provision calling for the buyer to take title subject to a Mello-Roos lien as part of the purchase price. This arrangement occurs during recessionary periods.

Alternatively, the purchase agreement may provide for the Mello-Roos debt to be treated like a tax but without proration or accounting for its principal balance. This arrangement results when buyers are subjected to boomtime recovery fever, the fear of missing out (FOMO).

When the purchase agreement treats the Mello-Roos debt as a tax, the broker is misrepresenting it as taxes assumed by the buyer, not principal on a mortgage debt.

Contents of the Mello-Roos assessment notice

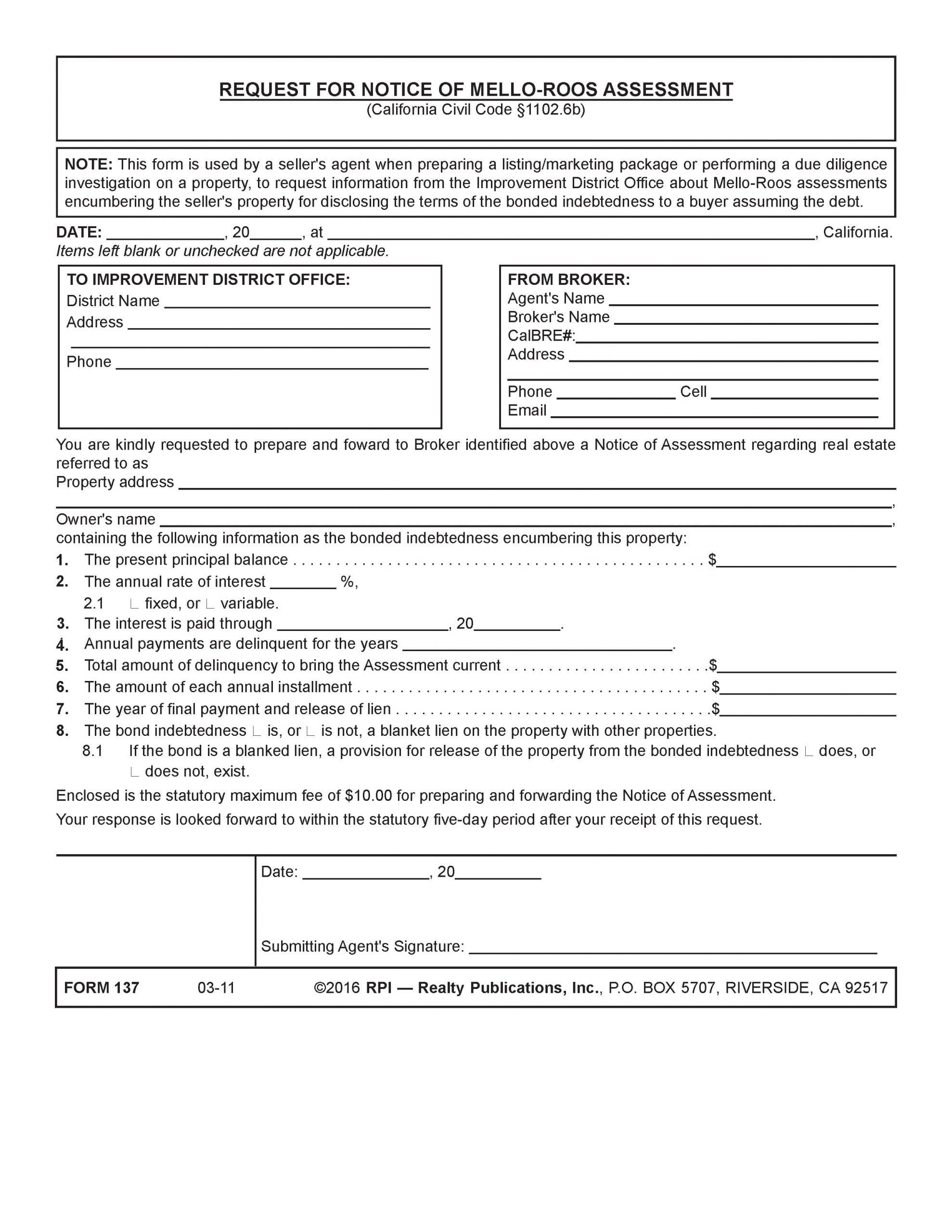

A seller agent uses the Request for Notice of Mello-Roos Assessment form published by RPI when preparing a marketing package as part of their due diligence obligation owed their seller, and in turn the buyer and the buyer agent when they assume the debt. The notice requests information from the Improvement District Office about the Mello-Roos lien on the property. [See RPI Form 137]

The contents of the Request for Notice of Mello-Roos Assessment include spaces for the Improvement District Office to fill out the information, including:

- the present principal balance [See RPI Form 137 §1];

- the annual rate of interest as a percentage, and whether it is fixed or variable [See RPI Form 137 §2];

- the date or length of time for which the interest is paid [See RPI Form 137 §3];

- the years for which the annual payments are delinquent [See RPI Form 137 §4];

- the total amount of delinquency to bring the assessment current [See RPI Form 137 §5];

- the amount of each annual installment [See RPI Form 137 §6];

- the amount on the year of final payment and release of lien [See RPI Form 137 §7]; and

- whether the bonded indebtedness is or is not a blanket lien on the property with other properties. [See RPI Form 137 §8]

The agent making the request signs the form and forwards it together with the maximum fee of $10.00. [See RPI Form 137]

Related article:

{kind=link}