A crisis squandered by an inactive government

Conventional wisdom holds that foreclosures are triggered when homeowners owe more on their mortgages than the fair market value (FMV) of their homes — in other words, when they are underwater. This is a financial condition called negative equity (the opposite being positive equity which permits a conventional sale with net proceeds going to the seller.

Updated June 1, 2026.

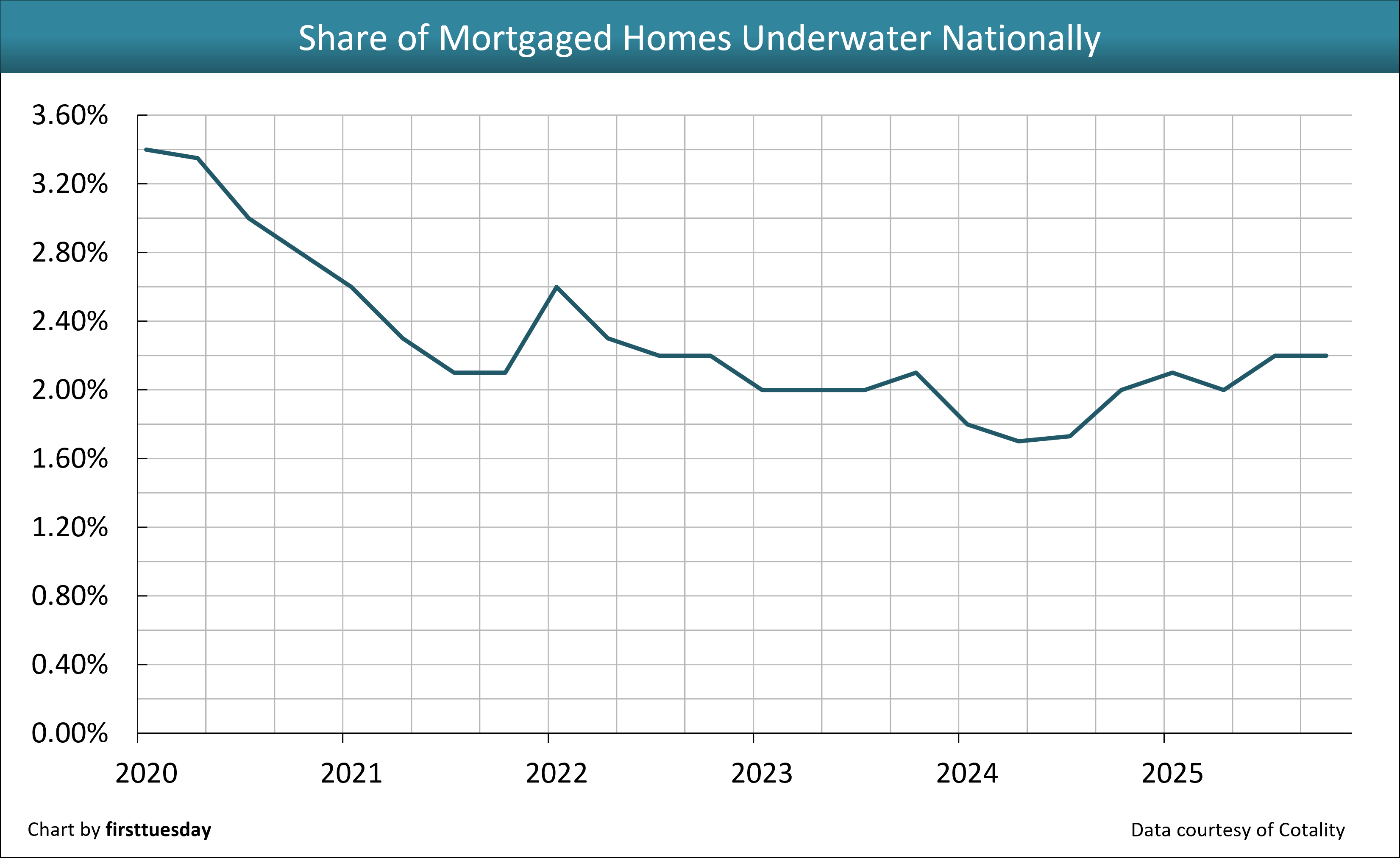

Chart 1

Chart update 5/20/26

| Q4 2025 | Q4 2024 | Annual Change | |

| Percentage of homes with negative equity nationwide | 2.20% | 2.00% | +10% |

Experienced by a debilitating one-third of California’s homeowner population in the years immediately following the Millennium Boom, negative equity is universally feared by homeowners, lenders and policymakers alike. Consistent with this wisdom, negative equity is often blamed as the primary cause for the rise in foreclosures that invariably accompanies a bust in real estate pricing as occurs in each business cycle.

In response to the huge increase in households with negative equity homeownership and the corresponding foreclosure frenzy in 2008-2011, the government unleashed a series of policies. The attempt aimed to induce lenders who made the bad mortgages to offer mortgage modification in lieu of foreclosure, reasoning it was in the public interest.

When negative equity is the problem for an employed owner, mortgage modifications, most effectively in the form of reduced mortgage debt and payments (also known as a cramdown), are the preferred solution. However, the federal administration in 2005 put an end to mortgage cramdowns for families who owned the home they lived in — but available to investors owning an identical SFR next door. Yet government efforts to generate mortgage modifications were largely unsuccessful as they were the only viable alternative to court ordered cramdowns, owner default and lender foreclosure.

The lending industry historically disregards government incentives to modify mortgages with impunity. However, lenders are less able to ignore the lawsuits of state attorneys general, which do induce action. Without modifications, marginally insolvent homeowners go into foreclosure, the negative equity default.

The lack of debt restructuring as policy puts a drag on the state’s economy and personal financial well-being. Just in California, some 1.1 million households lost their homes in the 2008 Great Recession period through 2012.

The remaining balance of negative equity

When lenders do choose to modify a mortgage, they leave the mortgage balance intact and the accrued interest unforgiven. This is the extend-and-pretend approach lenders use to keep the mortgage reportable as “performing.” The catch is the owner’s inability to pay as agreed when burdened by negative equity is a trap only avoided by the buoyancy gifted by a recovering economy, as took hold in 2013.

However, the result worsens from complications of the “disease” of negative equity in a recession. The debt increases every month killing off any opportunity to sell the negative-equity property so the owner can restructure their financial life.

Modifications merely reduce the monthly payment, deferring payment of any reduction in exchange for extending into additional years of the mortgage payments while interest accrues unpaid. Property taxes and insurance premiums build up and do not go away.

Congress guaranteed this result in 2005 for homeowners seeking debt relief from insolvency due to negative equity during a recession. Homeowners, but not home investors, are barred from bankruptcy relief reducing the mortgage balance when the home value is less than the mortgage debt.

Thus, the lender either makes a deal or is forced to buy the property by foreclosure sale. To force a foreclosure, the underwater owner simply exercises their legal right to default and rid themselves of the otherwise unmarketable property.

That lender perspective is best encapsulated in a 2008 study from the Federal Reserve Bank of Boston (FRBB).

Contrary to popular belief, the FRBB study found negative equity on its own is rarely sufficient to induce foreclosure. By examining historic foreclosure rates in Massachusetts over a 20-year period, the report found that over 90% of homeowners with negative equity continued to pay their mortgages since they did not lose their job and were not forced to relocate.

What then compels a negative equity owner to strategically default — forcing the lender to foreclose?

A 2016 paper by the FRBB, an acknowledged arm of mortgage lenders as a federal agency, identified the main culprit for strategic default — job loss or other financial shock. Negative equity status was revealed to rarely play a primary role.

This fact is not lost on mortgage lenders who play hardball, even after they are forced to foreclose. In the meantime, they destroy for a decade the owner’s credit for buying a home at a price they can afford in a location where they find a job.

Further, the 2016 report demonstrates that strategic default almost always remains a seldom-used option for homeowners. Homeowners are faced with many economic disincentives that accompany the foreclosure process. These personal family issues drive negative equity owners to hold on to their homes, in spite of the severe long-term financial costs imposed by the desire to retain ownership for the sake of the household.

As a result, the family becomes prisoners in their own home, policed by lenders seeking to keep their mortgages performing. No help here from Congress as the lobbyists’ money does not lie with homeowners.

A viable debt relief alternative, eventually agreed to by lenders and mortgage insurance when their REO foreclosure inventory builds up, is the owner’s market priced sale of the property also known as the short sale arrangement. Here, the mortgage debt is declared satisfied in a discounted payoff on receipt of the owner’s net proceeds from selling the property.

Of course, the owner’s credit is destroyed for owning a home to house their family. However, they make good long-term tenants for landlords when a member of the household has a job. Thus, after 2012 investors piled into SFR ownership as never before experienced. Their sole opportunity was the horde of prospective tenants coming out from turnover on the foreclosure of their home.

In 2026, investors still are buying and renting to tenants who have not forgotten what the double-edged sword of mortgage debt can do to you.

Negative equity — plus a shock — spells default

Even when the outstanding mortgage balance exceeds the home’s market value, lenders argue the more personally sound decision for homeowners is to continue making payments on their mortgages when they are able. For marginally underwater homeowners, these features, well, carry some water.

This is due to:

- the costs of relocating;

- the damage done to credit; and

- the emotional distress associated with failing to keep their home.

Combined, these factors keep relatively solvent homeowners in their residences — imprisoned — unless some additional external factor tips the scale of their judgment.

When the preponderance of underwater homeowners are not in fact at risk of default due to inability to pay, then mortgage modifications that reduce the mortgage balance or interest rate are argued as an unnecessary loss for lenders. This juxtaposes the owner who saddles themselves with principal and interest payments on a mortgage exceeding the value of occupying the home and excessive property taxes in future years. Great for their mortgage lender.

Why would lenders effectively offer discounts to owners who would never have defaulted in the first place?

This lender logic also applies to the approval of a short sale.

Short sale approval involves a discount given to owners, if they will give up their family residence. However, the lender forces the owner to first default after which the lender files notices to foreclosure in order to deliberately cause adverse credit reporting. This occurs when the owner is actively seeking a way out from under what has become an unreason amount of mortgage debt for which there is no other way out.

The risk of the economy turning sour is a risk taken on by both the owner on acquisition and the lender on a mortgage origination. However, the owner is in a weaker position than the lender. Thus, it is the owner who is penalized. Here, the owner forces the issue by

- selling at current prices contingent on the lender discounting for a final payoff; or

- continuing to occupy until the foreclosure sale and eviction.

The primary relief when offered to the homeowner is a forbearance agreement. Here, the lender temporarily reduces monthly mortgage payments while leaving in place the mortgage’s original terms – and a collection of accrued and unpaid interest.

These are far more frequently considered by lenders. Unlike other measures, forbearance agreements are economically beneficial primarily to homeowners who are at serious risk of foreclosure and their home has positive equity to protect.

During 2020-2021, heightened numbers of homeowners entered forbearance programs under the Coronavirus Aid, Relief and Economic Security (CARES) Act. It was a time consisting of record-low foreclosures, despite high levels of job loss and mortgage defaults.

However, during this economic shock no property with only a purchase money mortgage had a negative equity. Thus, all these owners with payment issues had equity to protect. The good part is most still do in 2026 as prices have remained flat and not yet, at mid-year, dropped.

This contributed to record-low levels of for-sale inventory during 2021 which rippled through California producing a 33% increase in home prices within 12 months.

Without government-backed housing relief, the only cure available to a mortgaged homeowner who slips underwater is strategic default. Cramdown provisions in the bankruptcy code to reduce mortgage debt for homeowners was eliminated in 2005. This was an attempt to keep negative equity homeowners paying their government insured mortgages so Fannie Mae and Freddie Mac do not become insolvent, which happened anyway.

Related article:

California’s for sale inventory: a symptom of seller reluctance in 2023

Negative equity in the years ahead

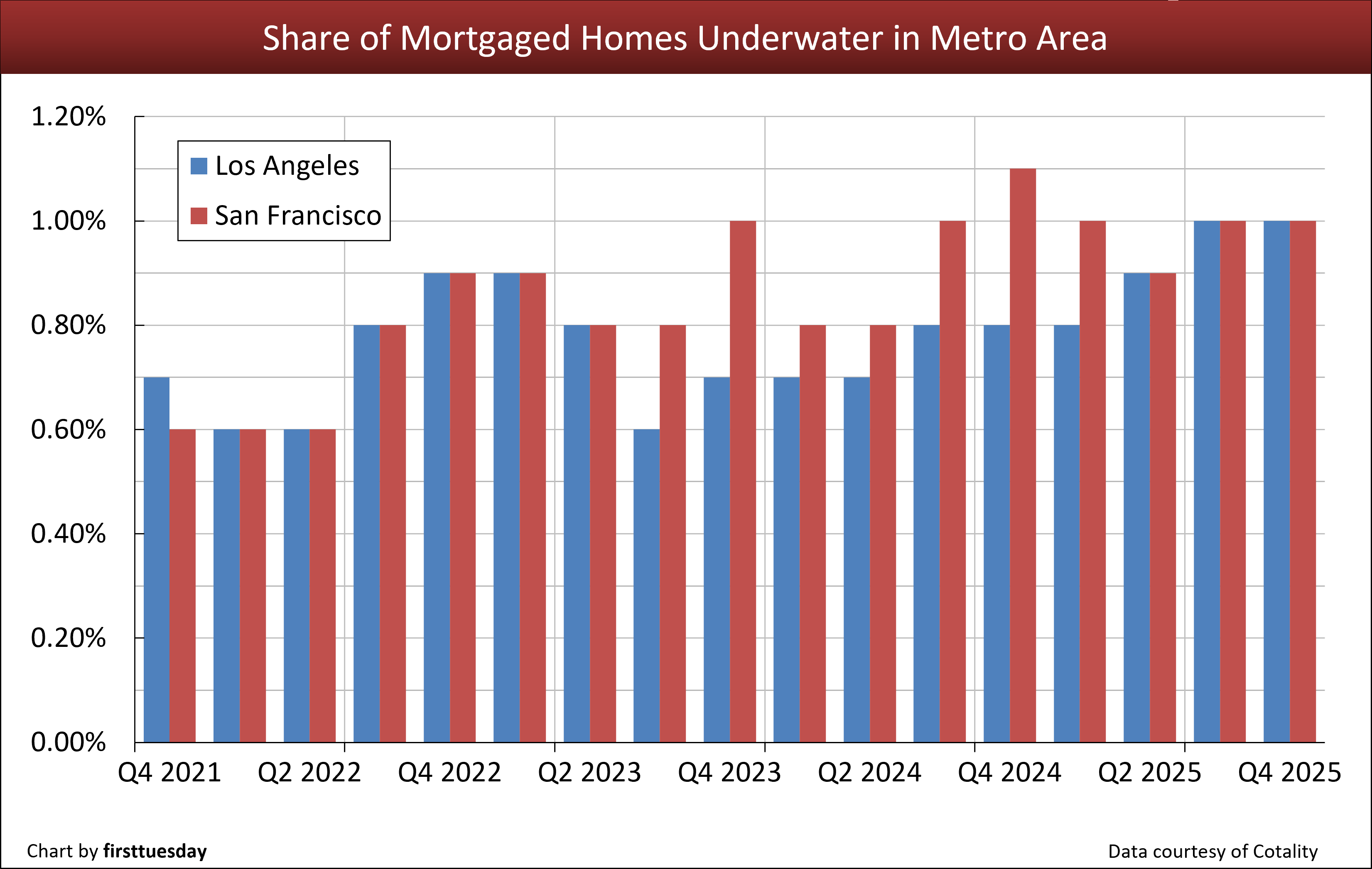

Chart 2

Chart update 5/20/26

| Q4 2025 | Q4 2024 | Annual Change | |

| Percentage of Los Angeles homes with negative equity | 1.0% | 0.8% | +25% |

| Percentage of San Francisco homes with negative equity | 1.0% | 1.1% | -9.1% |

The share of mortgaged homes with negative equity in California’s influential metro areas increased slightly in the years since early 2022 but are far below the national average. However, watch for this number to rise through 2026 and 2027 as the price decline resumes following.

For perspective, a whopping 37% of mortgaged California homeowners were underwater at the height of the foreclosure crisis in early 2010, two full years into the Great Recession and two years before prices recovered. Due to massive reregulation of mortgage lenders in 2010, mortgaged homeowners today have none of the predatorily deceptive aspects that fueled the dangerous millennium peak in 2005 and the financial collapse of 2007.

As home prices continue to contract over the next two-to-three years, watch for the share of underwater homes to rise rapidly, plunging anyone who purchased after 2021 with a minimal down payment a mortgage deep underwater.

Real estate agents can get ahead of rising owner need to sell by learning how to assist underwater homeowners. Gathering options for homeowners facing negative equity on top of their inability to pay or a need to move prepares agents to work with a larger share of clients in the inevitable down years ahead.

Stay on top of the latest market developments with firsttuesday.

Related video:

{kind=link}

Great read! Really insightful and well-written. Thank you for sharing such valuable thoughts — looking forward to your next article!

This article really resonates with me, especially the part about navigating negative equity during tough market shifts. I’ve experienced similar challenges in real estate, feeling stuck while trying to make sound decisions. It’s a daunting landscape, but sharing insights like these makes it a bit less lonely. Thank you!