California’s high home prices have lifted homeownership out of reach for the core residents of our communities. Teachers, first responders and even doctors are having a hard time finding homes in their budget.

In California, affordable housing has become harder to find over the past year, according to Trulia. That’s because even as wages have increased, California home prices have increased much faster, at a rate of:

- 11% in the low tier;

- 8% in the mid tier; and

- 8% in the high tier.

Trulia’s analysis assumes homebuyers:

- make the median wage for their industry in their region;

- have a 20% down payment;

- pay a 4.44% mortgage interest rate on a 30-year fixed rate mortgage (FRM);

- are willing to pay no more than 31% of their wages on housing; and

- include property taxes, insurance and any homeowners’ association (HOA) fees in their calculus to qualify.

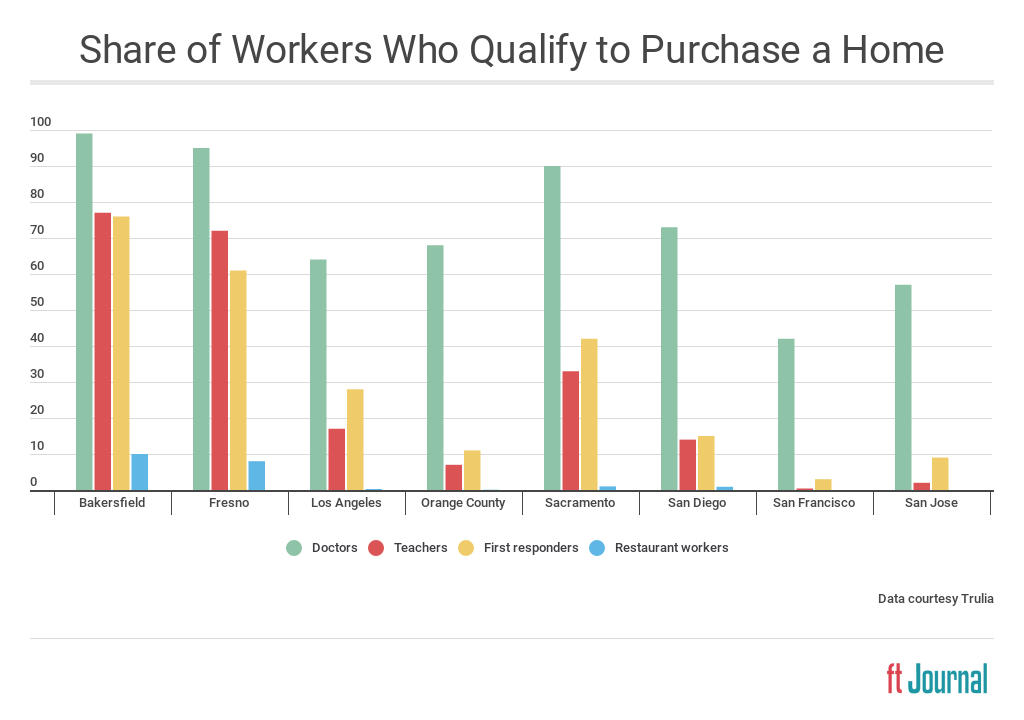

Trulia finds that in 2018, the percentage of workers who can qualify to purchase is:

No homes for restaurant workers

Restaurant workers by far have the hardest time finding homes within their wage-allocated budget in this list. Even in Bakersfield and Fresno, where housing is plentiful and homeownership is high, the percentage of restaurant workers who qualify to purchase is in or near the single digits.

Teachers also face challenges finding appropriate housing. It’s nearly impossible for a teacher’s salary to buy a home in pricey San Francisco and San Jose. But teachers who purchase jointly may be able to get around this norm if their spouse or other homebuying-partner brings extra income to the table.

Doctors and, to some extent, first responders, are most likely to be able to qualify for a home across California’s largest metros.

But therein lies the problem: a potential homebuyer shouldn’t need to have a doctor’s salary to become a homeowner. This metric excludes many responsible and earnest homebuyers from the housing market.

This problem for the housing market extends to real estate professionals — when fewer workers qualify to buy at today’s high prices, there are fewer transaction fees to go around.

The solution is ultimately the construction of more housing within the price range of most first-time homebuyers. When more low- and mid-tier housing is built, annual home price changes will slow to a pace in step with income increases.

Look to the next boom in construction for this to occur, expected to impact home sale and prices around 2020-2021. In the meantime, home prices are expected to slow briefly towards the end of 2018. But this will be due to higher interest rates, which pull back buyer purchasing power — not good for homebuyers reliant on mortgage financing. The longer-lasting reduction in prices won’t occur until more residential construction floods the market sufficient to cool off today’s runaway prices and encourage more would-be homebuyers to become homeowners.

Related article:

{kind=link}