This form is used by an escrow officer when, on behalf of an authorized person, escrow requests information from the holder of a mortgage on a property in sale or loan escrow to confirm the terms and conditions of the debt owed on the mortgage.

Mortgage debt information on request by escrow

When the seller under a purchase agreement has a mortgage lien on the property sold, escrow will need information on the mortgage so they can close escrow. To obtain mortgage information, a request for a beneficiary statement is made by escrow on the mortgage holder of record.

A beneficiary statement is a written disclosure made by a mortgage holder regarding the condition of a debt owed to them, usually evidenced by a note. With a mortgage, the debt is secured by a trust deed lien on the real estate described in the trust deed. [See RPI Form 415]

After receiving a request for a beneficiary statement, the mortgage holder states the terms for payment on the note and the amount necessary to pay a mortgage in full by preparing and delivering either a beneficiary statement or a payoff demand as requested. [CC §2943(d)(1)]

On escrow’s receipt of the beneficiary statement, it is relied upon in situations such as:

- a buyer of real estate takes title either subject to the mortgage or by an assumption, with or without a release of liability for the seller;

- a mortgage holder or other creditor receives a trust deed or other lien recorded as a junior encumbrance on the real estate; or

- a tenant acquires or encumbers a long-term leasehold interest in the real estate.

A complete beneficiary statement includes information and data regarding:

- the amount of the unpaid balance;

- the interest rate of the debt;

- the total of all overdue payments of principal and/or interest;

- the amounts of any periodic payments;

- the due date for final/balloon payoff of the debt;

- the date to which real estate taxes and special assessments have been paid, when known;

- the amount of hazard insurance and its term and premium, when known;

- any impound balance reserve for the payment of taxes and insurance;

- the amount of any additional charges incurred by the beneficiary that have become part of the mortgage; and

- whether it is possible for the mortgage to be assumed by a new owner. [See RPI Form 415; CC §2943(a)(2)]

When delivering a beneficiary statement, the mortgage holder also provides a copy of the note or other evidence of the debt, including any modifications. [CC §2943(b)(1)]

However, the statutory scheme controlling beneficiary statements does not require that a payoff demand include delivery of a copy of the note.

Statements for an ARM obligation

On adjustable rate mortgages (ARMs), the beneficiary statement needs to list the note rate as adjustable and reference the rate formula.

Formulas for ARM adjustments and payment options vary extensively from mortgage to mortgage. Thus, the seller or buyer relying on the beneficiary statement for an ARM needs greater detail than the current interest rate and payment amount. To that end, the mortgage holder attaches a copy of the ARM note to the beneficiary statement for full disclosure of the index used to calculate the periodic adjustments with the margin which comprise the note rate.

Requesting a statement

A mortgage holder responds to a written request for a beneficiary statement only when made by an entitled person. An entitled person includes:

- the property owner who entered into the mortgage;

- the successor-in-interest (new property owner) to the person who originally entered into the mortgage;

- any junior mortgage holder; and

- the authorized agent of an entitled person, such as an escrow agent, real estate broker or attorney. [CC §2943(a)(4)]

An entitled person who does not specifically request a beneficiary statement allows the mortgage holder to send only a payoff demand statement. [CC §2943(e)(1)]

The request for either statement needs to be in writing and delivered to the mortgage holder by:

- mail, at the address given in the payment notice or payment book; or

- fax. [CC §§2943(a)(3), 2943(e)(5)]

Before the mortgage holder delivers the beneficiary statement or payoff demand, they may require proof the request is being made by an entitled person — proof of ownership or other authority. Accordingly, a written request from an escrow officer is delivered with the escrow’s written authorization to order a statement signed by the entitled person. [CC §2943(e)(3)]

Further, any oral amendment by the mortgage holder to either the beneficiary statement or the payoff demand statement requires the mortgage holder to deliver a written amendment by the next business day. Entitled persons may rely on an amended statement to establish, prorate and adjust payoff amounts for closing. [CC §§2943(d)(1), 2943(d)(2)]

However, any error in a statement regarding the amount owed the mortgage holder becomes the unsecured debt of the person named in the original note once:

- escrow closes;

- title is transferred; or

- a trust deed is recorded. [CC §2943(d)(3)(A)]

When the statement from a mortgage holder is amended prior to the close of escrow or a trustee’s sale, the amounts listed in the amended statement control, whether the statement is a payoff demand or a beneficiary statement. [CC §2943(d)(3)(B)]

Timely delivery required of mortgage holder

Delivery of a beneficiary statement by the holder of any type of mortgage is to be made within 21 days of their receipt of the written request from an entitled person. [CC §2943(b)(1)]

The mortgage holder may not charge more than $30 for each beneficiary statement, with the exception of mortgages insured by the Federal Housing Administration (FHA) or the U.S. Department of Veterans Affairs (VA). Occasionally, the trust deed states a lesser amount which then controls the charge. [CC §2943(e)(6)]

When a request for either a beneficiary statement or a payoff demand includes a request for a copy of the trust deed, the mortgage holder needs to supply copies of the document at no extra charge. [CC §2943(e)(2)]

The mortgage holder’s intentional failure to send the statement within 21 days of receipt of request results in the mortgage holder’s forfeiture of $300 to the person making the request. Also, the mortgage holder is liable for all money losses resulting from its intentional failure to comply. [CC §2943(e)(4)]

However, the mortgage holder’s failure to timely deliver the statement must be an intentional failure without legal excuse before the entitled person making the request may recover a penalty — a very difficult burden.

Requests received during the foreclosure process

The request for a beneficiary statement or payoff demand statement may be made at any time up to two months after the recording of a notice of default (NOD). During this time, the mortgage holder is obligated to respond. [CC §2943(b)(2)]

When the mortgage is in foreclosure, an entitled person may request a payoff demand until the publishing of:

- the notice of trustee’s sale (NOTS) in a nonjudicial foreclosure; or

- the notice of sale in a judicial foreclosure. [CC §2943(c)]

However, part of complying with the foreclosure process requires the mortgage holder to provide the owner-in-foreclosure with an accounting of the exact amount due to reinstate or fully satisfy the mortgage.

Procedurally, the recorded NOD states the beneficiary will provide the owner-in-foreclosure with accurate information in response to the owner’s written request to determine the exact amount to be paid to stop the foreclosure. [CC §2924c(b)(1)]

Consider a beneficiary statement or payoff demand that is requested after an NOD is recorded, and the mortgage is not reinstated or paid in full. When an error exists in the amount requested and the property is sold at a foreclosure sale for a price based on the error, the amount of the error becomes the unsecured obligation of the payor on the note on completion of the foreclosure sale. [CC §2943(d)(3)(B)]

Also, once the mortgage holder is tendered the amount demanded to pay off the debt, the omitted amounts become unsecured. The owner originally signing the note remains liable for the unpaid amount which is now unsecured and payable on the terms set forth in the note. [CC §2943(d)(3)]

The mortgage holder may enforce collection without first foreclosing since the security has been reconveyed.

Analyzing the beneficiary statement

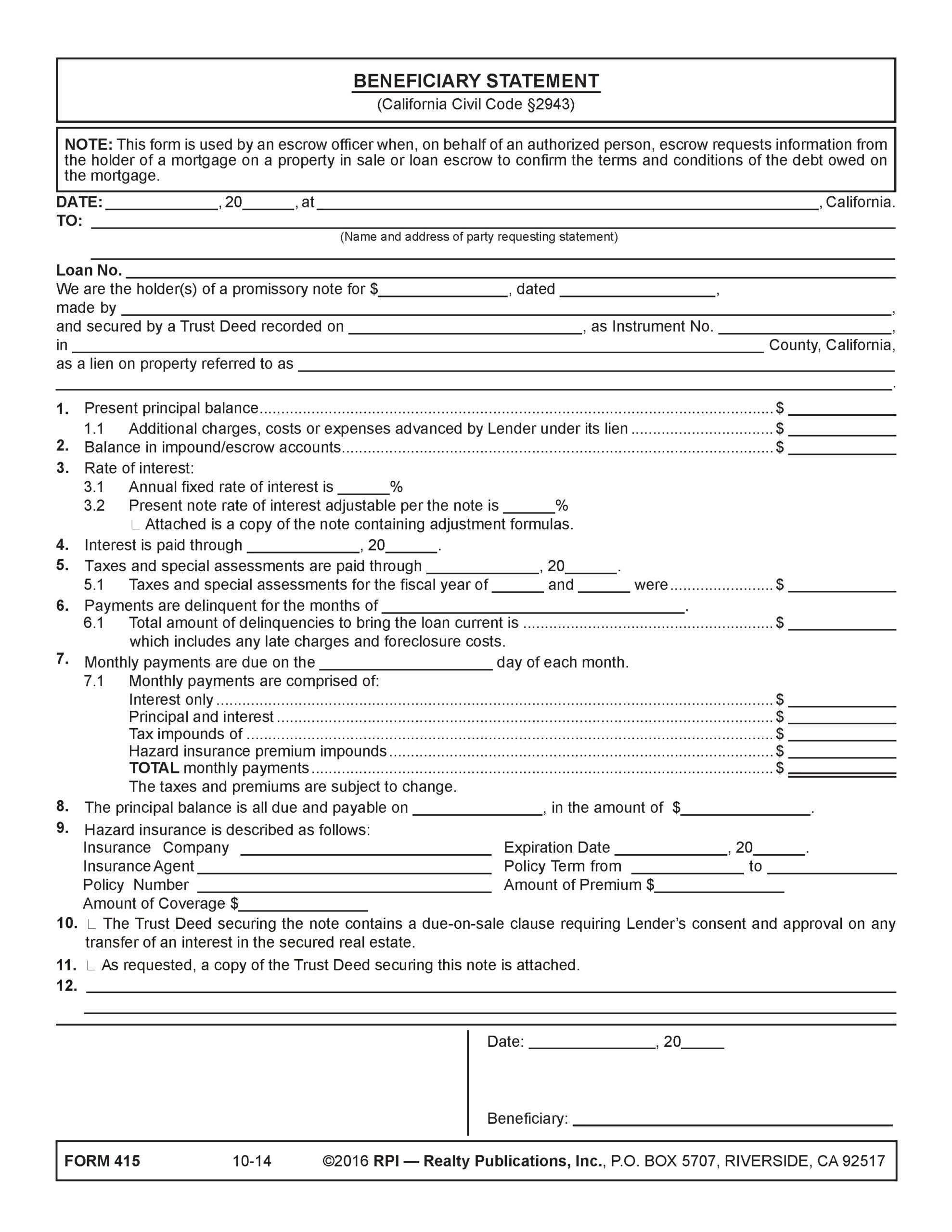

An escrow officer uses the Beneficiary Statement published by RPI when escrow on behalf of an authorized person requests information from a mortgage holder in a property sale or loan escrow to confirm the terms and conditions of the debt owed on the mortgage. [See RPI Form 415]

The Beneficiary Statement contains:

- the date [See RPI Form 415];

- the name and address of the principal requesting the beneficiary statement [See RPI Form 415];

- the mortgage loan number [See RPI Form 415];

- the promissory note amount and date, who owns it, the date the trust deed was recorded, the instrument number, the county where the relevant real estate is located, and the property address or description [See RPI Form 415];

- the present principal balance [See RPI Form 415 §1];

- additional charges, costs or expenses advanced by the lender under its lien [See RPI Form 415 §1.1];

- balance in impound/escrow accounts [See RPI Form 415 §2];

- the annual fixed rate of interest [See RPI Form 415 §3.1];

- the present note rate of interest adjustable per the note [See RPI Form 415 §3.2];

- what date interest is paid through [See RPI Form 415 §4];

- what date taxes and special assessments are paid through [See RPI Form 415 §5];

- the amount of taxes and special assessments for the previous two fiscal years [See RPI Form 415 §5.1];

- what month’s payments are delinquent [See RPI Form 415 §6];

- the total amount of delinquencies to bring the mortgage current [See RPI Form 415 §6.1];

- what day the monthly payments are due [See RPI Form 415 §7];

- monthly payments comprised of:

- interest only;

- principal and interest;

- tax impounds;

- hazard insurance premium impounds;

- total monthly payments [See RPI Form 415 §7.1];

- when the principal balance is due and how much is due [See RPI Form 415 §8];

- hazard insurance information [See RPI Form 415 §9];

- whether the trust deed contains a due-on clause [See RPI Form 415 §10];

- whether a copy of the trust deed securing the note is attached [See RPI Form 415 §11];

- blank (other provisions); and

- date and signature of the beneficiary. [See RPI Form 415]

Form navigation page published 07-2026.

Form last revised 2016.