Why this matters: An agent or escrow officer uses RPI Form 401 when preparing instructions to open a purchase escrow with an escrow officer, and RPI Form 415 when escrow requests mortgage information from a mortgage holder regarding their lien on a property to confirm the terms of the debt or obtain a payoff demand.

The execution of a purchase agreement

Escrow is a process employing an agent, called an escrow officer, acting independent of the principals in a transaction, to manage and coordinate the closing of a real estate transaction. The process includes the exchange of documents and money between two principals who must now complete a transaction they agreed to, such as a buyer and seller.

Escrow activities are typically based on an underlying primary agreement between the principals, such as a purchase agreement, option or exchange agreement. [Calif. Financial Code §17003(a)]

Escrow activity employed to close a real estate transaction consists of:

- principals, such as a seller and buyer of real estate, who deliver documents and money, collectively called instruments, to the escrow officer. The purpose served by the instruments is for each principal to fully perform their obligations owed to others under a prior primary agreement between the principals, such as a sale, mortgage origination or lease; and

- the escrow officer who receives documents and money for delivery to others, such as the buyer, seller and third parties, on the occurrence of a specified event or the clearance of conditions, such as the approval of reports or the issuance of a title insurance policy. [Fin C §17003(a)]

Related video:

Read more about the escrow process.

Escrow companies and escrow officers

An individual engaged in the business of acting as an escrow agent is called an escrow officer. The officer is employed by an escrow company and needs to be licensed. Likewise, the escrow company is licensed by the Department of Financial Protection and Innovation (DFPI), unless exempt. [Fin C §17200]

Individuals exempt from the escrow licensing requirements when performing escrow activities include:

- a licensed real estate broker, either individual or corporate, who represents a person in the real estate transaction while the broker is providing escrow services;

- a licensed attorney who does not hold themselves out as an escrow agent;

- a bank, trust company or insurance company; and

- a title insurance company whose principal business is preparing abstracts or conducting title searches used for issuing title insurance policies. [Fin C §17006]

The services rendered by the escrow officer typically include:

- receiving funds and collecting necessary documents, such as property reports, disclosure statements and title reports called for in the escrow instructions [See RPI Form 401];

- preparing or obtaining documents necessary for conveyancing and mortgaging a property required for escrow to close;

- calculating prorations and adjustments; and

- disbursing funds and transferring documents on a closing when all conditions for their release have been met. [Fin C §17003(a)]

The specific duties of the escrow officer, outlined in the escrow instructions, vary according to local real estate custom. [See RPI Form 401]

Related video:

Read more about escrow companies.

Escrow instructions

An escrow officer performs only as instructed and follows instructions strictly with full performance. Escrow instructions are generally prepared by the escrow officer based on the information received from one of the transaction agents about the agreement between the principals. [See RPI Form 401]

In practice, the escrow officer preparing their instructions use forms designed for this purpose. Once completed, the instructions are forwarded to the agents of the principals in the transaction for their signatures and returned to escrow. When returned, escrow is then open for the person who signed and returned the instructions.

Two types of escrow instructions are used in California:

- bilateral; and

- unilateral

Throughout most of California, escrow instructions used in real estate sales transactions are bilateral. When escrow instructions are bilateral, the copies of the single set of instructions are signed by the buyer and seller and handed to escrow. [See RPI Form 401]

In some areas of Northern California, separate sets of unilateral escrow instructions are prepared, usually written up when the transaction is ready to close. Each set of instructions contain only the activities to be performed by or on behalf of one principal; one set as the buyer’s instructions, the other set the seller’s instructions. When escrow determines it has all documents necessary to call for funding and closing the transaction, only then does the officer prepare the separate instructions for signatures of the respective buyers and sellers.

Related video:

Read more about escrow instructions.

The documents work together

Today’s real estate sales transactions depend on both the purchase agreement and the escrow instructions working in tandem and are entered into to document the purchase agreement and to close the transaction.

Both the purchase agreement and the escrow instructions are contracts regarding interests in real estate. Both documents are written as required for enforcement under the Statute of Frauds. [Calif. Civil Code §1624]

A purchase agreement sets forth the:

- sales price;

- terms of payment; and

- conditions to be met before closing. [See RPI Form 150]

Escrow instructions constitute an additional agreement, contemplated by the purchase agreement, entered into by the buyer and seller with an escrow company. As instructed, escrow facilitates the completion of the performance required of the buyer and seller in their purchase agreement.

Escrow instructions do not replace the purchase agreement. Instead, the instructions function as directives an escrow officer follows to coordinate a closing intended by the terms of the purchase agreement. [Claussen v. First American Title Guaranty Co. (1986) 186 CA3d 429]

Escrow instructions occasionally add exactness and completeness, providing the enforceability sometimes lacking in purchase agreements prepared by brokers or their agents.

A written and signed purchase agreement typically is the primary document underlying a real estate sales transaction. All further agreements, including the escrow instructions, need to comply with the primary document, unless the parties intend to modify the terms of that original agreement.

The agents negotiating a transaction are responsible for ensuring the escrow instructions prepared by the escrow officer conform to the purchase agreement. Thus, each transaction agent reviews the instructions prepared by the escrow officer to ensure the intentions of the buyer and seller are clear. Their review takes place prior to submitting instructions to their clients for review and signatures.

In some instances, or principal to principal agreements to buy and sell a property, the transaction is orally negotiated, and the principals go directly to escrow. In this case, they do not first memorialize their negotiations in a written purchase agreement. Here, no primary written purchase agreement is generated prior to opening escrow.

Further, the escrow instructions now function as the binding contract documenting the sale as it is the only written agreement signed by the principals. While the instructions provide for performance and closing of the agreement between the principals, the written escrow instructions constitute a binding contract between the buyer and seller, satisfying the Statute of Frauds permitting enforcement. [Amen v. Merced County Title Co. (1962) 58 C2d 528]

To provide for a timely closing, the transaction agents collect and hand to the escrow officer all the information necessary to prepare documents for closing.

Related video:

Read more about the purchase agreement and escrow.

Modifying escrow instructions

When a dispute between the buyer and seller arises over a point not addressed in the purchase agreement or escrow instructions, the agents need to mediate an agreeable solution.

The negotiated resolution is added to the escrow instructions by an amendment signed by the buyer and the seller. Signed amended instructions bind the buyer and seller to the terms agreed to in the amended instructions as part of their contractual obligations in the transaction. [U.S. Hertz, Inc. v. Niobara Farms (1974) 41 CA3d 68]

Escrow instructions which modify the intentions stated or implied in the purchase agreement need to be written, signed and returned to escrow by both the buyer and seller. Proposed modifications signed by some but not all principals are not binding on a principal who has not agreed to the modifications. [Louisan v. Vohanan (1981) 117 CA3d 258]

Related video:

Read more about escrow amendments.

Mortgage debt information on request by escrow

When the seller under a purchase agreement has a mortgage lien on the property sold, escrow will need information on the mortgage so they can close escrow. To obtain mortgage information, a request for a beneficiary statement is made by escrow on the mortgage holder of record.

A beneficiary statement is a written disclosure made by a mortgage holder regarding the condition of a debt owed to them, usually evidenced by a note. With a mortgage, the debt is secured by a trust deed lien on the real estate described in the trust deed. [See RPI Form 415]

After receiving a request for a beneficiary statement, the mortgage holder states the terms for payment on the note and the amount necessary to pay a mortgage in full by preparing and delivering either a beneficiary statement or a payoff demand as requested. [CC §2943(d)(1)]

On escrow’s receipt of the beneficiary statement, it is relied upon in situations such as:

- a buyer of real estate takes title either subject to the mortgage or by an assumption, with or without a release of liability for the seller;

- a mortgage holder or other creditor receives a trust deed or other lien recorded as a junior encumbrance on the real estate; or

- a tenant acquires or encumbers a long-term leasehold interest in the real estate.

A complete beneficiary statement includes information and data regarding:

- the amount of the unpaid balance;

- the interest rate of the debt;

- the total of all overdue payments of principal and/or interest;

- the amounts of any periodic payments;

- the due date for final/balloon payoff of the debt;

- the date to which real estate taxes and special assessments have been paid, when known;

- the amount of hazard insurance and its term and premium, when known;

- any impound balance reserve for the payment of taxes and insurance;

- the amount of any additional charges incurred by the beneficiary that have become part of the mortgage; and

- whether it is possible for the mortgage to be assumed by a new owner. [See RPI Form 415; CC §2943(a)(2)]

When delivering a beneficiary statement, the mortgage holder also provides a copy of the note or other evidence of the debt, including any modifications. [CC §2943(b)(1)]

However, the statutory scheme controlling beneficiary statements does not require that a payoff demand include delivery of a copy of the note.

Statements for an ARM obligation

On adjustable rate mortgages (ARMs), the beneficiary statement needs to list the note rate as adjustable and reference the rate formula.

Formulas for ARM adjustments and payment options vary extensively from mortgage to mortgage. Thus, the seller or buyer relying on the beneficiary statement for an ARM needs greater detail than the current interest rate and payment amount. To that end, the mortgage holder attaches a copy of the ARM note to the beneficiary statement for full disclosure of the index used to calculate the periodic adjustments with the margin which comprise the note rate.

Related video:

Read more about ARMs.

Requesting a statement

A mortgage holder responds to a written request for a beneficiary statement only when made by an entitled person. An entitled person includes:

- the property owner who entered into the mortgage;

- the successor-in-interest (new property owner) to the person who originally entered into the mortgage;

- any junior mortgage holder; and

- the authorized agent of an entitled person, such as an escrow agent, real estate broker or attorney. [CC §2943(a)(4)]

An entitled person who does not specifically request a beneficiary statement allows the mortgage holder to send only a payoff demand statement. [CC §2943(e)(1)]

The request for either statement needs to be in writing and delivered to the mortgage holder by:

- mail, at the address given in the payment notice or payment book; or

- fax. [CC §§2943(a)(3), 2943(e)(5)]

Before the mortgage holder delivers the beneficiary statement or payoff demand, they may require proof the request is being made by an entitled person — proof of ownership or other authority. Accordingly, a written request from an escrow officer is delivered with the escrow’s written authorization to order a statement signed by the entitled person. [CC §2943(e)(3)]

Further, any oral amendment by the mortgage holder to either the beneficiary statement or the payoff demand statement requires the mortgage holder to deliver a written amendment by the next business day. Entitled persons may rely on an amended statement to establish, prorate and adjust payoff amounts for closing. [CC §§2943(d)(1), 2943(d)(2)]

However, any error in a statement regarding the amount owed the mortgage holder becomes the unsecured debt of the person named in the original note once:

- escrow closes;

- title is transferred; or

- a trust deed is recorded. [CC §2943(d)(3)(A)]

When the statement from a mortgage holder is amended prior to the close of escrow or a trustee’s sale, the amounts listed in the amended statement control, whether the statement is a payoff demand or a beneficiary statement. [CC §2943(d)(3)(B)]

Timely delivery required of mortgage holder

Delivery of a beneficiary statement by the holder of any type of mortgage is to be made within 21 days of their receipt of the written request from an entitled person. [CC §2943(b)(1)]

The mortgage holder may not charge more than $30 for each beneficiary statement, with the exception of mortgages insured by the Federal Housing Administration (FHA) or the U.S. Department of Veterans Affairs (VA). Occasionally, the trust deed states a lesser amount which then controls the charge. [CC §2943(e)(6)]

When a request for either a beneficiary statement or a payoff demand includes a request for a copy of the trust deed, the mortgage holder needs to supply copies of the document at no extra charge. [CC §2943(e)(2)]

The mortgage holder’s intentional failure to send the statement within 21 days of receipt of request results in the mortgage holder’s forfeiture of $300 to the person making the request. Also, the mortgage holder is liable for all money losses resulting from its intentional failure to comply. [CC §2943(e)(4)]

However, the mortgage holder’s failure to timely deliver the statement must be an intentional failure without legal excuse before the entitled person making the request may recover a penalty — a very difficult burden.

Requests received during the foreclosure process

The request for a beneficiary statement or payoff demand statement may be made at any time up to two months after the recording of a notice of default (NOD). During this time, the mortgage holder is obligated to respond. [CC §2943(b)(2)]

When the mortgage is in foreclosure, an entitled person may request a payoff demand until the publishing of:

- the notice of trustee’s sale (NOTS) in a nonjudicial foreclosure; or

- the notice of sale in a judicial foreclosure. [CC §2943(c)]

However, part of complying with the foreclosure process requires the mortgage holder to provide the owner-in-foreclosure with an accounting of the exact amount due to reinstate or fully satisfy the mortgage.

Procedurally, the recorded NOD states the beneficiary will provide the owner-in-foreclosure with accurate information in response to the owner’s written request to determine the exact amount to be paid to stop the foreclosure. [CC §2924c(b)(1)]

Consider a beneficiary statement or payoff demand that is requested after an NOD is recorded, and the mortgage is not reinstated or paid in full. When an error exists in the amount requested and the property is sold at a foreclosure sale for a price based on the error, the amount of the error becomes the unsecured obligation of the payor on the note on completion of the foreclosure sale. [CC §2943(d)(3)(B)]

Also, once the mortgage holder is tendered the amount demanded to pay off the debt, the omitted amounts become unsecured. The owner originally signing the note remains liable for the unpaid amount which is now unsecured and payable on the terms set forth in the note. [CC §2943(d)(3)]

The mortgage holder may enforce collection without first foreclosing since the security has been reconveyed.

Related article:

Analyzing the escrow instructions

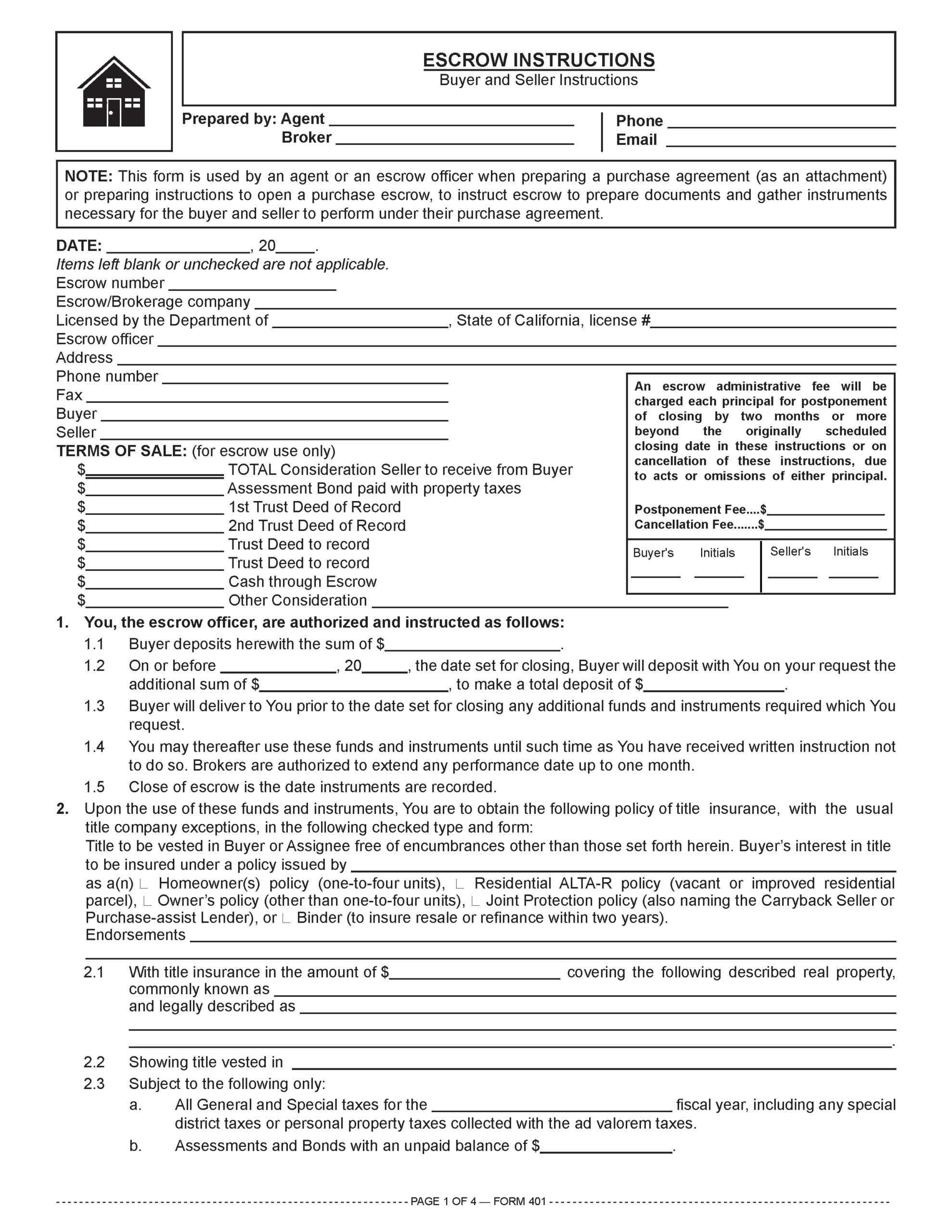

An agent or escrow officer uses the Escrow Instructions published by Realty Publications, Inc. (RPI) when preparing a purchase agreement (as an attachment) or preparing separate instructions to open a purchase escrow. The form instructs the escrow officer to gather instruments and draft documents necessary for the buyer and seller to perform under their purchase agreement so escrow can close. [See RPI Form 401]

The Escrow Instructions contains:

- basic information, including the:

- date;

- escrow number;

- escrow/brokerage company;

- department issuing a license;

- license number;

- escrow officer;

- address;

- phone number;

- fax; and

- buyer and seller identities [See RPI Form 401];

- terms of sale, including:

- the total consideration seller is to receive from the buyer;

- assessment bond paid with property taxes;

- first trust deed of record;

- second trust deed of record;

- trust deed(s) to record;

- cash through escrow; and

- other consideration [See RPI Form 401]

- buyer and seller initials regarding postponement and cancellation fees;

- the buyer’s deposit [See RPI Form 401 §1.1];

- the closing date and total deposits due on closing [See RPI Form 401 §1.2];

- the title insurance to be used and any endorsements [See RPI Form 401 §2];

- the amount of the title insurance, and the common and legal addresses of the real estate [See RPI Form 401 §2.1];

- how the title is vested [See RPI Form 401 §2.2];

- the sale is subject to the following:

- the fiscal year for which taxes apply [See RPI Form 401 §2.3(a)];

- unpaid assessment and bond amounts [See RPI Form 401 §2.3(b)];

- first and second encumbrances and their unpaid balances, monthly amounts and annual interest rates [See RPI Form 401 §§2.3(d) and (e)];

- trust deed amount(s) [See RPI Form 401 §§2.3(f) and (g)];

- trust deed with assignment of rents amount, including annual interest, monthly installment amounts, commencement and end dates and address for delivery of note payments [See RPI Form 401 §2.3(h)];

- beneficiary statements the escrow officer obtains at the seller’s expense for any existing trust deed liens [See RPI Form 401 §3];

- whether the escrow officer obtains a UCC-3 clearance on personal property, listed here and UCC-1 financing statement information, when applicable [See RPI Form 401 §4];

- a checkbox indicating the seller has handed the escrow officer a structural pest control clearance [See RPI Form 401 §6];

- a homeowner’s warranty policy information [See RPI Form 401 §7];

- when the home is located in a homeowners’ association (HOA), whether the buyer received:

- a statement of condition of assessments;

- copies of the association articles, bylaws, CC&Rs, collection and lien enforcement policies, operating rules, CPA’s financial review, insurance policy summary and any age restriction statement; and

- copies from the association of any notice to seller of CC&R violations, any list of construction defects, and any assessment charges not yet payable [See RPI Form 401 §8];

- whether there are any assignments for existing lease/rental agreements [See RPI Form 401 §9];

- prorations and adjustments to be computed by the escrow officer on a monthly basis, including:

- taxes;

- hazard (fire) insurance premium;

- interest on existing note(s) and trust deed(s);

- rents and deposits;

- impounds;

- HOA assessments; and

- other [See RPI Form 401 §10];

- the amount of time the buyer has to approve or disapprove and cancel the transaction based on conditions in the preliminary title report on the property from a title company [See RPI Form 401 §11];

- the address in space provided on the grant deed for mailing tax statements [See RPI Form 401 §12];

- the purchase agreement and counteroffer date the escrow instructions are based on [See RPI Form 401 §13];

- items the seller is charged for, including:

- bonds, assessments, taxes and other liens of record to show title;

- documentary transfer taxes;

- broker fees;

- transaction coordinator fees;

- title insurance premium on the policy to be issued to the buyer;

- costs of recording the seller’s grant deed;

- escrow fees;

- payables submitted to escrow for payment by the seller or seller broker;

- attorney fees; and

- other [See RPI Form 401 §18];

- items the buyer is charged for, including:

- escrow fees;

- costs of and lender’s charges for recording or assuming any trust deeds, including a policy of title insurance for any new lender;

- attorney fees;

- broker fees;

- title insurance premium on the policy to be issued to the buyer; and

- other [See RPI Form 401 §19];

- a blank for listing miscellaneous provisions [See RPI Form 401 §20]; and

- signatures of the seller and buyer. [See RPI Form 401]

Related article:

Form-of-the-Week: Escrow Instructions and Sales Escrow Worksheet – Forms 401 and 403

Analyzing the beneficiary statement

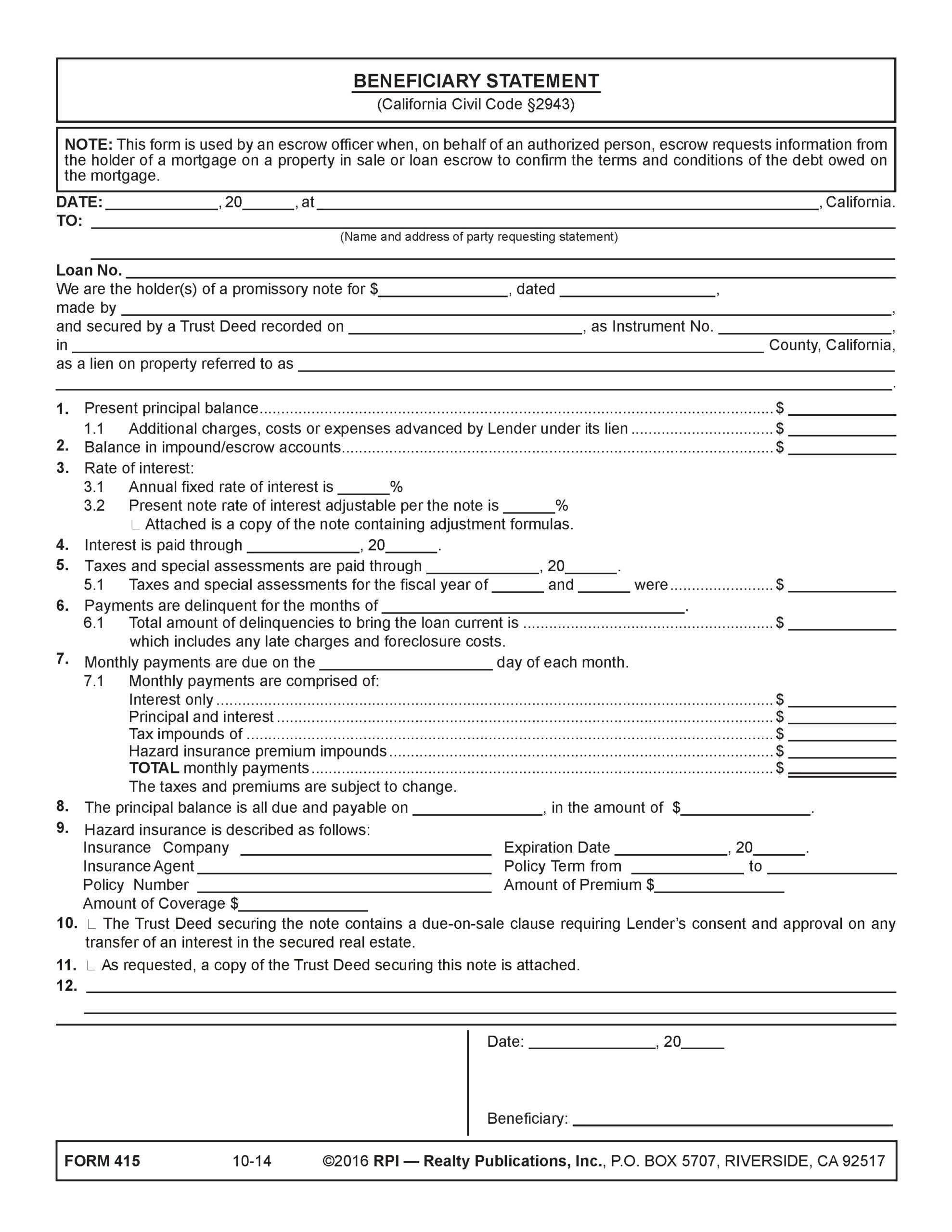

An escrow officer uses the Beneficiary Statement published by RPI when escrow on behalf of an authorized person requests information from a mortgage holder in a property sale or loan escrow to confirm the terms and conditions of the debt owed on the mortgage. [See RPI Form 415]

The Beneficiary Statement contains:

- the date [See RPI Form 415];

- the name and address of the principal requesting the beneficiary statement [See RPI Form 415];

- the mortgage loan number [See RPI Form 415];

- the promissory note amount and date, who owns it, the date the trust deed was recorded, the instrument number, the county where the relevant real estate is located, and the property address or description [See RPI Form 415];

- the present principal balance [See RPI Form 415 §1];

- additional charges, costs or expenses advanced by the lender under its lien [See RPI Form 415 §1.1];

- balance in impound/escrow accounts [See RPI Form 415 §2];

- the annual fixed rate of interest [See RPI Form 415 §3.1];

- the present note rate of interest adjustable per the note [See RPI Form 415 §3.2];

- what date interest is paid through [See RPI Form 415 §4];

- what date taxes and special assessments are paid through [See RPI Form 415 §5];

- the amount of taxes and special assessments for the previous two fiscal years [See RPI Form 415 §5.1];

- what month’s payments are delinquent [See RPI Form 415 §6];

- the total amount of delinquencies to bring the mortgage current [See RPI Form 415 §6.1];

- what day the monthly payments are due [See RPI Form 415 §7];

- monthly payments comprised of:

- interest only;

- principal and interest;

- tax impounds;

- hazard insurance premium impounds;

- total monthly payments [See RPI Form 415 §7.1];

- when the principal balance is due and how much is due [See RPI Form 415 §8];

- hazard insurance information [See RPI Form 415 §9];

- whether the trust deed contains a due-on clause [See RPI Form 415 §10];

- whether a copy of the trust deed securing the note is attached [See RPI Form 415 §11];

- blank (other provisions); and

- date and signature of the beneficiary. [See RPI Form 415]

{kind=link}