This form is used by a buyer broker when preparing an offer for their buyer-client to purchase an interest in one-to-four unit residential property with short sale contingency provisions.

Conventional foreclosure

Foreclosure is a procedure to recover the amounts owed on a mortgage debt in default through an orderly sale of property pledged as security for the debt. The foreclosure process is triggered by a default in payment or a breach of trust deed terms relating to the property.

A mortgage holder or carryback seller holding a note secured by a trust deed in default has two foreclosure methods available, the only methods to enforce collection of the secured debt. These two foreclosure methods are:

- a judicial foreclosure sale, also called a sheriff’s sale [Calif. Code of Civil Procedure §726]; or

- a nonjudicial foreclosure sale, also called a trustee’s sale. [Calif. Civil Code §2924]

The key to the mortgage holder’s ability to nonjudicially foreclosure by a trustee’s sale on the mortgaged real estate is the power-of-sale provision contained in the mortgage trust deed document.

By foreclosing under the trust deed’s power-of-sale provision, the mortgage holder avoids a costly (and potentially time consuming) court action for judicial foreclosure.

Alternatives to foreclosure

A homeowner in default on their mortgage has alternatives to foreclosure.

Alternatives to foreclosure that may be more favorable for a homeowner include negotiating a:

- mortgage forbearance;

- loan modification;

- conventional sale;

- short sale; and

- deed-in-lieu of foreclosure.

A mortgage forbearance occurs when a mortgage holder agrees to temporarily forego proceeding with their collection efforts, such as canceling a trustee’s foreclosure. During the forbearance period, the property owner takes steps to bring the mortgage payments current.

A loan modification occurs when the mortgage holder agrees to change the terms of the note documenting the mortgage debt. The note itself is not cancelled or newly rewritten since the debt it documents is secured by a trust deed which references the note.

A conventional sale of the property is the most common alternative to foreclosure as the mortgage is paid off using the owner’s sales proceeds.

However, when the property’s value is less than the mortgage amount, the owner’s sale of the property is called a short sale or non-conventional sale.

Short sales become common during recessions. During the Great Recession of 2008-2009, roughly 25% of California multiple listing service (MLS) sales transactions were short sales.

Following the Great Recession, California home prices peaked in 2022. Since then, prices bounced on a flat plateau of pricing which held until 2026 when prices started to decline.

Prices will continue to retract in the years ahead. This means anyone who purchased with a minimal down payment in 2019-2022 will slip underwater. For owners needing to sell property with a value less than the mortgage debt, they will either find a buyer and negotiate a short sale or default and force the lender to acquire it as real estate owned (REO) at a trustee’s sale.

Short sale

To dispose of a property in a short sale, the owner negotiates with the mortgage holder to accept the net proceeds from a sale of the property in full satisfaction of the greater amount of debt owed. To start the process, the property owner hires a real estate agent to market their property for sale.

The benefits of a short sale are twofold:

- for the mortgage holder, a short sale saves money as the process is quicker and often the payoff received is greater than bidders will pay at a foreclosure sale, or later when sold as REO by the mortgage holder; and

- for the property owner, a short sale usually results in less harm done to their credit score. Also, they avoid any “moral shame” they may feel from a foreclosure (though financially the short sale result is nearly the same since the owner retains possession rent free until the foreclosure sale).

Still, a short sale results in the property owner no longer retaining the property. On a recourse mortgage in a short sale (such as with a commercial property or a home equity mortgage), they are also dealing with the mortgage holder reporting discharge of indebtedness income to the taxing authorities.

To qualify for a short sale, the homeowner needs to:

- be delinquent on their mortgage payments;

- owe more on their mortgage than their property is worth; and

- be unable to pay their mortgage.

Purchase agreement contingency in a short sale

Especially in recessionary times, a buyer broker may encounter a seller seeking an unconventional sale when the property is underwater — meaning the mortgage balance exceeds market value.

In response to this scenario, a buyer broker submits a purchase agreement on behalf of their buyer containing a short sale contingency provision. Thus, the close of escrow is conditioned on the seller arranging a short sale approval with their mortgage holder in full satisfaction of the debt. [See RPI Form 150-5]

The contingency states the agreement may be terminated by either the buyer or seller when the seller is unable to obtain written payoff demands and consent to the sale from the lienholders. [See RPI Form 150-5 §10.2]

The seller acknowledges a discount by the lienholder in full satisfaction of the debt owed has adverse consequences on the seller’s credit score and income taxes. [See RPI Form 150-5 §10.4]

Analyzing the purchase agreement with short sale contingency provisions

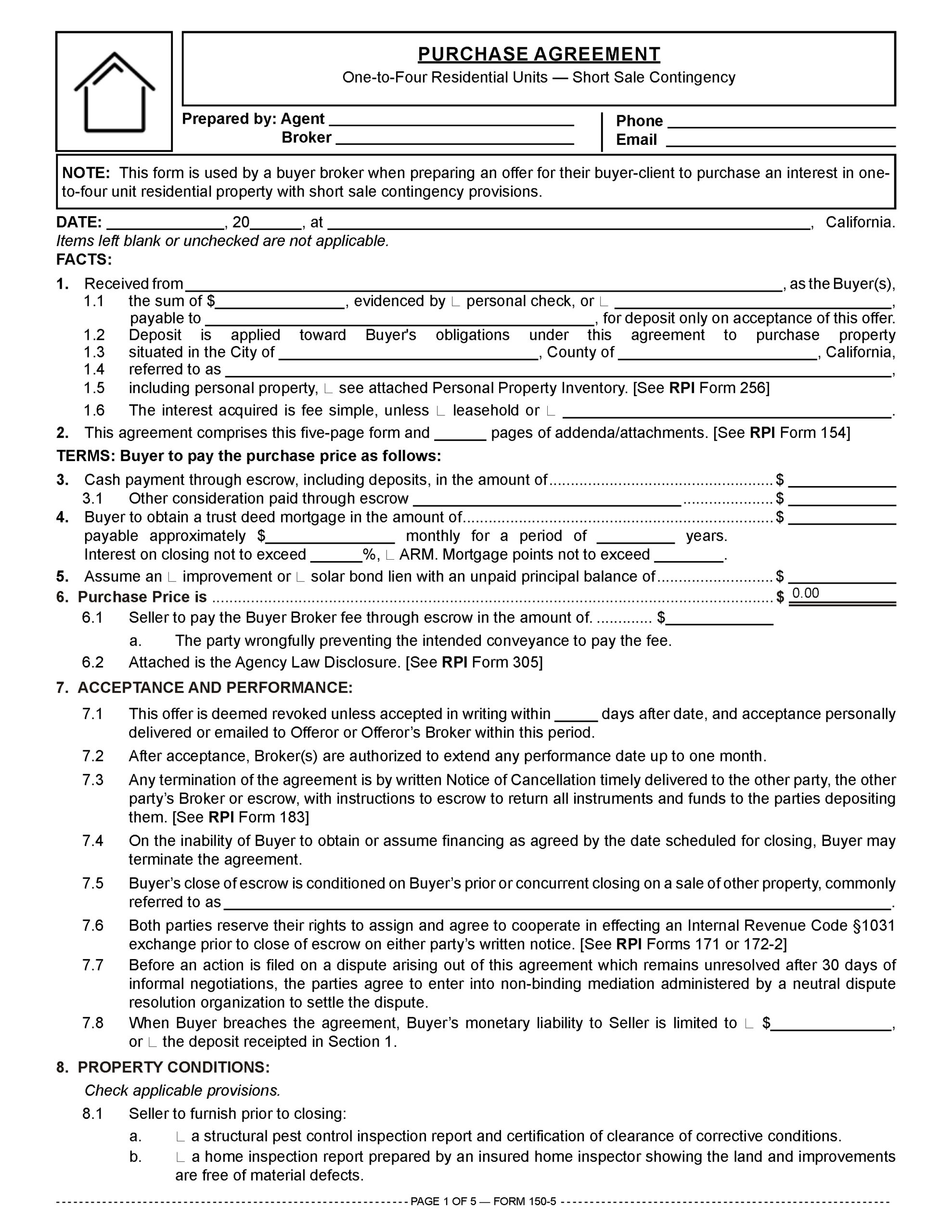

A buyer broker uses the Purchase Agreement — One-to-Four Residential Units — Short Sale Contingency published by Realty Publications, Inc. (RPI) when preparing an offer for their buyer-client to purchase an interest in a one-to-four unit residential property when short sale contingency provisions are needed. [See RPI Form 150-5]

The Purchase Agreement — One-to-Four Residential Units — Short Sale Contingency contains:

- Facts: the buyer’s name, the amount of the good-faith deposit, the property’s address and the type of ownership sought (fee simple, leasehold, etc.) [See RPI Form 150-5 §1];

- Terms: the down payment and mortgage amounts, the terms of the mortgage, the principal balance and monthly amount of the mortgage, any junior trust deeds, improvement bonds and solar bond liens [See RPI Form 150-5 §§3 through 5];

- Purchase price: the purchase price the buyer agrees to fund, with a provision for payment of the buyer broker fee out of the purchase price funds. Also attached is the Agency Law Disclosure [See RPI Form 305; See RPI Form 150-5 §6];

- Acceptance and performance: the amount of time for acceptance of the offer, a contingency provision for the sale of the buyer’s current residence when applicable, a mediation provision and any amount the seller is due on a buyer’s breach [See RPI Form 150-5 §7];

- Property conditions: indicates whether the seller agrees to provide:

- a structural pest control inspection report;

- a home inspection report;

- a home warranty policy;

- a certificate of occupancy;

- a certification by a licensed contractor stating the sewage disposal system is operational;

- a certification by a licensed water testing lab stating the well supplying the property meets potable standards;

- how many gallons a well on the property produces per minute, when applicable;

- an energy audit report; and

- the Transfer Disclosure Statement [See RPI Form 150-5 §8];

- Due diligence contingencies: a contingency provision for the buyer’s due diligence investigations into income and expense records, rental income statements, hazard disclosures, property condition disclosures and other relevant information the seller is to deliver are listed in an addendum for buyer consideration and checking those applicable to the agreement [See RPI Form 279; See RPI Form 150-5 §9];

- Short sale contingency: sale of the property is conditioned on seller obtaining a discounted payoff demand from each lienholder in full satisfaction of all amounts owed, backup offer agreement, seller acknowledgement of adverse effects on credit and taxes and the date of any notice of default recording [See RPI Form 150-5 §10];

- Closing conditions: the escrow company to be used, the date escrow is to close, any covenants, conditions and restrictions (CC&Rs) or easements on record, and the title company to issue a policy [See RPI Form 150-5 §11];

- Notices: regarding sales data, registered sex offenders, appraisal objectivity, gas and hazardous liquid pipelines and supplemental property tax bill [See RPI Form 150-5 §12];

- Blank: miscellaneous provisions not included elsewhere in the body of the form are listed here [See RPI Form 150-5 §13]; and

- Signatures of the buyer, their broker and agent, and a space for the seller, their broker and agent to enter their signatures, forming a contract. [See RPI Form 150-5]

Form navigation page published 04-2026.

Form updated 2025.

Form-of-the-Week: Purchase Agreement with Short Sale Contingency, and Deed-in-Lieu of Foreclosure — Forms 150-5 and 406

Form-of-the-Week: Purchase Agreement variations and their addenda

Form-of-the-Week: Purchase Agreement — for One-to-Four Residential Property — with Buyer Broker Fee Provision [RPI Form 150]

Real Estate, Explained: Short sales, explained

Article: Mortgage delinquencies lead to foreclosures

Article: MLO recession survival guide Part 2: Buyers’ agents and underwater home sellers

Chart: Negative equity and foreclosure

Client Q&A: What are a homeowner’s foreclosure alternatives?

FARM: Short sales: What you need to know

Video: The Power-of-Sale Provision