How will California’s economy affect the real estate market in 2013? Here’s the answer, in eight charts.

The economy in 2013

California real estate will gradually recover in 2013. This is due to ongoing, modest improvements in:

- employment;

- demographics;

- interest rates;

- construction starts;

- negative equity;

- distressed sales;

- home sales volume; and

- home pricing.

Each of these factors influences the quantity and quality of sales the average broker and agent will close in the year to come.

1. Jobs will slowly increase

The number of jobs in California directly impacts both home sales and rentals. With rare exception, individuals need a paycheck to rent or buy.

In 2013, employment numbers will continue on the slow route to full recovery. At the end of 2012, 14.5 million people were employed in California. This is 830,000 jobs below the December 2007 peak of 15.3 million. Once these jobs are recovered, another 1,000,000 jobs will be needed due to the intervening population growth.

When will a full jobs recovery occur? At the anticipated rate of 350,000 jobs added on a year-over-year basis during the coming years, the full recovery will occur in 2016. The good news is that California’s job market is doing better than the national job market: slow and steady is the trend for now and the future.

2. Demographics of demand: first-time homebuyers on the sidelines

Even as the number of would-be first-time homebuyers (aged 25-35 years) rises, California’s homeownership rate suffers.

Why hasn’t the increased number of young Californians increased the number of homeowners? This age group (Generation Y or Gen Y) has collectively been forced to put off dreams of homeownership due to high rates of unemployment, underemployment and heavy student debt.

At the same time, California’s population is swiftly becoming more educated. In the short-term, this negatively affects home sales, as first-time homebuyers put off homeownership while paying off their student debt. However, the next decade will bring a shift in housing demands due to the influx of highly-educated homeowners. Members of Gen Y will settle in urban areas, close to high-paying jobs and all the amenities city-living offers.

Gen Y will likely enter the housing market in full force in 2016 with the jobs recovery. They will mostly settle in cities, where the highest paying jobs are located. This will coincide with a housing shift for Baby Boomers, who will be retiring in earnest by this time. Boomers will often choose to be near to their city-bound children and grandchildren.

In the meantime, agents can focus their efforts on members of Gen Y with families, as they are more likely to buy or at least rent more expensive property. Begin building a presence in urban areas, as this is where both demographic groups will choose to buy or rent.

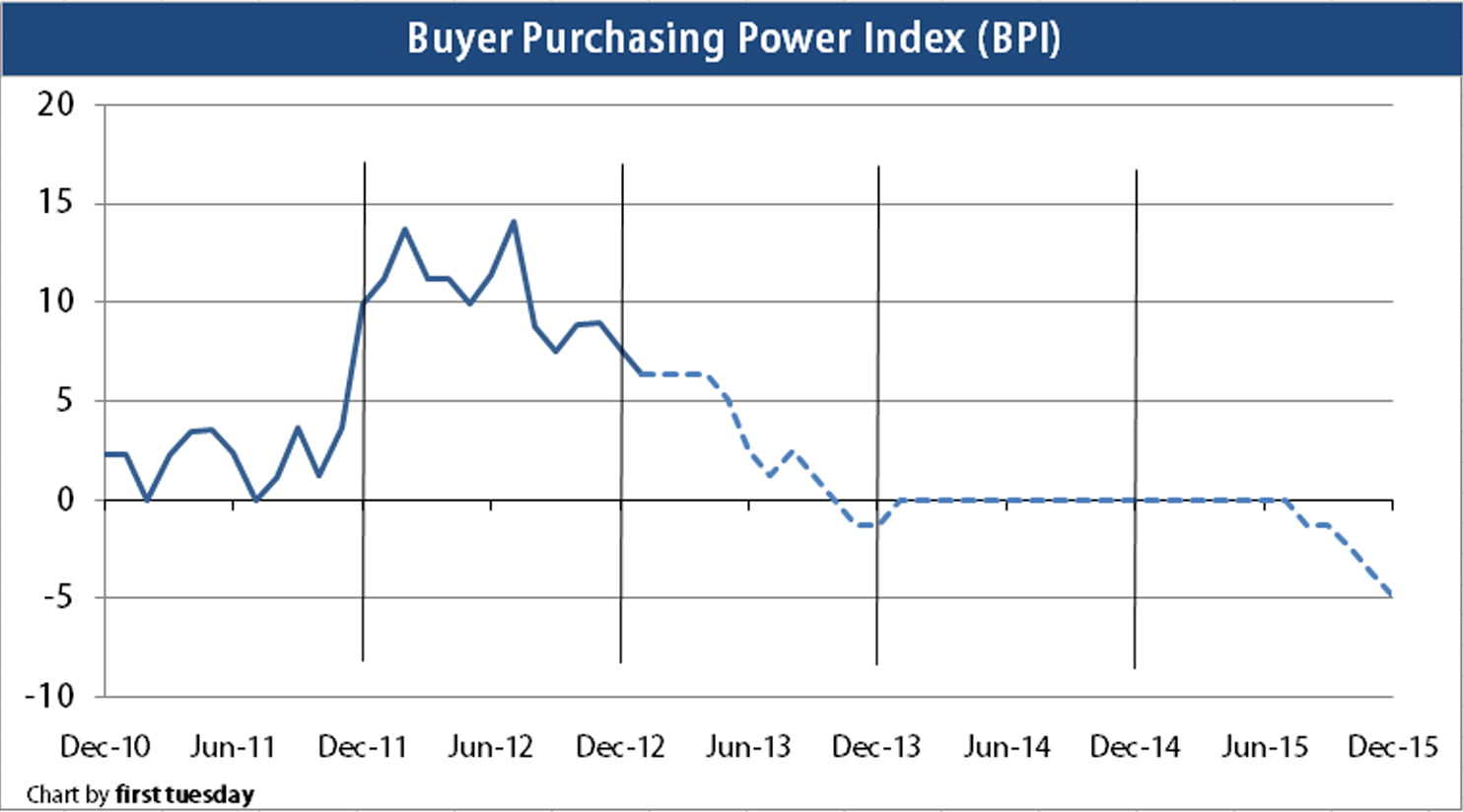

3. Interest rates to stay low — for now

Interest rates on 30-year and 15-year fixed-rate mortgages (FRMs) reached historical lows in 2012. Rates will not drop further.

Low interest rates translate to high buyer purchasing power, as buyers can purchase more square footage or amenities with the same monthly payment (less goes toward interest). The buyer purchasing power index (BPI) measures the mortgage funds available today compared to one year earlier. BPI remained high toward the end of 2012, but will decrease in 2013 to zero, as rates continue to remain at their bottom for the next two years.

The Federal Reserve (the Fed) will work to keep interest rates low through 2015. Around this time, bond market investors will sense future rising inflation, and the 10-year Treasury note will rise. Shortly thereafter, mortgage interest rates will begin their long period of increase. Both will adversely affect the pricing of all types of real estate, with interest rates controlling market results.

Encourage potential buyer clients to buy now before sellers raise prices or interest rates rise, reducing purchasing power.

4. Construction starts pick up speed

While single family residential (SFR) construction starts varied from month to month throughout 2012, the overall trend was up 25% from 2011. first tuesday forecasts an additional 11% increase for 2013, or 30,000 total SFR starts.

Apartment and condo starts increased in 2012 by 17%. This trend will pick up in 2013 with a forecasted 33% increase, or 40,000 total apartment/condo starts.

As a greater percentage of Californians rent today than any time since the 1990s, multi-family properties have become more attractive to builders than suburban tract homes. The reason: lenders are more likely to make apartment/condo loans, as they present a reduced risk of default and high rate of return. These new properties will be found mostly in high density, coastal and city center locations.

California is nowhere near the rate of starts seen during the Millennium Boom. However, expect the increase to continue for both SFR and apartment/condo starts through 2018-2020, likely slowing in 2016 in reaction to the rise in interest rates.

5. Distressed sales taper off, still very high

Notices of default (NODs), the first step in the foreclosure process, declined throughout 2012. However, the number of NODs remains elevated far above the normal level. The number of foreclosures (trustee’s deeds recorded) likewise declined while remaining well above normal.

NODs and foreclosures will continue to decline through 2013, which means even fewer real estate owned properties (REOs) on the market. This is good news for positive equity sellers, as REOs tend to drag home prices down.

At some point in the future, possibly as early as 2015, NODs (as well as personal bankruptcies) will briefly pick up. This burst occurs at the tail end of a recovery from most recessions. It is then that homeowners become simultaneously frustrated with their black hole asset and better informed about their options to shed their negative equity home.

California homeowners continue to deleverage during this recovery. This is evidenced in the still-high number of foreclosures and short sales, and the declining number of underwater homes. Before the real estate market can recover, this deleveraging must take place across a sufficient number of households. Once this occurs, homebuyer occupants will return in full force.

6. Underwater homeowners to become solvent… sooner or later

The number of California homeowners encumbered by negative equity (underwater homeowners) continued to decline in 2012, though this number remained high by anyone’s standards at just under two million homes. The decline is due to:

- underwater homeowners shedding their mortgages through short sale and foreclosure;

- minimal price appreciation; and

- principal amortization.

Underwater homeowners will continue to decline in 2013 as the factors above cumulatively decrease negative equity.

Later, the rate of decline will pick up speed once strategic default becomes a popular choice for these homeowners. This will likely occur around 2015 when interest rates begin to rise, causing price increases to slow. Underwater homeowners will become frustrated and choose to rid themselves of their homes by pursuing a short sale or walking away.

7. Home sales volume’s slow and steady rise

The number of California home sales increased 8% in 2012 to 448,000 homes sold. This is still 41% below the 2005 peak of 754,000 sales. The sales volume rise in 2012 was due:

- primarily to speculator activity in the second half of the year; and

- partially to increased end user demand.

2013 will likely see a 10% total increase in sales volume over 2012, occurring mostly in the first half of the year. This rise will occur despite a waning speculator presence in the market, and level off by the end of 2013. A sustainable increase in home sales will occur only when end users collectively gain:

- financial support (in the form of jobs);

- positive home equity allowing for a sale; and

- confidence in the economy.

Home sales volume is forecasted to return to peak levels around 2019 with the confluence of Gen Y and Baby Boomer homebuyers. By this time employment, confidence and distressed sales will have attained a full recovery.

8. Home prices to remain flat

Home prices increased in the latter half of 2012, continuing into 2013. Like home sales volume, this price movement was mainly due to speculator competition and not end user demand. Therefore, this price increase is not indicative of a sustainable recovery, but is a short-term price bump.

Prices can be forecasted by looking at home sales volume movement 12 months prior. Thus, as sales volume begins to taper off in mid-2013, expect prices to settle downward in another 12 months.

It will be decades before home pricing returns to 2006 levels. The next peak in pricing will occur around 2020, following one year after a peak in home sales volume.

Dear agents: using the forecast

Renters will remain a significant force in the housing market as the recovery continues. If you have trouble finding buyer and seller clients, consider focusing on this rental demographic. Offer your services in locating rental property. Take this recession-induced opportunity to build relationships with renters who are most likely to buy once the economy has fully recovered.

Encourage homebuyers by demonstratively presenting the positives of today’s market. In particular, low interest rates mean greater buyer purchasing power until prices rise to eliminate it. Today’s prices, while lamented by sellers as low, can be used to entice first-time homebuyers to purchase while the market is at its bottom level.

You can also invest in your future career by marketing yourself through vigorous FARMing campaigns. Instead of chasing after business one sale at a time, expand your efforts to build scope and breadth in a long-term client base.

Related article:

Even better, if you have homebuyer clients unwilling to compete with speculators, you can simultaneously FARM door-to-door searching out positive equity sellers to present with offers. Focusing FARMing activity in mid- and high-tier property areas will mean greater income per sale for the same effort.

Finally, consider acquiring your own long-term investment property, on your own or in a group. As 2013 is a year at or near the bottom of this real estate cycle, it is an excellent time to invest in income-producing property as a hedge against future inflation. Avoid purchasing income property based on low capitalization rates (cap rates) that are touted by listing agents to seem attractive today. Instead, anticipate that interest rates will rise within three short years, and only consider properties with cap rates above 8%. To calculate otherwise is to act at your peril.

Looking forward

The economic recovery has thus far plodded along on a bumpy plateau path. This direction will continue in 2013 with an upward tilt. End users who occupy the property they purchase will be the fuel for the ultimate recovery. Look to their movement for the best indication of the strength and stability of California’s recovering housing market.

{kind=link}

Its the first time I read this articles,now I look at the real estate more optimistically.Great Info’s.

I really enjoy reading your info. It is loaded with good information. Please keep it coming.

Macy

Good Analysis and Presentation!