The gateway to homeownership for most is a mortgage. Fixed rate mortgage (FRMs) are the smartest option for all but the most savvy investors. This leaves just one question: which is better, a 15-year or 30-year term?

A 15-year FRM can be a good option, because:

- it builds equity quickly; and

- the borrower pays less interest over the life of the mortgage.

Then again, a 30-year FRM is the more popular option, since it:

- qualifies the homebuyer for a larger mortgage, or a higher purchase amount; and

- can give the homebuyer a lower monthly payment even though it means more interest is paid over the life of the mortgage.

Homebuyers usually prefer the 30-year FRM over the 15-year, since it provides more buyer purchasing power and/or lower monthly payments.

However, for the rare homebuyer interested solely in building equity (rather than qualifying for the most house or best neighborhood), the mortgage term can make a difference. So does the 15-year FRM win for allowing equity to be built quickest, or is the 30-year FRM better because it allows for a bigger initial investment?

A report by Trulia finds the local housing market’s strength influences the answer to the 15-year versus 30-year dilemma.

The Trulia report claims the 15-year FRM is best in housing markets where home values are rising quickly. On the other hand, 30-year FRMs are better in more gradually rising housing markets. However, Trulia assumes the mortgage is used to purchase the same-priced house, when in fact, homebuyers usually stretch their homebuyer purchasing power to the limit, using a 30-year FRM to qualify for a larger mortgage amount than with a 15-year FRM.

[dfads params=’groups=37813&limit=1&orderby=random’]

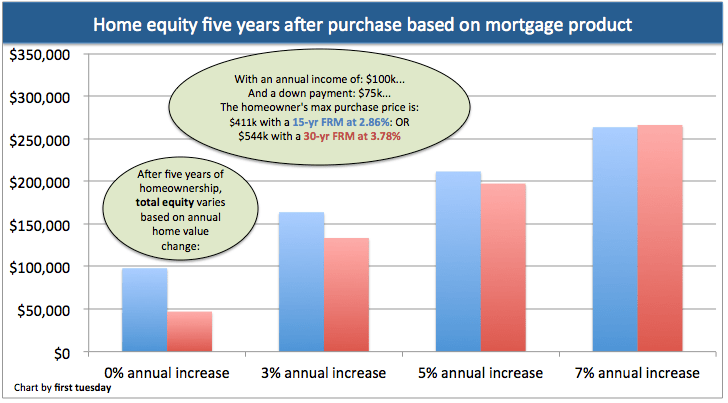

An example

In this illustration, the homebuyer has an:

- annual income of $100,000; and

- a $75,000 down payment.

The homebuyer is approved for two mortgage products:

- a 15-year FRM at 2.86%; and

- a 30-year FRM at 3.78% (the most recent average mortgage rates available at the time of publication).

For each of these mortgage products, the monthly payment includes principal, interest, taxes and insurance (PITI), and is $2,700. This will put the homebuyer’s debt-to-income ratio (DTI) at 32%.

The homebuyer plans to own the home for five years before selling. At that time, they wish to know which mortgage product will give them the largest return on investment (ROI). They know a 15-year FRM will build equity quicker, but the initial home for which they will qualify will be of lesser value than with the 30-year FRM. So which mortgage product provides the best return after five years?

It depends on how quickly the home appreciates in value, which hinges on local market variables. In this scenario, the 15-year FRM produces the most equity if the housing market is appreciating at an annual rate less than 7%. If the market is rising by 7% annually or faster, the 30-year FRM provides the best return after five years. This is complicated by the fact that homes appreciate at different rates in different neighborhoods — and the 30-year FRM qualifies the homebuyer for a home in a more expensive neighborhood than the 15-year FRM. Therefore, the higher-priced home may appreciate at a different rate than the lower-priced home.

It’s difficult to anticipate a home’s future rate of appreciation. In high-demand markets like the Bay Area, a high rate of appreciation is likely, whereas inland areas are likely to appreciate more slowly. All of these factors are complicated by larger economic factors, like interest rates, jobs and bond market movement.

A homebuyer’s best bet is to look at historic average pricing in their area. For California, the average historic annual increase, called the mean price trendline, is about 3% per year. Specific areas and home price tiers have different average appreciation rates, which can be figured on a neighborhood-by-neighborhood basis using comparable sales.

Real estate agents: what’s the motivating factor when your homebuyer clients choose a 15-year FRM over the more popular 30-year FRM? Share your experience in the comments below!

{kind=link}

This article dangerously oversimplifies the 30 vs 15 choice and omits important decision factors. Borrowers with typical shorter-term plans are often much better off with 5/1 or 7/1 ARMs; they can provide faster amortization with a lower payment. Moreover, as is the case for all 30-year loans, you can make extra principal payments without committing to higher payments that can become a problem when income declines. Higher principal balances act as a form of asset protection, deterring potential lawsuits or encouraging more favorable settlement. For borrowers with fixed-rate assumable loans, higher balances can be very beneficial. But a major consideration should be what borrowers will do with the 30/15 payment differential; if it can be invested with a better net return, it would be foolish to pay off a lower rate mortgage. The key here is that the choice of any mortgage should be made only in connection with an overall financial plan, choosing the loan program that best fits that plan.