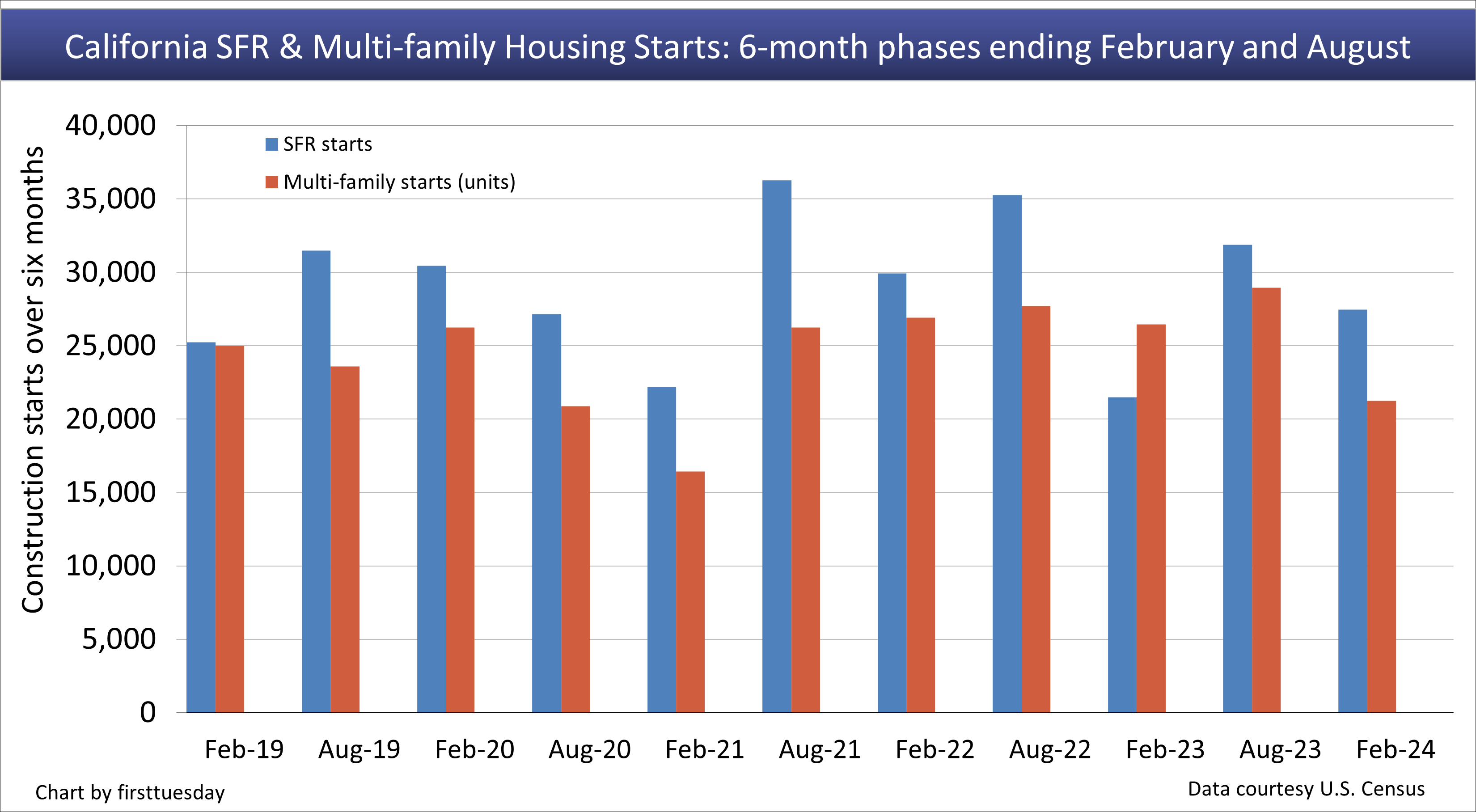

Single family residential (SFR) construction starts were 28% above one year earlier in the six-month phase ending February 2023. During those same six months, multi-family construction starts were down 20% from the six-month phase a year earlier.

In 2023, multi-family construction experienced a 4% decrease from the prior year, with 53,100 new units started. Demand for multi-family rentals has generally been higher during this past decade compared to new SFRs. But new multi-family construction continues to hit roadblocks in the form of labor and supply shortages — on top of vocal not-in-my-backyard (NIMBY) advocates.

Likewise, SFR construction starts in 2023 were down 10% from the previous year, for a total of 56,655 new SFRs started. This downward movement follows a construction bounce in 2021, the temporary surge being the result of homebuyer fear of missing out (FOMO), low home-resale inventory, and demand for remote locations where zoning does not much interfere with construction starts as occurs in coastal urban centers. And yet, compared to the 150,000 SFR starts achieved in 2005 at the height of the millennial boom, the 64,500 SFR starts achieved in 2021 were just a fraction of the starts needed to meet demand.

State-initiated legislative efforts to add to the low- and mid-tier housing stock have focused on encouraging more multi-family construction in recent years. As a result, metro areas with the highest annual increases in construction include Sacramento, Riverside and San Diego. The most anemic growth occurs where zoning remains restrictive for housing, including San Francisco, San Jose and Los Angeles.

While builders were beginning to cash in on legislative incentives and rising homebuyer demand, leaping mortgage rates and spiraling sales volume and prices in 2022 crushed builder sentiment, causing starts to plummet. Thus, residential construction starts will not reach their full potential until after the next recession, when prices bottom around 2026 and the recovery picks up steam around 2027.

Updated February, 2024. Original copy posted November 2012.

Chart 1

This chart illustrates the number of California residential construction starts during semi-annual phases ending in February and August.

Chart update 03/27/24

| Six-month period ending | Feb 2024 | Feb 2023 | Annual change |

| SFR Starts | 27,453 | 21,501 | +28% |

| Multi-family Starts | 21,236 | 26,456 | -20% |

Chart update 02/07/24

| 2023 | 2022 | 2021 | 2005 peak | |

| SFR Starts | 56,700 | 62,900 | 64,500 | 154,700 |

| Multi-family Starts | 53,000 | 55,200 | 52,800 | 50,300 |

*Forecasts are made by firsttuesday and are based on current new home sale trends, actual construction starts and current government policies.

Detached single family residential construction trends in California:

- 27,453 SFR starts took place in the six-month period ending February 2024. This is 5,952 more starts than occurred during the same period one year earlier, a 28% increase.

- 56,700 SFR starts took place in 2023. This is down 10%, or 6,300 starts, from 2022.

- For perspective, this cycle’s peak year in SFR starts was 2005 with 155,000 starts. The lowest year was 2011 with 22,000 starts.

Detached SFR forecast:

- firsttuesday‘s projection for SFR starts in 2024 is a slight decrease from the prior year. The forecast for 2024 is most affected by the downward pressure placed by higher interest rates in 2023, which slashed buyer purchasing power. Expect SFR starts to remain below their potential in the next two years, until the recovery from the next recession begins to pick up steam, likely around 2025.

- SFR starts have increased gradually each year since bottoming in 2011, but remain far below the Millennium Boom peak.

- Subdivision final reports will remain low until developers sense a return of first-time homebuyers is on the horizon.

- The next peak in SFR starts will likely occur during the boomlet period in the years following 2027.

Multi-family housing construction trends:

- 21,236 multi-family housing starts took place in the six-month period ending February 2023. This is 5,220 less starts than occurred during the same period one year earlier, a 20% decrease.

- 53,100 multi-family housing starts took place in 2023. This was a slight 4% lower than 2022, and below 2018 when multi-family starts hit their most recent peak.

- For perspective, this past cycle’s peak year in multi-family housing starts was 2004 with 61,500 starts. The lowest year was 2009 with just 9,500 multi-family housing starts.

Multi-family housing forecast:

- firsttuesday forecasts multi-family housing to be flat-to-down in 2024. As the economy is stuttering alongside rising borrowing costs, lenders continue to keep a tight fist on funds, hampering builders. This dynamic will only worsen as interest rates continue to generally rise over the coming decade, slashing buyer purchasing power. The concurrent building material and construction labor shortages are also holding back new development.

- Multi-family housing starts were expected to rise at a gradual pace beginning in 2020, as several legislative changes aimed at increasing multi-family construction encourage more building of dense, low- and mid-tier housing. However, social distancing restrictions and tightening lines of credit pushed multi-family construction numbers down significantly in 2020-2021, picking up slightly since 2022.

- The next peak for multi-family housing starts is likely to occur around 2027-2028, with the recovery of all jobs lost to the oncoming recession and crux of the next housing boom.

Statistics related to California housing:

- 14.5 million total housing units existed in California in 2021, 13.4 million of which are occupied and 7.5 million of which are owner-occupied, according to the U.S. Census Bureau. This continues a slight increase over prior years.

- Prior to 2020, California population growth had been increasing at a rate of 0.5%-1% per year. But California’s population has since begun to decline, the result of more deaths than births alongside more residents moving to other states in search of a lower cost of living.

- Roughly 18.3 million people were employed in California in October 2023. This is just over the number of jobs held prior to the 2020 recession, according to the California Employment Development Department (EDD).

- California’s rental vacancy rate was 4.3% in Q2 2023.

Related articles:

Key factors for builders

How do builders decide when and where to build? Builders analyze existing home sales, end user demand and local employment. Together, an analysis of these and ancillary factors produces a prediction of future construction trends.

Obstacles facing SFR builders

While end user homebuyer-occupant demand is the ultimate driver of construction starts, several obstacles face builders in 2021-2022 that will determine the pace of SFR and condo starts.

Builders rely on buyer-occupants to support new home construction. Discouraged by low inventory, high home prices and rising interest rates, buyer-occupant demand to purchase a home in 2018 remained stunted through 2019. However, 2020 saw interest rates plunge to record lows, which boosted buyer interest, a need unfulfilled by available resale homes since sellers remained timid in 2020. Yet, builders were largely unable to meet homebuyer demand due to social distancing measures and tightened access to credit.

In 2021, construction began to pick up as homebuyer enthusiasm exceeded the resale market and spilled over into new homes. However, building material shortages have caused delays and soaring costs, pricing out many would-be homebuyers and holding back construction increases.

Obstacles of concern to future construction starts include:

- the historic job losses of 2020, over 300,000 of which still need to be recovered in California as of April 2022;

- tightened credit for homebuilders;

- building material shortages which continue in 2024;

- rising mortgage rates, reducing homebuyer borrowing capacity; and

- restrictive zoning regulations, which discourage density in desirable living areas.

Until these factors are considered and a conclusion reached, builders (and their lenders) may not take for granted that construction starts will pay off. Expect starts to remain low until most of these factors collectively improve and starts have another 12-18 months to catch up, likely to occur around 2027.

{kind=link}

construction is a very good way to produce more work and improve better living developments.

Could you fix the first number in this statement you have? $ million is wrong.

Statistics related to California housing:

4 million total housing units existed in California in 2019, 13.2 million of which are occupied and 7.2 million of which are owner-occupied, according to the U.S. Census Bureau. This continues a slight increase over prior years.

James,

Thank you for alerting us to this typo. We have fixed the error and gone ahead and updated these statistics with the latest numbers.

Thanks for reading!

Great content, thanks for sharing.

This make no mathematical sense.

“4 million total housing units existed in California in 2019, 13.2 million of which are occupied and 7.2 million of which are owner-occupied, according to the U.S. Census Bureau. This continues a slight increase over prior years.”

13.2 mil + 7.2 mil = 20.2 million. You said there were 4 million total. If you made such a basic error in math, how could we expect accuracy in any part of the article?

Double check your math.

The writer appears to have meant “14” not “4” million. !3.2 million occupied units means that about 800,000 were vacant. Subtract the 7.2 owner occupied from 13.8 million occupied to get 6.6 million occupied by renters. These numbers are consistent.

It would be helpful to know if any of the multi-family construction increase is privately financed as opposed to gov’t subsidized (ie: “affordable” construction.

Lots of useful information, thank you. I noted the construction chart going back to the 1980’s. The chart shows a total collapse of multi-family development beginning about 1986. I wonder how much of this may have been caused by the Reagan tax changes? Prior to that there was a period where limited partnerships built or bought apartments and commercial properties. After the tax change many people decided it was better to invest in a larger personal residence rather than a small income property and the limited partnership industry disappeared. Any thought on how tax law and government policy other than zoning laws can affect change?

If you add factors of living in CA… it is extremely costly. Land banking will do good but… having such a high tax state with cost of living so high… plus capital gain on both Federal and State end… does it really make sense???

I used to be positive about CA… real estate… as an investment…

Your own home, ok, but mortgage plus high property tax plus all others…

What is your intake?

New construction will only come back when we stop some of the wayward government t programs. No more debt forgiveness and no more refinancing underwater properties (Harp). It’s time to let the marketplace get back to normal buyer and seller demand conditions so employment will return and demand will new homes will follow. Just hope we elected the right person this time around.

THE BLACK SWAN

It interests us how so many persons, when offering their predictions as to what turn future events and trends might take, virtually NEVER figure in a black swan event.

What is that? A black swan event is a dramatic, even cataclysmic event that comes on suddenly and unexpectedly and can have a drastic effect on any prognostication based solely on observable, historical, or cyclical trends.

The huge storm in the East–hurricane Sandy–is a type of black swan event. A huge earthquake would be one on the West Coast. Such things can turn the trend-lines upside down. Massive damage means massive reconstruction. Is it good or bad for the economies so affected?

MASSIVE SOLAR EVENT IN THE NEAR FUTURE?

And no one is figuring in the possible catastrophic solar event that astrophysicists are saying could very likely hit before the end of 2012 or during 2013. (for more info on that see: AthenaAcademy.net/home/current_news). Would such an event bring negative consequences or positive? Apparently Earth has gone through such monumental solar events in the past.

Builders are “Re-active” to demand. They are NOT Pro-Active and build for the DEMAND. Long term investors shoot for 5-10 years out like me. I bought thousands of Acres in 2009 to 2012 at the BOTTOM BOTTOM LOW! Builders are consumers of LAND.