New national numbers on delinquencies and foreclosure rates are out from the Mortgage Banker’s Association (MBA), and it’s good news — even we won’t dispute that. What’s this mean for California’s real estate market?

First, chew on these indisputable facts.

Delinquencies (mortgages at least one month past due but not yet in foreclosure) are at their lowest levels since Q1 2008. By Q4 2013, a scant 6.39% of all loans were at some stage of delinquency. This reflects a two-basis point decline from the previous quarter and 70 basis points from the year prior. Two basis points is not a lot (0.02 percentage points), but the figure has been steadily declining.

The percentage of loans in the foreclosure process nationwide (marked by the filing of a notice of default or judicial foreclosure proceedings) has also fallen to a new low. As of Q4 2013, 2.86% of all loans were in the foreclosure process. This is down 22 basis points from the prior quarter and 88 basis points from the same period last year.

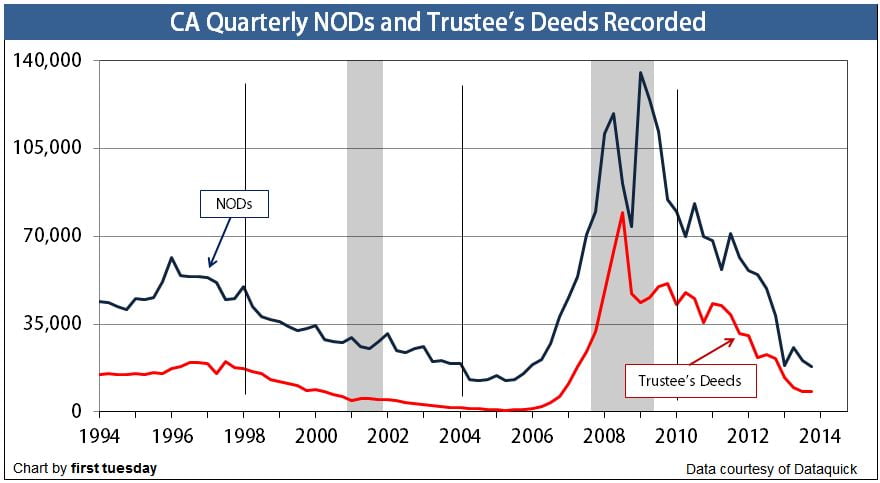

California is doing even better than the rest of the nation. California NODs (entering the foreclosure process in the non-judicial foreclosure state of California) fell by half from Q4 2012 to Q4 2013. 18,120 NODs were filed in California in Q4, which is the lowest number recorded since 2006. Trustee’s deeds (actual foreclosures) recorded also fell by about half since the previous year. Suffice it to say, the word “recovery” can be fairly applied to the issue of mortgage delinquencies and default.

Here’s our proprietary chart that shows the same:

But Dorothy wouldn’t have visited Oz and been content with just listening to the voice bellowing behind the curtain. So, let’s follow her lead and take a look at what’s behind the improved delinquency and foreclosure data.

A major factor at play here is the purported success of the government’s mortgage modification programs. As a rule, we’re highly critical of extend-and-pretend programs like Home Affordable Modification Program (HAMP) and Home Affordable Refinance Program (HARP). These programs tie homeowners to their non-performing assets and turn them away from the succor of strategic default.

Additionally, prices have been appreciating rapidly and consistently for the past year. With the price movement induced by the speculator-driven mini-bubble, the thousands of true, end-user homebuyers caught up in the speculator-induced bidding wars of 2012 and 2013 are likely going to have to contend with another price dip by the end of 2014. That’s right: just when we thought we were out of the negative equity waters, they pull us back in.

This round of negative equity will be nothing like what we saw during the Millennium Boom. Credit will be involved, but it will be on behalf of those who have been genuinely qualified to make the payments they have. They’ll be disappointed once prices readjust, certainly. But if they are in it for 7-10 years, their equity situation will prove bumpy but fair — no return on investment (ROI), but at least keeping pace as a hedge against inflation.

Those who bought in 2013, who competed in the cash bidding wars, who were foolhardy enough to go toe to toe with investors and win them out: well, they may be in for a rude awakening.

{kind=link}

While good news, the lower foreclosure numbers should be viewed with caution. Several risks remain, including:

1. Most loan mods are rising after the end of the 5-yr fixed period;

2. HELOCs are starting to enter the repayment phase, causing payment spikes due to short amortization;

3. Wages and employment are stagnant;

4. Inflation is rising;

5. The large number of low down FHA;

6. Many ARMs are coming out of interest-only, with potential payment spikes.

These risks could be compounded if rates continue to rise. So it is too soon to say we are out of the woods.