Jobs are essential to a healthy housing market. Without a consistent, well-paying job, tenants and homeowners alike are unable to make housing payments or save up for their next home purchase. But understanding how job numbers impact the housing market isn’t easy, primarily because there doesn’t exist a simple figure to quickly understand where the jobs market stands relative to where it ought to be in a healthy market — or does there?

The unemployment rate is a number cited frequently by the media to denote the health of the jobs market. But all is not as it seems.

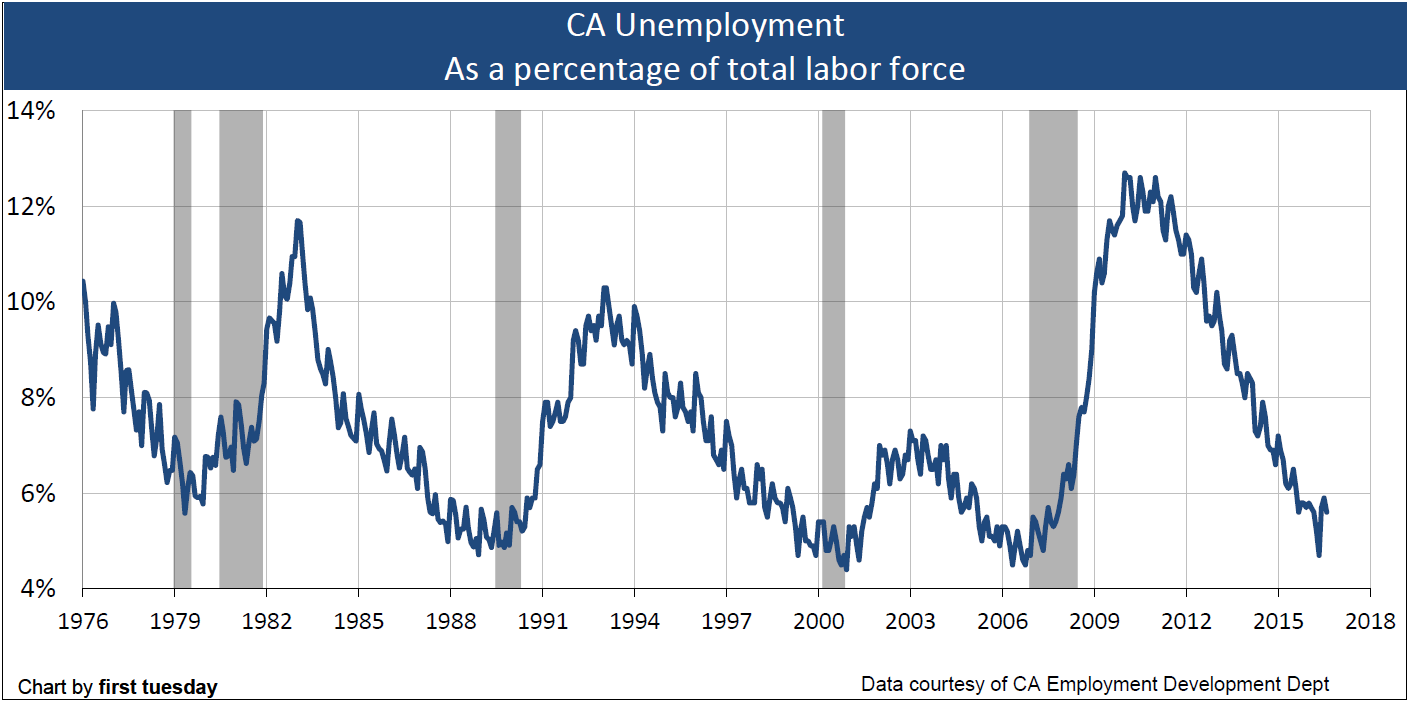

In California, the unemployment rate was 5.3% in September 2016, up slightly from the decade-low of 4.7% experienced in May 2016, according to the California Employment Development Department.

The casual observer might think this is a pretty good unemployment rate, especially when viewed alongside the high 12%+ unemployment rate of the Great Recession. But this figure is not as straightforward as it seems.

At first glance, you might expect the unemployment rate to show the percentage of people unemployed, an uncomplicated and easy-to-understand figure. But how the government gets to that number is not straightforward at all. The unemployment rate only counts those who:

- don’t have a job;

- have actively looked for work in the past four weeks (simply reading job ads doesn’t count — the individual needs to actually contact potential employers); and

- are currently available for work, according to the Bureau of Labor Statistics.

Further, an individual who does any work in the week before being surveyed won’t count in the unemployment rate. This means those who work just a couple hours a week, or someone who was laid off from a high-paying job and now working a seasonal retail job are not factored into the unemployment figure. The unemployment rate also doesn’t include those who would like to work but have given up the search.

These limitations may be partly to blame for the mismatch between today’s low unemployment rate and slow economic growth. Further, after accounting for the increased labor force, our number of jobs has yet to catch up to pre-recession numbers, when the unemployment rate was roughly the same as it is today. So how does today’s low unemployment rate make sense?

The unemployment rate is too simple to give an accurate representation of the labor market, especially in our nation’s elongated recovery from the 2008 recession.

Alternate measures of job market health

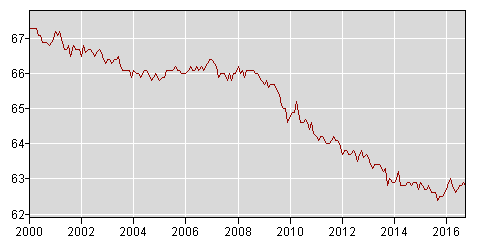

The Labor force participate (LFP) rate is another highly cited statistic, one that has shown a troubling trend in recent years.

U.S. Labor Force Participation (LFP) rate

Source: Bureau of Labor Statistics

The LFP rate measures the percentage of individuals who are employed out of the total labor force, about 19.5 million individuals in California as of September 2016. Here in California, the LFP rate most recently peaked at just above 67% in 2000, and has declined to 62.8% in September 2016.

This relatively low LFP rate indicates an unhealthy jobs market. LFP has declined across almost all age groups in California — except those Baby Boomers of retirement age, who are now delaying retirement to make up for the savings lost in the 2008 recession.

How do policymakers measure the health of the jobs market? The Federal Reserve (the Fed), which uses employment data to decide monetary policy, has their own measure.

Source: Federal Reserve Bank of St. Louis

The Fed uses data from 19 seasonally adjusted labor market indices to calculate its Labor Market Index (LMI), seen above. The Fed’s LMI takes into account the unemployment rate, the LFP rate, as well as those working part-time for economic reasons, those seasonally employed, hiring plans and other measures.

The LMI shows how labor market conditions change from month to month. For instance, October 2016’s LMI figure of 0.7 represents a small, but positive change in the labor market from the previous month. When it declines below zero, as it tends to do before and during each recession, labor market conditions are deteriorating.

The LMI has shown a long-term, gradual decline since the jobs market rebounded after the 2008 recession. Today’s dwindling LMI is part of the reason why the Fed has been slow to increase interest rates, which will cool off the economy as well as hiring. It shows a bleaker picture of the labor market than the misleading unemployment rate.

The health of the housing market goes back to unemployment

How do you determine job market performance so you can forecast the housing market?

The answer is a combination of the above. Keep an eye on the LFP rate, as well as the Fed’s less-reported LMI.

Also watch annual changes to California job numbers.

For instance, in California there were over 16.5 million people employed in September 2016, up from nearly 16.2 million a year earlier. This is a 2.2% increase, amounting to 362,500 additional jobs. For perspective, the labor force increases about 0.8% each year in California, so this 2.2% increase far exceeds what is needed to keep up with labor force growth. But — and this is significant — we still haven’t caught up with pre-recession job numbers when adding in the interim labor force growth over the past eight years.

Since 2007, when jobs were at their pre-recession peak, California’s labor force has grown by 1.5 million individuals, to the present labor force of 19.5 million. In the meantime, despite healthy annual increases over the past couple of years, we have only recovered 916,400 jobs since 2008, 585,300 short of the labor level needed to get back to where we were before the recession. At the present rate of job additions, it will be late-2018 or 2019 before California is fully recovered from the recessionary job losses.

Keep it local

Finally, remember that national and even statewide numbers can be misleading for your local market.

Job — and housing market — performance is highly localized. For example, you wouldn’t compare the Bay Area’s bustling, high-tier housing market with the slower, low-tier housing markets of the Central Valley. Likewise, you also wouldn’t compare the health of the Bay Area’s tech industry with the agriculture industry in the Central Valley.

Therefore, keep watch over job performance in your area of the state. first tuesday Local provides regional real estate news, including coverage of local employment rates by each region’s top-employing (and thus most influential) industries.

Areas where jobs are growing more rapidly will continue to see rapid growth in home sales volume and prices, too. For instance, San Francisco home values have fully recovered, and this follows a full post-population gain jobs recovery achieved back in 2014. Meanwhile, Sacramento’s lagging jobs recovery has dragged down its still-declining homeownership rate and turnover rate.

Next time you hear the nationwide or even state unemployment rate don’t be fooled into thinking our jobs market is fully recovered. Instead, find out your local job and labor force numbers to forecast the future of the housing market, and your real estate business. Visit first tuesday Local for information on our state’s most populous regions, or investigate the range of resources available on California’s Employment Development Department site.

{kind=link}