A property’s value seems to constantly change. The process of booms and busts creates pricing peaks and valleys for owners needing to sell.

During a full cycle of price fluctuations, a durable underlying pricing fundamental anchors all property values to the demographics of wages and population density. This anchor is the mean price trendline for real estate. It’s related to value which requires a use, by humans.

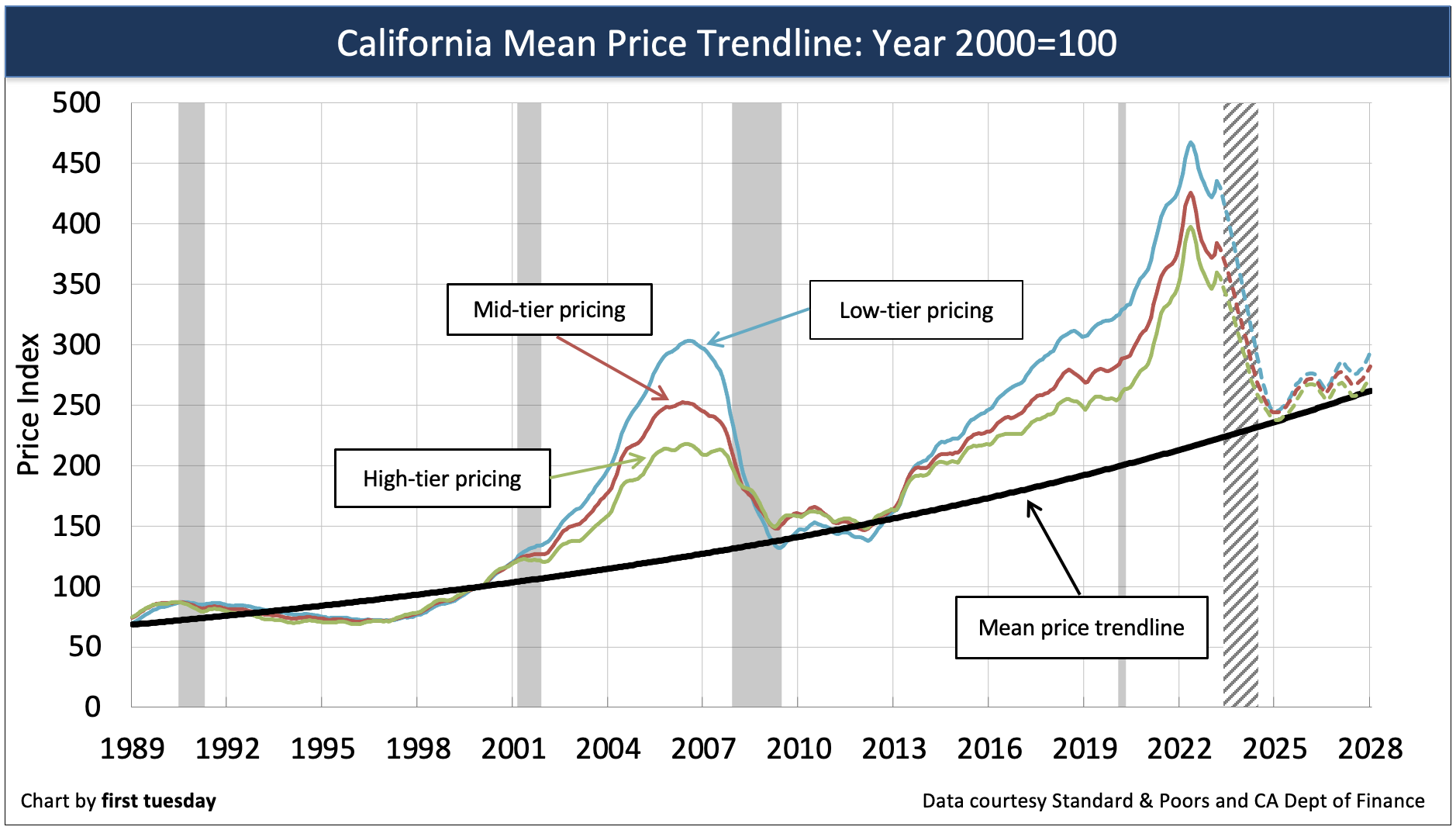

The mean price trendline is the benchmark to which prices return after a boom or a bust. A comparison of current prices with the mean price trendline tells us how far seller pricing has deviated from the historical norm, and the level prices will return to in the years ahead.

Home prices during the past decade of boom times became far removed from the mean price trendline. Several events came about which collectively caused property prices to rise in disregard of fundamentals:

- buyers’ wages accelerated in California as skilled and educated talent populated the state;

- fixed rate mortgage (FRM) rates dropped to never before experienced levels in 2012 and again in the 2020-2021 pandemic economy;

- a housing inventory starved of new housing created larger family units (and income) due primarily to zoning; and

- the higher percentage of stimulus-juiced buyers paying all cash for homes.

Prices free fall, tethered to the mean price trendline

Record-low interest rates temporarily boosted homebuyer purchasing power in both 2013 and in 2020-2021. However, when interest rates began to leap from their historic cyclical and pandemic lows, the “put” support for home prices rapidly disappeared. Without fuel from low-rate mortgage funding to support seller asking prices, California home prices peaked in May 2022. Now prices are measurably below one year ago and in a downward trend that has a likely bottom in 2025 and 2026.

For sellers, the ode is: Just how far do prices need to fall before they reach the mean price trendline?

This question is followed with: When will prices return to present levels after they hit bottom?

From their May 2022 peak, home prices will need to plunge 40% to get to the mean price trendline, likely in 2025. In other words, a $1 million home in mid-2022 will be a $600,000 home by 2026. Already mid-2023, it is priced at $900,000, and the recession has not begun.

Home prices will slump below 2019 pre-recession levels in 2024, not expected to find a bottom until 2025.

Related article:

Historic patterns

A quick review of the recent past is needed to understand today’s half cycle of a devolving price environment.

Prior to the 2008 recession, California real estate began experiencing the formation of a long-term pricing bubble. The experience took root during the stagflation years of relentlessly increasing inflation in the late 1970s. These years ended January 1983 with the highest interest rates experienced since the creation of the Federal Reserve (the Fed) in 1913 to manage excessive inflation from happening again, and again.

A 30-year bubble then began to get legs with the Baby Boomer invasion into the jobs and housing markets of the 1980s into the 1990s. The period started with mortgage rates receding from the peak 18% range in 1983 to a historically more normal 6% range by 2003.

Prices in the late 1980s reverted to the mean price trendline after the July 1990-March 1991 recession, which left the property market with excess inventory. Between 1991 and 1999, prices were depressed, and the cost of property was low, from a historical perspective. Accordingly, prices dipped below the trendline during this period, a time to acquire, not dispose. This condition is known as a buyer’s market which is yet to reemerge, but likely in 2026.

Prices began to rise in 1997, growing to intersect the mean price trendline in 2000. At that time, the price index and California Consumer Inflation index were, for a fleeting moment, at the same price point: the crossover moment.

After crossing the mean price trendline in 2000, real estate prices began a skyward trajectory. The 2001 recession was short-lived due to the very excessive monetary and fiscal reaction to the September 11, 2001 terrorist activities.

As a result, the price of homes froze in 2001 at their artificially elevated, pre-recession peak. Instead of reverting to the mean price trendline, prices leveled out. The magic on pricing produced by a recession did not take place and pricing remained without adjustment as the economy prematurely began a weak recovery.

After 2000, prices continued to rise going into a steep trajectory fueled by deregulation of mortgage lending. This period is now known as the Millennium Boom. Real estate prices peaked going into 2006, then began their sudden decline.

The unabated expansion of the pricing bubble caused its implosion in 2005 when home sales volume began a steep decline. Predictably, home prices followed one year later. One year later, the Great Recession set in at end of 2007. A classic garden variety recession was underway, but with a mortgage bond market taking a huge loss, as did property owners.

The mean price of property once again came into stark view. The ensuing drama was the worst financial experience homeowners were to endure, ending with the 2013 price recovery year.

The causes of the Great Recession’s decline in sales volume were many. Primarily, Californians experienced:

- a lack of desire to own (vs. rent) the family home, opting for mobility in our socioeconomic culture;

- price momentum speculation from 2002 through 2005;

- near total deregulation of mortgage financing permitting predatory lending to make everyone a homeowner during the Millennium Boom; and

- the Fed’s increase of short-term interest rates to fight excessive consumer price inflation beginning in August 2004.

Prices bottomed in 2009 with a “dead cat bounce” that lasted for the one-year period of the stimulus package into mid 2010. 2013 ended the period of bottom pricing.

Eventually, rates dropped to essentially zero in the pandemic years of 2020-2021. Sellers picked off the increase in buyer purchase-assist funding permitted at low rates by immediately raising asking prices. Low inventory produced an auction environment that simply hastened the FRM rate-fueled price increases.

Related article:

The mean price trendline forecast

Following the 2020-2021 pandemic economy, home prices fully reversed course after hitting their May 2022 peak. By March 2023, pricing already ranged from 7% below the peak for low-tier housing to a staggering loss of 10% in the mid and high tiers.

Watch for prices to continue to fall back in the months ahead, slumping below pre-recession levels in 2024, not expected to find a bottom until well into 2025.

Home prices at the bottom are expected to bounce along near the mean price trendline through 2026-2027.

The next big peak in prices won’t be until after 2028.

Most property buyers, whether speculators or end users, won’t return until they sense prices have fully bottomed. Even then, the buying public is generally of a pessimistic attitude toward commerce and thus hesitate to join in a recovery, until it is well underway and fully embraced by the media pundits.

As home prices continue to contract over the next two-to-three years after peaking in mid-2022, watch for the share of underwater homes to rise rapidly. Anyone who purchased with a minimal down payment during 2019-2022 will plunge deep underwater. Whether they end up in foreclosure or a short sale depends on homeowners losing their jobs or being forced to relocate for a job. The politicians will pray while others simply prey.

Related video:

Sellers in today’s market

Sellers who are going to sell within the next five years or so need to be advised to sell now, not wait. Today’s price will be the best sellers can expect until at least 2028.

As prices return to the mean price trendline over the next two years, today’s market is the ideal time for sellers to get the best price for their property.

Sellers agents are in the prime position to educate their sellers about the current market conditions and the incentives they have to sell now, not later when prices are lower.

However, sellers who plan to remain in their homes for longer than five-to-seven years will have an equal or better opportunity to sell later when prices stabilize and begin to rise, after 2028.

Keep updated on the California housing market by subscribing to the weekly firsttuesday newsletter, Quilix.

Related article:

{kind=link}