How many homes currently on the market are delinquent on mortgage payments?

- Between 10% and 20% (36%, 69 Votes)

- 10% or less (25%, 48 Votes)

- Between 20% and 30% (20%, 39 Votes)

- 30% or more (19%, 37 Votes)

Total Voters: 193

After spiking in April and May 2020, the mortgage delinquency rate — the share of homeowners not paying their mortgage — has gradually fallen back. But a closer look reveals that seriously delinquent mortgages are on the rise.

Nationwide, there were still 3.9 million homeowners in forbearance as of August 25, 2020, equal to 7.4% of all mortgages, according to Black Knight. While in a forbearance program, the lender agrees to temporarily refrain from beginning the foreclosure process while the homeowner attempts to bring the mortgage current. The 3.9 million currently in forbearance is down from the 6.0 million homeowners who have, at one point or another, entered a forbearance program due to COVID-19-related activity.

The roughly 2.1 million homeowners no longer in forbearance have either:

- become current on their mortgages (1.5 million homeowners);

- left their forbearance plan and are now delinquent and potentially headed for foreclosure (roughly 250,000); or

- paid off their mortgage by selling their home or obtaining a refinance (roughly 275,000).

Most homeowners in forbearance programs are behind on their mortgage payments, or delinquent. On the flip side, roughly three-quarters of delinquent mortgages were in an active COVID-19 forbearance program.

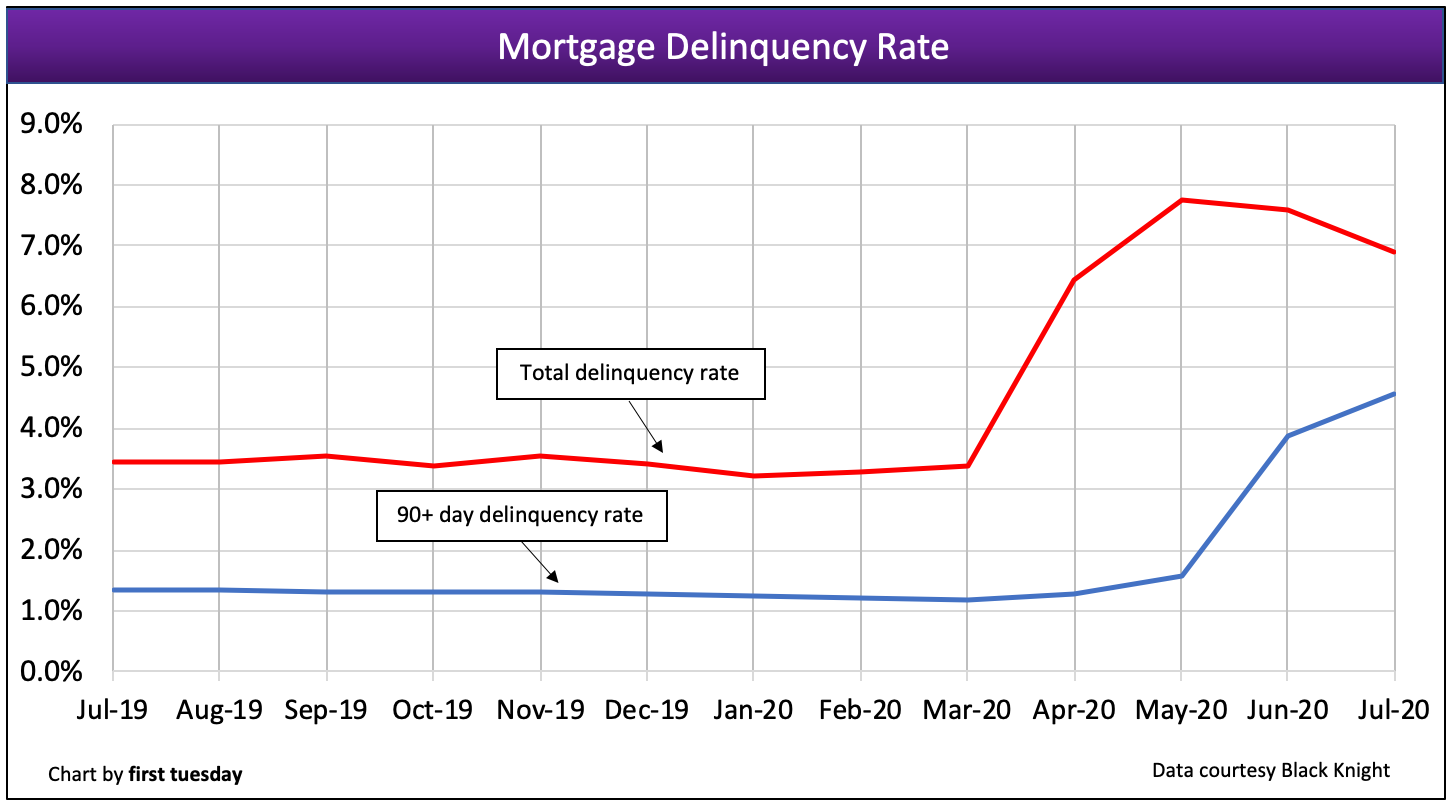

In the U.S., 6.9% of mortgaged homeowners are in some stage of delinquency as of July 2020. Here in California, the delinquency rate is a lower 5.5%. But our state still has one of the highest year-over-year increases in delinquencies, a pace of increase behind only Nevada and Alaska.

Seriously delinquent mortgages — 90 or more days past due, not counting those already in foreclosure — are, on average, 157 days past due as of July 2020. This average is typically much higher, indicative of the sudden influx of newly delinquent mortgages starting this spring.

While mortgage delinquencies continue to decline from their peak each month, the share of seriously delinquent mortgages is increasing, at 4.6% of all mortgages as of July 2020:

Worse, 2 million forbearance plans reach their expiration date in September 2020, with another 1+ million expiring in October. Since roughly three-quarters of homeowners in forbearance programs are still unable to make mortgage payments, when their forbearance programs expire the lender may begin to pursue foreclosure — once federal and state foreclosure moratoriums are up.

Related article:

Forbearance requests rise while access to mortgage credit falls

Today’s delinquencies, tomorrow’s foreclosures

The nationwide foreclosure moratorium for single family homes was recently extended through December 31, 2020.

While the current moratorium on foreclosures keeps homeowners housed during a time when the pandemic makes the loss of home dangerous for the health of all residents, it is pushing off the inevitable.

The underlying economic conditions that caused the 2020 recession will not be cured by an end to the pandemic. Historic job losses will not be restored overnight, nor will they return by the end of the moratorium period.

As job losses linger, the number of households with serious delinquencies will continue to rise. When the foreclosure moratorium ends, these delinquent mortgages will head for foreclosure in a building wave.

Think of today’s delinquent mortgages as the foreclosure shadow inventory. These serious delinquencies are not yet tangible in the market, but they reflect the future distressed sales to eventually be added to the inventory. The longer the shadow grows, the greater the tidal wave of foreclosures to come.

The impact will be a sudden influx of distressed inventory in 2021, and a dramatic cut to home prices. The housing market won’t recover until jobs begin a solid recovery, a situation — absent a government-sponsored jobs program the likes of which hasn’t been seen since the Great Depression — not likely to arrive until around 2023.

{kind=link}