This article examines residential property rent skimming recoveries available to tenants, carryback sellers and lenders who incur money losses when an investor defaults on mortgage payments during their first year of ownership.

Rent skimming during the first year of ownership

A residential property occupied by tenants may be the subject of rent skimming if delinquent mortgage payments during the absentee owner’s first year of ownership are not cured and the property goes to foreclosure sale.

Rent skimming occurs when, during their first year of ownership of a parcel of residential real estate, an investor:

- receives rents from tenants; and

- fails to apply the rents towards the mortgages encumbering the property, causing a mortgage delinquency and eventual foreclosure. [Calif. Civil Code §890(a)]

Thus, a property must go to foreclosure as a result of the failure to pay the mortgage for the action to be considered rent skimming. However, it is the date of the delinquency of at least one month’s payment on the mortgage during the first year of ownership that triggers application of the rent skimming penalties, not the date of the foreclosure sale.

For example, an investor skips a mortgage payment during the first year of ownership. In the months following, the investor makes some mortgage payments but does not cure the delinquent payment, known as a rolling late payment. After owning the property for more than 12 months, the investor stops making payments and the property goes into default, and eventually foreclosure. Here, the investor is engaged in rent skimming activities due to the initial delinquent payment occurring within the first year of ownership, triggering the eventual foreclosure sale.

If the delinquencies on mortgage payments occurring within the first year of ownership are cured, later delinquencies in payments occurring after the first year of ownership do not constitute rent-skimming activities. [CC §890(a)(1)]

Rent skimming rules apply per parcel of residential real estate, defined as one or more residential units located within the boundaries of land with a single legal description.

Investors expose themselves to civil and criminal penalties depending on the level of misconduct set out in two categories of rent skimming:

- single acts of rent skimming; and

- multiple acts of rent skimming.

Single acts of rent skimming subject the perpetrating investor to civil penalties for their conduct, not criminal prosecution.

However, an investor who engages in rent skimming on five or more parcels, all acquired during a two-year period, is also subject to criminal penalties for multiple acts of rent skimming. [CC §890(a), (b)]

The act of rent skimming

Consider an investor who locates a fully-rented residential complex they deem suitable to own. The investor and the seller negotiate terms for purchase which include:

- the assumption or origination of a first trust deed; and

- the execution of a note and trust deed in favor of the seller.

The amount of the carryback note is for the gap between the down payment amount and the amount of the first trust deed.

The property’s rental income is enough to carry its verifiable operating expenses and mortgage payments with a 10% annual vacancy factor.

The investor’s savings and liquid assets are entirely consumed by the down payment and closing costs. With this bet, the investor is left with no cash reserves to cover operating expenses if the property experiences more than the pro forma 10% vacancy at present rental rates.

Soon after acquisition, the investor experiences a substantial drop in rental income due to the loss of a tenant. Worse, the investor is unable to locate a new tenant willing to pay the rent amount the prior tenant paid.

Shortly thereafter, the investor is laid off by their employer. Starved for cash, the investor makes no further payments on the mortgages and immediately attempts to resell the units. The investor receives no offers.

After two months of delinquencies, the investor locates a tenant at a lower rental rate and enters into a one-year lease. The investor collects rents and uses the monies to cover living expenses, not mortgage payments.

The property eventually sells at a foreclosure sale on the first trust deed, exhausting the carryback seller’s trust deed lien.

At the foreclosure sale, the lender acquires ownership and the property becomes a real estate owned property (REO). The lender requests the property be vacated and gives the tenants the required 90-day Notice to Quit Due to Foreclosure. [See first tuesday Form 573]

The tenant on a one-year lease with several months remaining vacates immediately on receipt of the notice to vacate. The tenant relocates to a comparable residential unit incurring moving costs and an increase in monthly rent. The other tenants, on month-to-month rental agreements, vacate within the 90 days provided by the lender’s notice.

The tenants and the carryback seller now make demands on the investor for their money losses, claiming the investor engaged in rent skimming activities. The investor claims they did not maliciously engage in rent skimming and are not liable for the tenants’ and seller’s losses due to the concurrence of several adverse economic conditions.

Can the tenants and seller recover their losses from the investor based on the claim the investor was engaged in the act of rent skimming?

Yes! The tenants and the seller have separate, enforceable claims against the investor. Each can collect their money losses caused by the investor’s collecting rent and failing to apply the rent toward mortgage payments during the investor’s first year of ownership, called rent skimming. [CC §§890(a), 891(a), (d)]

Five or more within two years is a crime

Now consider an investor who during a two-year period acquires ownership to five or more parcels of residential property. Each is encumbered by a mortgage and occupied by tenants. Within one year of acquiring ownership to each property, the investor defaults on the mortgages secured by the properties. Rents or equivalent sums of money are not used to make mortgage payments and the properties are all lost to foreclosure sales.

Here, the investor is engaged in multiple acts of rent skimming. While the investor is liable for money losses inflicted on tenants, sellers and lenders, the investor now exposes themselves to criminal prosecution with jail or prison sentences and fines as penalties.

A tenant, lender or carryback seller who suffers money losses as a result of the investor’s rent skimming may file a civil claim against the investor alleging multiple acts of rent skimming without waiting for the state to file its criminal action. Any claimant needs to prove the investor engaged in multiple acts of rent skimming to be awarded out-of-pocket losses and punitive sums of money.

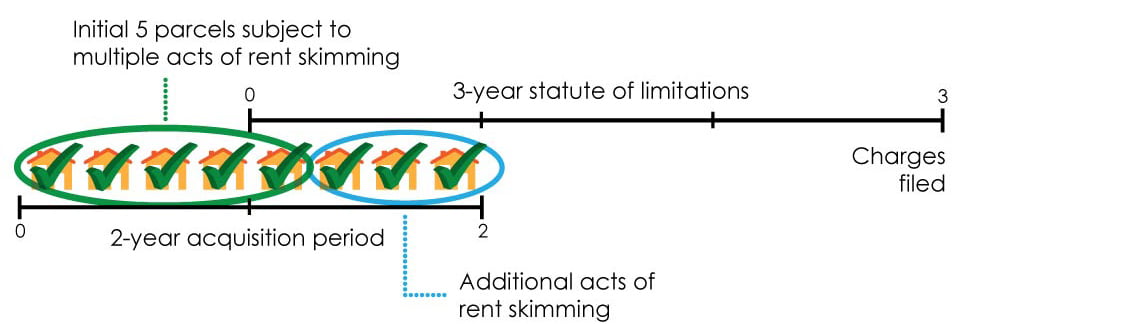

For the state to prosecute an investor for multiple acts of rent skimming, the criminal action needs to be filed within three years after the date the investor acquired the last of five parcels used for the initial claim of multiple acts of rent skimming. The parcels listed as the subject of multiple acts of rent skimming are limited to parcels acquired by the investor within a two-year period. [CC §892(c)]

Each of the acts of rent skimming which collectively make up the multiple acts of rent skimming (five or more) is separately listed in the criminal filing. Thus, the investor needs to be convicted of rent skimming on at least five parcels to be penalized for committing multiple acts of rent skimming.

Furthermore, each conviction for rent skimming on a property beyond the initial five for the conviction of multiple acts of rent skimming imposes further criminal penalties upon the investor.

For example, within a two year period, an investor acquires more than five residential rental parcels. Each parcel is encumbered by a mortgage. The investor collects the rents and defaults on mortgage payments during the first year of ownership of each parcel. The properties are all eventually foreclosed on by the mortgage lenders due to the investor’s failure to cure delinquent payments.

The state files criminal charges on:

- multiple acts of rent skimming identifying five parcels; and

- additional acts of rent skimming on the remaining parcels.

The state files the criminal action within three years after the investor’s acquisition of the last of the five parcels listed in the charge for multiple acts of rent skimming. All the listed parcels were acquired during a two-year period. However, none of the additional parcels were acquired within three years of the state filing its criminal complaint for rent skimming.

The investor claims the criminal charges cannot be brought for the additional acts of rent skimming since the additional parcels beyond the five needed for a conviction of multiple acts of rent skimming were not acquired within three years of the state filing the action. Thus, criminal prosecution for the additional acts of rent skimming was barred by the statute of limitations.

The state claims the prosecution of each additional violation is proper since:

- the rent skimming charges were filed within three years after the last acquisition of the parcels listed in the multiple acts of rent skimming; and

- the properties subject to the additional acts of rent skimming were acquired within the two-year period required for all listed parcels.

Is the investor subject to criminal penalties for the additional acts of rent skimming on parcels acquired more than three years before charges were filed?

No! The state’s demand for penalties for each additional act of rent skimming beyond the five needed for a criminal conviction is time-barred by the three-year statute of limitations. The acquisition of each additional parcel listed as subject to rent skimming did not occur within three years prior to filing the action. [People v. Bell (1996) 45 CA4th 1030]

Here, properly, all the parcels listed in the multiple acts of rent skimming accusation were acquired within a two-year period. Also properly, five of the parcels are the basis for conviction on the initial charge of multiple acts of rent skimming, subjecting the investor to criminal penalties for rent skimming.

However, some of the parcels listed as multiple acts of rent skimming were acquired outside the three-year statute of limitations (but within the two-year acquisition period). For the initial five parcels listed in the charges, only the acquisition of one parcel need occur within the three-year period to prosecute the initial multiple acts of rent skimming. [CC §892(c)]

All additionally listed parcels subject to rent skimming beyond the initial five parcels may not be prosecuted if they were acquired outside the three-year period before the criminal complaint was filed.

To be subjected to penalties for additional acts listed, along with the initial five parcels needed to prove multiple acts of rent skimming for a conviction, the additional listed parcels need to be both acquired within:

- the two-year period for all listed parcels; and

- three years of the criminal filing.

An investor guilty of an initial five acts of rent skimming under a multiple rent skimming charge is subject to criminal penalties of:

- imprisonment for one year;

- a fine of no more than $10,000; or

- both imprisonment and a fine. [CC §892(a)]

For each additional act of multiple rent skimming the investor is found guilty of beyond an initial five acts, additional penalties include:

- an additional one-year imprisonment;

- a $10,000 fine; or

- both imprisonment and the fine. [CC §892(a)]

When an investor has been previously convicted of multiple acts of rent skimming, later convictions for further rent skimming impose the same penalties as additional acts of rent skimming. Thus, for each new single act of rent skimming conviction, the investor is subject to:

- one-year imprisonment;

- a fine of no more than $10,000; or

- both imprisonment and the fine. [CC §892(b)]

The tenant’s recovery of money

A tenant of residential property subject to rent skimming may recover their actual out-of-pocket money losses from the investor in a civil action if:

- the property is sold at a foreclosure sale while the tenant is in possession; and

- the tenant is given notice or otherwise forced to vacate. [CC §890(d)]

The tenant’s recovery from the owner who rent skims includes any:

- security deposit lost;

- moving expenses;

- attorney fees; and

- court costs.

When a rent-skimming investor breaches a lease agreement held by a tenant who is forced to move before the lease term expires due to the foreclosure sale, the tenant’s initial recovery is the difference between:

- the rent due for the months remaining until expiration of the breached lease; and

- any higher rent they pay on a comparable replacement residence for the remaining term of the breached lease.

Further, the tenant holding an unexpired lease agreement at the time of the foreclosure sale may receive an additional award of punitive sums of money from the rent-skimming investor up to three times the amount of the tenant’s out-of-pocket losses if:

- payments on the underlying trust deed were at least two months delinquent at the time the tenant entered into the lease agreement; or

- the investor was engaged in multiple acts of rent skimming. [CC §891(d)]

The carryback seller’s recovery of money

A carryback seller who loses money on their note and trust deed due to rent skimming activities of an investor who became the owner of the property securing the carryback note is entitled to recover their actual out-of-pocket money losses. The seller’s recovery includes losses of amount owed on the carryback note, land sales contract or lease-option documenting the sale — despite anti-deficiency, nonrecourse law barring recovery of money.

When the property securing the carryback note is one of the properties involved in multiple acts of rent skimming, the carryback seller is entitled to a punitive award of no less than three times their out-of-pocket losses. [CC §891(a)]

The carryback seller who forecloses and recovers ownership of the property from a rent skimming investor needs to underbid at the foreclosure sale if they intend to pursue recovery of losses. The underbid is calculated by reducing the maximum credit bid permitted under the amounts due on the carryback note by the amount of the loss they anticipate on repossession of the property. If the carryback seller does not underbid, they do not sustain a recoverable loss on the foreclosure. A full credit bid and acquisition of the property are considered full satisfaction of the debt.

Recoverable losses up to the total amount of the debt owed include:

- lost value due to waste inflicted on the property by the investor;

- a casualty loss suffered by the property;

- a deficiency in the property’s value at the time of the foreclosure sale to fully satisfy the carryback note; and

- cash advances made as necessary to protect the carryback seller’s interest in the property, including payments on prior trust deed loans, property taxes and insurance premiums. [CC §891(a), (g)]

A carryback seller confronted with a default in the note may accept a deed-in-lieu of foreclosure from the rent-skimming investor. However, without a policy of title insurance on the deed-in-lieu, the investor may later discover judgment liens that attached to the title during the investor’s ownership. Here, the seller may obtain a court order to clear title.

On the seller’s request, a court will clear the title of all judgment liens against the investor which encumber the property. Exemptions from the seller’s ability to clear title of liens include mechanic’s liens and voluntary junior liens held by a lender who was unaware rent skimming activities were taking place when the (trust deed) lien was created. [See first tuesday Form 406]

A carryback seller who reacquires title under a deed-in-lieu clouded by judgment liens needs to give the judgment lienholders at least 30 days’ advance written notice of the seller’s intention to remove their liens by court order. [CC §891(b)]

However, a court will not clear tax liens, since tax liens are not judgment liens. Hence, the carryback seller needs to consider purchasing title insurance coverage before accepting a deed-in-lieu. [CC §891(b)]

Lender recovery is limited

An investor who engages in multiple acts of rent skimming is liable to the mortgage lenders for money losses incurred on mortgages secured by property involved in multiple acts of rent skimming. However, lender recovery is limited to the rents collected on the property, whether or not the investor obtained or assumed the mortgage. [CC §891(c)]

Like the carryback seller, the lender needs to underbid at the trustee’s sale (if they are going to acquire title) by the amount of rents the lender anticipates collecting from the rent-skimming investor. The recovery of rents is for losses remaining after applying the lender’s credit bid at the foreclosure sale to the mortgage debt when the lender acquires the property.

The lender cannot recover more than the money owed them on their note and trust deed which is fully satisfied by a full credit bid. Here, due to rent skimming, anti-deficiency law does not prevent the lender from recovering the rents up to the amount of the loss established by the lender’s underbid. [CC §891(g)]

In addition, a lender may receive an award for punitive sums of money, an amount solely within the discretion of the court. [CC §891(c)]

The investor’s defenses to rent skimming claims

A rent skimming investor avoids rent skimming liabilities, both criminal and civil, if:

- the rents were used to pay their medical expenses, or licensed contractors or material suppliers to correct any building violations relating to the habitability of the property;

- the expenses were paid within 30 days of receiving the rental revenue; and

- no other source of funds existed from which to pay the expenses. [CC §893]

Thus, to avoid rent skimming charges, an investor who becomes delinquent submits to the lender the entire monthly rent they receive from tenants, limited to the delinquent and current monthly payments due. Typically, the lender will imprudently return the funds to the investor, refusing to accept the rents when the amount is insufficient to fully reinstate the mortgage. To be assured the lender receives the rents, a deposit of some other nature with the lender needs to be pursued.

Investor attempts to limit liability

An investor does not shield themselves from rent skimming claims by obtaining an agreement from a tenant waiving the tenant’s rights against rent skimmers. Any waiver of rent skimming law is void as contrary to public policy. [CC §891(a)]

Similarly, an investor cannot shield themselves from rent skimming penalties by purchasing their properties through a limited liability company (LLC), partnership or corporation. The investor operating under any type of business entity or title holding arrangement will still be held liable as a rent skimmer, since they are the individual in control of the rental properties and mortgage payments. [CC §890(c)]

In distinction, a property manager is not liable for rent skimming. A property manager is an employee of the owner and is not in the position of control over the property. Their work is as an agent of the owner, the individual who controls the use of rents and payments on the mortgages. [CC §890(c)]

Likewise, rent skimming law does not hold a tenant liable who:

- sublets their unit;

- collects rental payments; and

- fails to make rental payments to the owner of the property. [CC §890(2)]

Adverse possession

An individual holding themselves out as an “adverse possessor” often acts as a landlord. In this capacity, they rent out properties and receive rents from residential tenants without the property owner’s consent. Typically, they claim they have the right to possession through a false claim of title and trespass (a requisite to becoming the owner when five years pass and all property taxes are paid). An adverse possessor who does not use the rents to make payments on mortgages encumbering the property is engaging in rent skimming. [CC §890(a)(2)]

Consider an individual who, within a 24-month period, takes possession of five or more parcels of unoccupied residential property, calling himself an adverse possessor by profession. Each parcel is encumbered by a trust deed lien.

During the first year after taking possession of each property, the adverse possessor rents the properties to tenants under their claim of ownership. The adverse possessor collects rents which are not applied toward payments due on trust deed notes encumbering the properties.

The state prosecutes the adverse possessor for engaging in multiple acts of rent skimming. The adverse possessor has no justification (such as maintaining the habitability of the property or correcting code violations) for not forwarding the rents to the lender, up to the amount of the delinquent and current month’s payments.

The adverse possessor claims they are not engaged in rent skimming since they rented the unoccupied properties as their initial step toward acquiring title.

Is the adverse possessor guilty of the crime of multiple acts of rent skimming?

Yes! The adverse possessor is criminally liable for multiple acts of rent skimming. Here, they collected rents during the first year of possession on five properties taken over within two years and did not use the rents to pay the mortgages.

However, the adverse possessor, like any property investor, is initially entitled to take the rents since they are in physical possession of the parcels. Thus, an adverse possessor does not commit the felony of grand theft since their taking of the rents is not a crime. Nevertheless, they are criminally liable for multiple acts of rent skimming for failing to apply the rents to mortgage payments. [People v. Lapcheske (1999) 73 CA4th 571]

The federal scheme

Many investors seek out desperate owners who are in default on mortgages insured by the Federal Housing Administration (FHA) or guaranteed by the U.S. Department of Veterans Affairs (VA). In these situations, the investor acquires the property with little or no money down, and then converts it to a rental unit.

For example, an investor acquires homes in default which are encumbered by FHA or VA mortgages. The investor rents the properties to tenants but applies none of the rents received to the underlying mortgages.

The investor is prosecuted for rent skimming by the federal government.

The investor claims the government cannot prosecute them unless it can show they had the intent to defraud the government.

Here, the investor need not even be aware the properties are FHA-insured or VA-guaranteed to be convicted of rent skimming when the investor who acquires a single residential property:

- rents the property;

- collects rents; and

- fails to make payments on the mortgages. [United States v. Laykin (9th Cir. 1989) 886 F2d 1534]

An investor is guilty of rent skimming under federal law if they:

- purchase one-to-four unit residential properties subject to FHA-insured or VA-guaranteed mortgages which are in default at the time of acquisition, or default on the mortgages within one year after acquisition;

- intentionally fail to make payments on the mortgages when due; and

- use the rental income for their own purposes. [12 United States Code §1709-2]

The investor may be guilty of rent skimming regardless of whether they are personally obligated on the FHA/VA mortgage.

The federal rent skimming statute does not apply to an investor who skims rent on only one property subject to an FHA/VA mortgage. The investor needs to be involved in rent skimming activities on two or more properties subject to FHA/VA mortgages to be prosecuted by the federal government. An investor guilty of rent skimming will be subject to:

- a fine no greater than $250,000;

- imprisonment for no more than five years; or

- both imprisonment and the fine. [12 USC §1709-2]

{kind=link}

Thank you for this real clear picture of rent skimming – I totally understand. however, my question is what if the lender does not accept payments due to mortgage being in default and the borrower is waiting for a loan modification which is in process; is this also considering rent skimming? if the lender is the one taking a lot of time to modifiy the home? Can you clearify this for me please. thank you for your expertise and immediate response. I recently have a client who acquired the property by court order in her divorce and she had put in personally over 100K into her owner occupied home ; however the lender is working on her modification how should I advise this client as far as keeping her rents for a room she rents, is this considered rent skimming; if it is owner occupied?