The share of homebuyers opting to use an adjustable rate mortgage (ARM) has increased in 2017, according to CoreLogic.

This increase has occurred across all segments of the housing market, from low-tier home sales to high-tier. More specifically:

- 47% of mortgages greater than $1 million were ARMs in Q1 2017, up from 43% in Q4 2016;

- 13% of mortgages between $400,000 and $1 million were ARMs in Q1 2017, up from 10% in Q4 2016; and

- 4% of mortgages less than $400,000 were ARMs in Q1 2017, up from 2% in Q4 2016.

Home prices here in California are much higher than the national average. Thus, ARM use is also higher in the Golden State than elsewhere in the country.

ARMs carry more risk than FRMs, since the interest rate on ARMs fluctuates after an initial set period of time at a comparably low rate, called the teaser rate. The teaser rate the homebuyer pays for (usually) the first five years of ownership is much lower than the interest rate after the ARM resets to match the market. This higher rate can be impossible to pay for a homeowner who, after all, qualified at the lower teaser rate. This is particularly true if the economic situation of the homebuyer hasn’t changed in the intervening five years.

Therefore, the share of ARMs in the market can be an indicator of future instability. Referring to them as ticking time bombs may be a bit hyperbolic, but it’s not too far off.

ARM use moves with interest rates

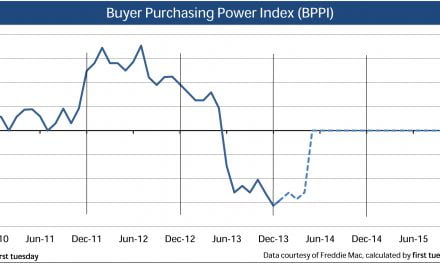

Interest rates on fixed rate mortgages (FRMs) exert sympathetic pressure on ARM use. When interest rates rise, the amount of mortgage homebuyers qualify for with the same income — a dynamic called buyer purchasing power — is reduced. Homebuyers compensate by opting for an ARM with a lower introductory interest rate to increase the amount of mortgage principal they can access and regain their purchasing power.

On the flipside, when interest rates on FRMs decrease, there is little reason for homebuyers to choose a riskier ARM over a more stable FRM with an already low interest rate.

Of course some experienced investors who plan to own the property short-term choose to take out ARMs over FRMs even when FRM rates are relatively low. But the trend for normal homebuyers remains: higher interest rates equals higher interest in ARMs.

Going into 2017, FRM interest rates jumped above 4%. This caused an equal jump in the number of homebuyers turning to ARMs. Thus, ARM use naturally rose.

However, while data is not yet available for the remainder of 2017, we can guess with a fair amount of certainty that ARM use has fallen off in 2017 as FRM rates have decreased to their current average of around 3.8% in California as of December 2017.

Related article:

However, the big caveat to this assumption is home prices.

ARM over-use signals a bubble

While ARM use fluctuates regularly with FRM rates, any distortions occurring in ARM use needs to be watched. Why? The sudden rise in the adoption of ARMs may signal an instable housing market and problems down the road.

For example, consider the leap in ARM use during the Millennium Boom. In California, about 20% of all mortgages originated in 2001 were ARMs. At the peak of the Millennium Boom in 2005, nearly 80% of all mortgage originations were ARMs. During this same time, interest rates on FRMs remained mostly flat, with the average 30-year FRM rate at about 6% during those years.

Homebuyers who used ARMs during the Boom were not reacting to higher interest rates. Rather, home prices were increasing so rapidly during this time homebuyers resorted to ARMs to keep up and not lose all the muscle behind their purchasing power.

The result: rapid home price increases were sustained far beyond the reach of incomes. As a matter of financial certainty, the inevitable housing crash began to take shape in 2006.

Real estate professionals need to keep an eye on ARM use in their local housing market, which may signal a price bubble. This is especially true in areas of the state which have seen home price increases exceeding local income growth (e.g., all of the coastal cities, including Los Angeles, San Francisco and San Diego). When ARMs start to become the new normal, recall the events of the Millennium Boom and take steps to secure your business and livelihood.

Related article:

{kind=link}