Home prices continue to rise at a breakneck pace here in California and nationally. But the increase has not been equal for all types of homes.

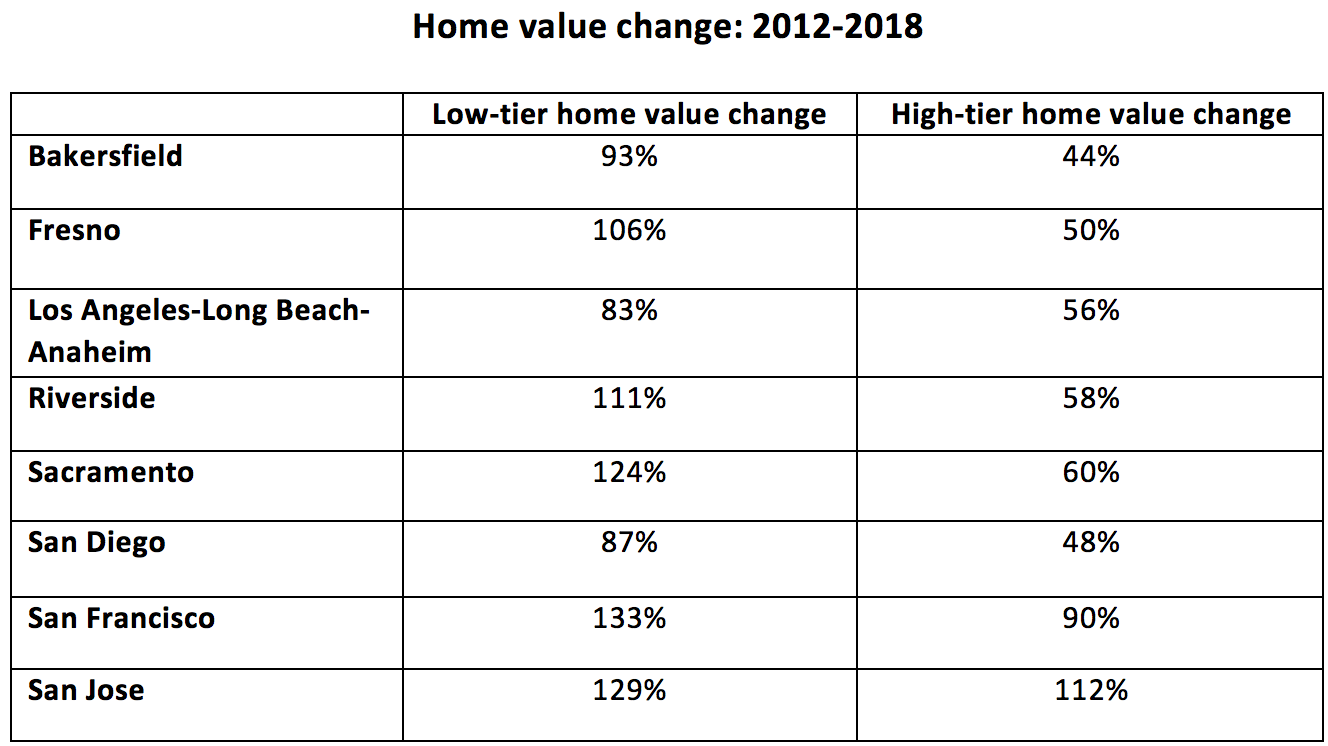

From January 2012 to January 2018, home prices rose nationally:

- 32% in the top third of home values (the high tier); and

- 48% in the bottom third of home values (the low tier), according to Zillow.

For most metros, the reason for the unbalanced price increase is due to lower inventory available for sale in the low tier. Nationally, just 22% of homes for sale were in the low tier in late 2017, compared to 51% of homes for sale in the high tier.

The lack of low-tier inventory has increased competition and caused prices to rise faster than area incomes, threatening market stability. As a result, first-time homebuyers have found it hard to keep up, and many would-be homebuyers are being pushed to the sidelines.

The problem for homeownership

Rapidly rising home values are a good thing for current homeowners, as they stand to make more profit when they sell. It’s also nice for homeowners — and their local economy — to have the freedom to move due to the fast home equity growth occurring across California.

But for renters who wish to become homeowners, it’s another story.

California renters face a number of obstacles to homeownership. Before even considering home prices, renters need to save up for a down payment. But saving is almost impossible after spending 50% or more of their income on rent.

What’s more, renter income was stunted for years during the economic recession and elongated recovery. The real jobs recovery has yet to occur in California, as the number of jobs haven’t even caught up to pre-recession numbers when counting the interim population growth.

Then, there are rising home prices, which present an ever-moving target for homebuyers attempting to save. And when they finally muster the savings needed for a minimum down payment, they find themselves in competition with multiple offers due to the inventory shortage in their price range.

Related article:

All of this has contributed to California’s below-average homeownership rate. The homeownership rate in 2017 was 54% in California, continuing a years’ long trend of flat-to-down homeownership. For reference, the national average homeownership rate is 64%.

Fewer homeowners ultimately means fewer home sales and, by extension, fewer real estate professionals. In order for the real estate industry to grow in a healthy and sustainable way, the inventory of homes needs to rise much faster in 2018. This will be accomplished by more low-tier construction, an effort currently underway across the state.

Related article:

California worst in the nation for new affordable construction

{kind=link}

Thank you Carrie for your clear detail on low-tier homes. For low-tier developers your report is a bit of good news, while simultaneously being bad news for renters wanting to buy. It remains interesting, however, that not everyone assumes renters have knee-jerk thirst to go out and buy. But for buyers wanting to shelter in the low-tier range, this may be a good time for them to buy.