This article discusses how the ratio of adjustable rate mortgages (ARMs) to all loans originated can be used to determine the health and direction of the real estate market in the near future.

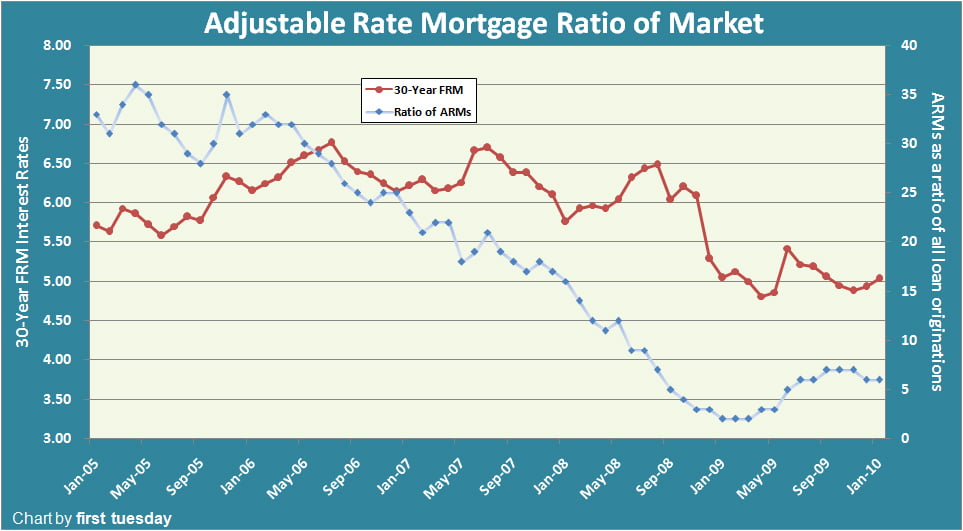

Chart last updated 3/2/10

Data courtesy of Freddie Mac

As of January 2010, adjustable rate mortgages (ARMs) made up about only 6% of the mortgage market nationally compared to the 36% at the height of the Millennium Boom. This 6% is low, yet it is higher than the 2% it was in January 2009. This slight upward trend is a harbinger of a certain set of events which, if they continue to unfold, will again prove disastrous as they did a scant four years ago.

As the gatekeepers to real estate, brokers and their agents need to know that the shift among homebuyers from fixed rate mortgage (FRM) to ARM financing means that the real estate market is destabilizing. This information can help them to provide better service to their sellers and homebuyers.

The story of ARMs, and a homebuyer

Consider a prospective homebuyer in the current market who hires a broker and one of his agents to locate a suitable property to purchase and occupy. On the advice of the agent, the prospective homebuyer meets with two or three lenders to obtain pre-approval letters. The letters will be submitted with a purchase offer on the house he may wish to purchase.

The prospective homebuyer first meets with a loan officer at a community bank or credit union and obtains a pre-approval letter for a FRM loan of a specific amount.After searching for weeks, the prospective homebuyer locates a house he wants to purchase. During his house hunt, real estate prices have risen in the area most attractive to the prospective homebuyer. Also, his agent tells him that several offers are being submitted for the better-priced homes since an auction environment is developing, pitting buyer against buyer.

To remain competitive, the prospective homebuyer plans on submitting an offer above the listing price. This requires him to return to the lender to obtain pre-approval for a higher loan amount.However, the loan officer informs him that, due to the recent rate hikes in the bond market purchasing mortgages, the community bank has increased interest rates available to mortgage borrowers. The lender will only approve the prospective homebuyer for a loan amount based on current rates for 30-year FRM loans with a payment equal to 31% of his gross monthly income, the traditionally acceptable debt-to-income ratio (DTI).

As his gross income has not changed, but the interest rates charged by the lender have gone up, 31% of the homebuyer’s gross income (the fulcrum between interest rates and corresponding maximum loan amounts) no longer qualifies the homebuyer to “buy” as large a mortgage as it had previously. Thus, the prospective homebuyer is no longer able to purchase the house at the price he thought he could.

The prospective homebuyer is anxious to purchase a house as soon as possible, as he has heard numerous reports by the media and his agent that housing prices will continue to rise in the future. The agent is aware the starting ARM interest rates — teaser rates — are currently lower than the FRM interest rates. The prospective homebuyer is advised by his agent to receive pre-approval for an ARM instead of an FRM if he wants to borrow a greater sum to buy the house. The prospective homebuyer is approved for a higher loan amount with an ARM loan, as the initial teaser rate (the rate at which the borrower is approved) is significantly lower than the interest rate for an FRM loan.

The prospective homebuyer submits his purchase offer to the seller for a price above the listing price — after all, he wants to be able to beat out other buyers when prices are rising — which is accepted. He purchases the home with funding from an ARM at a price above the property’s true value based on long-term real estate fundamentals. What the homebuyer does not comprehend is that the monthly payments on his ARM will later adjust upwards to an amount far above 31% of his gross monthly income, the maximum amount of income that should go to a mortgage payment if the homebuyer is to maintain his current and future standard of living.

Sound familiar?

It should, for any real estate agents practicing real estate at the time of the Millennium Boom in the mid-2000s. However, most agents looking back do so with aversion, rarely thinking of the valuable predictive power in the ARMs-to-FRMs ratio which reflects the overall health of the real estate mortgage market.

Rising ARMs ratio betrays market weakness

The predictive power of the ratio of ARMs comes from its movement as a share of all mortgage loans originated. The chart above tracks the monthly interest rates charged on 30-year FRMs from 2005 to present. The 30-year FRM rates are provided to show the relative stability of the FRM rates over recent years — until the onset of the financial crisis in late 2008 and the Federal Reserve’s (the Fed’s) massive mortgage-backed bond market intervention as the lender of last resort when open market funding collapses, as it did in 2008. The ARMs as a ratio of total mortgage loan originations are represented in blue. The shaded portion of the chart shows the official dates of the Great Recession. [For more information on the Fed’s role as the lender of last resort, see the December 2009 first tuesday article, The lender of last resort: understanding the function and methods of the Federal Reserve.]

The steady decrease in the ratio of ARMs to all loans originated beginning in mid-2006 and running through late 2008 reflects public awareness of the nasty effects of ARMs after adjustments to rates and payments set in, brought about by the Fed raising short-term rates to slow down the over-heated U.S. economy.

The trough in ARM popularity came when the ARM loan rates were equal to or slightly higher than FRM loan rates: the Fed was stepping up short-term rates, which in turn discouraged homebuyers from using the short-term ARMs to purchase property. At the same time, bond market investors were also beginning to reduce the long-term rates (which directly influence the FRM rates) in response to the reduced danger of inflation present in the consumer products and cooling real estate market. This reduction gradually shifted homebuyer interest away from ARMs and back to FRMs (until the financial crisis hit in late 2008, at which time the entire mortgage bond market shut down). [For more information about bond market investor’s role in predicting recessions with the yield spread, see the March 2010 first tuesday article, Using the yield spread to forecast recessions.]

However, the average collective memory of the public is very short. Notice that as the FRM rates increased slightly during the last year, the ratio of ARMs in the market showed a corresponding increase, since higher FRM rates are again slowly making ARM rates more alluring to short-sighted and over-anxious prospective homebuyers who pay too much to get into homes. This is probably a one-time shock brought about by the home purchase tax subsidies which will disappear in 2010.

ARMs and the dysfunctional real estate market

The weaknesses of the real estate market revealed by the recent Millennium Boom (and the associated Great Recession) are tied inextricably to the prevalence of ARM originations during that period. Financing the purchase of residential real estate with ARMs points to several key instabilities in a momentum environment of increasing sales volume:

- Homebuyers are over-anxious. Over-anxious homebuyers who cannot afford to finance the purchase of homes with stable long-term FRM loans are making the myopic decision to resort to ARMs and greatly over-extend their future finances to get into homes now, as no adverse short-term consequences are apparent. They are not being told, nor do they themselves properly take into account the true cost of ARM loans when short-term rates increase — as they invariably do in normal business cycles of recession and recovery. This overheating of the market — its weakness — creates a breeding ground for speculators.

- Speculators have a large presence in the market. ARMS provide a free lunch for flippers: rates are cheap in the short term, providing speculators with enough time to get in, wait for prices to go up — the rush delivered by a momentum-based market — and then sell, hoping all the time to take a profit.

- Home prices are unnaturally inflated. As more speculators enter the market to suck out their share of rising equities, they bid up property without regard to the fundamentals of real estate valuation, and over-inflation of housing prices ensues.

All of these conditions point to that most financially pernicious condition, the asset bubble. Thus, whenever ARM loans — slyly referred to as zero-ability-to-pay (ZAP) loans — rise in popularity, it should raise a massive red flag in the very face of industry professionals that the Fed will need to soon slam on the brakes of the speeding real estate market before the bubble implodes. The Fed accomplishes this primarily by raising short-term rates and reserve requirements for private banks to discourage lending in the overheating real estate market.

Knowledge brokers can use

The old joke in lending is that when a borrower opts for an ARM loan, lenders not only get an ARM off the borrower, but eventually his (proverbial) leg, as well. The industry has long been aware of what borrowers cannot seem to take to heart: ARMs are great only for the lenders who gladly take the fees, and speculators who don’t care about long-term ownership or market stability.

Agents need to take care to counsel their buyers not to succumb to the toxic ARM. Brokers and agents who keep a close eye on the future ratio of ARMs to all loans originated will have the knowledge as fiduciaries to provide their clients — buyers and sellers — with up-to-date information and their opinions about the potential direction of the market.

As ARMs become more popular during this recovery, potential buyers become more confident and momentum builds a chorus of “Buy, buy, buy!” Faced with these conditions, prospective homebuyers will find it increasingly difficult to compete, but will want to do so. These buyers must be told that there is no wisdom in mortgaging their future financial solvency for what will amount to a short-term tenancy when they can no longer make mortgage payments after they’ve paid too high a price in the frenzy. If buyers are informed, the speculators go away, the homebuyers buy and sellers get a fair price for their properties.

{kind=link}