What will home price movement look like in 2015?

- Home prices won't significantly change in 2015. (61%, 123 Votes)

- Home prices will rise significantly throughout 2015. (32%, 64 Votes)

- Home prices will fall significantly throughout 2015. (7%, 15 Votes)

Total Voters: 202

Back to the drawing board

Anticipating home prices is not unlike forecasting the weather. If you take all relevant factors into consideration and time it right, you will usually succeed with relative accuracy. And we hate to admit it, but this weather pattern got the best of us at first tuesday in 2014.

We – and other economically minded individuals – forecasted a drop in prices in the second half of 2014, continuing through 2015 into early 2016. Our primary reasoning was simply that home prices had jumped too high, too fast, far outpacing growth in homebuyer incomes or jobs.

Taken with the swift exit of speculators in 2013-2014, disappointing home sales volume performance, mortgage banker withdrawals from the market and a year of no retreat on mortgage rates, we were fairly certain home prices would fall.

But mortgage rates had a surprise in store. The average 30-year fixed rate mortgage (FRM) rate began to fall in October 2014, a couple months after home prices began to stall across California. In the span of four months, mortgage rates dropped from about 4.2% to just above 3.5%.

To translate, this drop in mortgage rates increased buyer purchasing power by many thousands of dollars. For an average income-earner in California, buyer purchasing power rose by $20,000 due to the rate drop. In turn, homebuyers were suddenly able to qualify for mortgages to fund home prices that until that point were out of reach – even with the use of a risky adjustable rate mortgage (ARM) for greater funding.

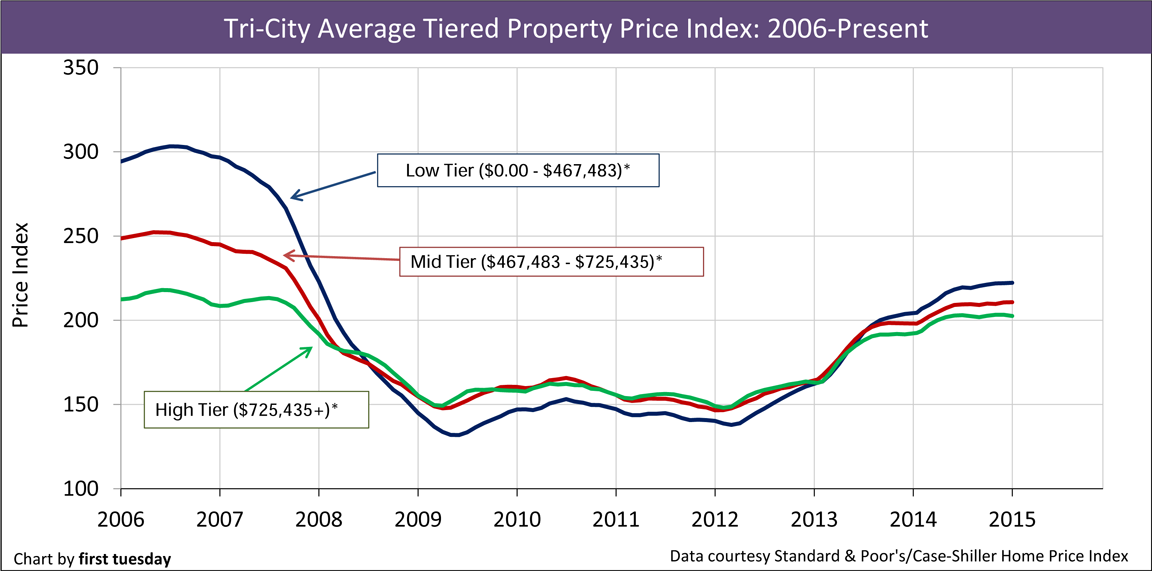

Since rates began to fall in October, home prices have reached a compromise. They are no longer accelerating as they did in 2012-2013. Rather, they have flat-lined. Here is a picture of what home price movement looks like, as averaged between the three major metropolitan areas in California: Los Angeles, San Diego and San Francisco. (To see charts for each of these regions, view our full pricing article).

The latest price report covering January 2015 shows low-tier home prices are still on average 9% higher than they were in January 2014. Likewise, mid-tier prices are 6% higher and high-tier prices are 5% higher. However, average prices have barely budged across all tiers since October 2014. Thus, this year-over-year rise will continue to narrow as we make our way through 2015.

A new forecast

So what is the new pricing forecast?

Considering all relevant factors, we can safely say that home prices will remain roughly the same through the first half of 2015. In the second half of this year (likely Q3 2015), you will see home prices rise gradually and not very significantly. The increase won’t last for long, and will probably reverse direction by the end of 2016.

Here are the reasons:

- Mortgage rates. The Federal Reserve (the Fed) has indicated it will most likely start raising the short-term rate in late 2015 or even early 2016. When the short-term rate rises, bond market investors tie bond rates to the short-term rate if inflation is the issue (which it isn’t, it’s actually excess savings). Keeping the difference between the two rates level is key to investors maintaining profits. Thus, when the Fed signals it’s almost ready to raise the short-term rate, you can bet that mortgage rates will rise in anticipation (as they did in mid-2013 in what is now called the “taper tantrum” when the Fed announced its intent to end the creation of more dollars).

With rising mortgage rates come decreased buyer purchasing power (as in 2013) and less support for home prices, hence the decrease in pricing within 12 months of the mortgage rate bump. Thus, prices will probably fall by the end of 2016.

We also acknowledge the unexpected massive inflow of excessive savings to the U.S. held by foreigners unable to find investment opportunities in this global recession. This move to the dollar contributed to the drop in bond rates (and an unhelpful strengthening of the dollar chilling manufacturers and jobs). In a reverse flow, the economies of the world beyond the U.S. will at some point start to pick up speed. When that happens, those foreign savings parked in the safe harbor of the U.S. dollar will leave and drive mortgage rates up, stalling homes sale volume and prices.

- Home sales volume. The number of homes sold fell 7% in 2014. So far in 2015, sales volume has shown to be roughly the same as last year. Lackluster sales volume will temper the rise in prices expected by the end of 2015. Prices will lack the momentum that would otherwise be present with a healthy home sales volume in California. Lacking the support of home sales volume, pricing will be limited to rise only gradually by the end of 2015.

- Jobs. Here is some very good news. In mid-2014, California finally regained the number of jobs lost during the 2008 recession. Now, we continue to add jobs at a robust pace. The latest jobs report shows a yearly increase of 3.2% or 489,300 new jobs. Good news in the jobs market means more confident homebuyers.

However, wages have yet to experience the same recovery pace as job growth and gross domestic product (GDP) wealth production, the income inequality issue. In this wage environment, increases in buyer purchasing power are most reliant on mortgage rates remaining the same or dropping as in the past, rather than changes in income which have not kept up with inflation for over a decade.

- Construction starts. Don’t expect to see much competition from new homes in the next couple of years. Single family residential (SFR) construction has faltered over the past 12 months, essentially the same as a year earlier and still well below pre-recession levels. On the other hand, multi-family construction (mostly built for rental purposes) is rebounding with a little more steam, at 44,300 starts in 2014 with lots of room to grow – until the influx of new tenants decide it is time to own a home and rental vacancies jump as happened in the late 1980s.

A lack of new housing construction is actually good news if you’re hoping for prices to rise. That’s because when adult population growth exceeds new construction, there is more demand for essentially the same number of units. This high demand, low supply situation naturally keeps prices afloat. Today, the housing demand tide is being wasted in California by the failure of most urban areas to see economic stability in providing proper zoning so high density condo construction can start.

Still not convinced? Let us know how you expect pricing to go in 2015, and why, in the comments.

{kind=link}