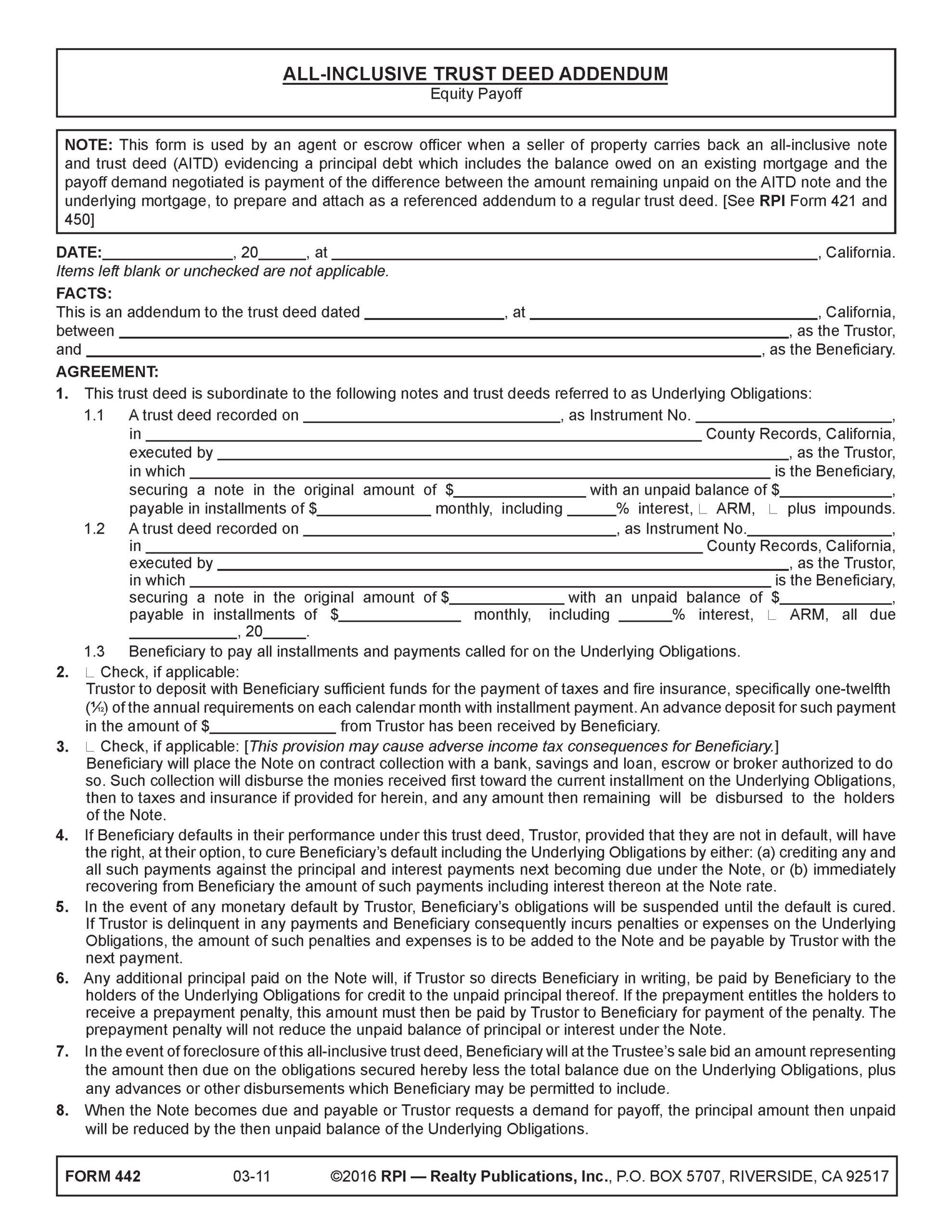

This form is used by an agent or escrow officer when a seller of property carries back an all-inclusive note and trust deed (AITD) evidencing a principal debt which includes the balance owed on an existing mortgage and the payoff demand negotiated is payment of the difference between the amount remaining unpaid on the AITD note and the underlying mortgage, to prepare and attach as a referenced addendum to a regular trust deed.

Flexible financing

The all-inclusive trust deed (AITD) and note is a debt instrument and security device for the carryback sale of mortgaged real estate. It provides agents, sellers and buyers with the flexibility needed to finance the balance of a sales price remaining to be paid after a down payment is made. [See RPI Form 421]

For a buyer with a down payment, the AITD carried back by a seller is all the financing needed to acquire the mortgaged real estate sought.

The principal balance amount of the AITD includes:

- the unpaid balance on the existing mortgage which will remain of record, called the wrapped mortgage or underlying mortgage; and

- the seller’s equity in the property remaining to be paid after the buyer’s down payment.

With an AITD, the buyer makes monthly payments to the seller as negotiated in the all-inclusive note. Likewise, the seller continues to make monthly payments to the mortgage holder on the underlying mortgage.

The seller, buyer and underlying mortgage holder all mutually benefit from the carryback arrangement.

To benefit the seller, the AITD:

- allows a greater yield than is ordinarily negotiated for the note rate on a regular second mortgage, a financial advantage generated by the overriding interest rate feature available by use of an all-inclusive note;

- eliminates the risk of loss due to a default on the underlying mortgage since the seller remains responsible for its payment;

- defers profit tax liability for a greater percentage of the transaction’s profit since an all-inclusive note increases the percentage of profit allocated to the principal in the carryback mortgage;

- supports the price sought by the seller by providing non-institutional financing; and

- provides for a trustee’s foreclosure on the buyer’s default, unlike other wraparound security devices, such as land sales contracts and lease-option agreements which require a judicial oreclosure (unless they contain a power-of-sale provision).

To benefit the buyer, the AITD provides more simplicity and flexibility than conventional or government insured mortgages, since:

- the interest rate and payment schedules are fully negotiable and not tied to rigid secondary money market standards;

- the carryback seller is less concerned with creditworthiness and income ratios than standardized institutional lenders due to the seller’s knowledge of the property and a more personal relationship with the buyer;

- the buyer makes payments on only one debt obligation, the all-inclusive note; and

- no third-party lender fees are required, such as points, garbage fees, private mortgage insurance (PMI), assumption fees or a separate lender’s American Land Title Association (ALTA) title insurance policy.

AITD final payoff amounts for two variations

An AITD is always a junior mortgage, usually a second. Thus, an AITD is subordinate to one or more pre-existing, underlying mortgages. For lender enforcement and ownership rights, the AITD has the same function as a regular trust deed.

An AITD form is created by using a regular trust deed form with the addition of an AITD addendum. The AITD addendum provisions covers the structure and accounting for the financial aspects unique to an AITD. [See RPI Form 450, 442 and 443]

Two types of AITDs exist based on payoff at reconveyance:

- an equity payoff AITD [See RPI Form 442]; and

- a full payoff [See RPI Form 443]

With an equity payoff AITD, reconveyance occurs when the amount of the seller’s equity in the AITD — the principal amount of the AITD remaining after deducting the underlying mortgage balance — is paid, called satisfaction.

Once the seller receives the payoff for their net equity amount in their AITD and reconveys it, the buyer is left with the primary responsibility for future payments on the originally wrapped mortgage. With the equity payoff AITD, the underlying mortgage is not paid off and remains of record with the reconveyed AITD no longer encumbering the property. In this situation, the buyer originally took title subject to the underlying mortgage.

With a full payoff AITD, reconveyance occurs only when the buyer pays the entire balance remaining unpaid on the AITD note. In turn, the seller as holder of the full payoff AITD, pays off the amounts owed on the underlying mortgage concurrently with the buyer’s satisfaction of the AITD debt. Thus, both the AITD and the underlying mortgage are fully satisfied and reconveyed on the payoff of the AITD. For the buyer, the full payoff AITD is less financially flexible, leaving no alternative for payoff of the mortgages.

Tax-wise, the full payoff AITD is preferable for the seller. The full payoff AITD, without a contract collection provision, provides for no debt relief at any time during the life of the AITD. The buyer may never take over primary responsibility for the underlying mortgage, even on final payoff and reconveyance of the AITD. Thus, the full payoff AITD allows the seller to use the installment sales method of income tax reporting without the issue of debt relief ever arising.

Analyzing the equity payoff AITD addendum

An agent or escrow officer uses the All-Inclusive Trust Deed Addendum — Equity Payoff published by RPI when a seller of property carries back an AITD note to evidence the debt owed, calculated as the portion of the price remaining after deducting the down payment. This debt includes the amount remaining on an existing “wrapped” mortgage.

The seller’s payoff demand for reconveyance of the equity payoff AITD will be the sum of the amount of the debt remaining unpaid on the AITD note minus the principal amount remaining on the existing mortgage which will remain of record. The AITD addendum form is attached to a regular trust deed form. [See RPI Form 442]

The equity payoff addendum for an AITD contains:

- existing financing information which identifies the existing encumbrances on the property, the principal amounts of each included in the all-inclusive note amount [See RPI Form 442§1];

- impounds for the agent to check when impounds will be paid to the seller by the buyer for property taxes and casualty insurance. When a wrapped mortgage is impounded, the AITD is also impounded [See RPI Form 442 §2];

- contract collection for the agent to check when the seller has agreed with the buyer to place the mortgage on contract collection with a third party [See RPI Form 442 §3];

- seller’s default/buyer’s remedies which state when the seller defaults on the underlying wrapped encumbrances, the buyer may cure the default and make payments directly on the delinquent underlying encumbrance [See RPI Form 442 §4];

- buyer’s default/seller remedies which state when the buyer fails to make payments on the AITD, the seller is no longer required to make payments on the underlying wrapped encumbrances unless the AITD is reinstated [See RPI Form 442 §5];

- a prepayment penalty pass-through provision which states a payoff of an underlying encumbrance caused by the buyer or made at the request of the buyer incurring a prepayment penalty places responsibility for payment of the penalty on the buyer [See RPI Form 442 §6];

- a foreclosure bid provision which states the seller’s demand on foreclosure of the AITD will be the amount of their equity in the AITD. The AITD equity is the difference between the balance remaining on an all-inclusive note and the balance(s) remaining on the underlying encumbrances. The buyer at the foreclosure sale takes the trustee’s deed subject to the underlying encumbrances [See RPI Form 442 §7]; and

- a payoff demand provision which states the payoff demand for reconveyance of the AITD. The payoff demand is the difference in the amounts remaining unpaid on the all-inclusive note and the underlying wrapped encumbrances. [See RPI Form 442 §8]

Form navigation page updated 12-2023. Updated 01-2026.

Form last revised 2016.

Form-of-the-Week: Deed of Trust & Assignment of Rents, and All-Inclusive Trust Deed Addendums — Forms 450, 442 and 443

Form-of-the-Week: All-Inclusive Trust Deed (AITD), AITD Addendum with Equity Payoff and AITD with Full Payoff —Forms 421, 442 and 443

Article: A trust deed investment for groups

Article: Rising rates bring back seller financing

Page: The Due-On Clause Strikes Back

Video: The Note and Trust Deed Work Together

Video: Who Conducts the Sale?

Video: Repayment Variations: Graduated Payment Mortgage and All-Inclusive Trust Deed