This form is used by a mortgage holder when the owner of a mortgaged property defaults and faces loss of the property by foreclosure, to transfer ownership of the property to the lender in exchange for the lender cancelling the trust deed note.

Conventional foreclosure

Foreclosure is a procedure to recover the amounts owed on a mortgage debt in default through an orderly sale of property pledged as security for the debt. The foreclosure process is triggered by a default in payment or a breach of trust deed terms relating to the property.

A mortgage holder or carryback seller holding a note secured by a trust deed in default has two foreclosure methods available, the only methods to enforce collection of the secured debt. These two foreclosure methods are:

- a judicial foreclosure sale, also called a sheriff’s sale [Calif. Code of Civil Procedure §726]; or

- a nonjudicial foreclosure sale, also called a trustee’s sale. [Calif. Civil Code §2924]

The key to the mortgage holder’s ability to nonjudicially foreclosure by a trustee’s sale on the mortgaged real estate is the power-of-sale provision contained in the mortgage trust deed document.

By foreclosing under the trust deed’s power-of-sale provision, the mortgage holder avoids a costly (and potentially time consuming) court action for judicial foreclosure.

Alternatives to foreclosure

A homeowner in default on their mortgage has alternatives to foreclosure.

Alternatives to foreclosure that may be more favorable for a homeowner include negotiating a:

- mortgage forbearance;

- loan modification;

- conventional sale;

- short sale; and

- deed-in-lieu of foreclosure.

A mortgage forbearance occurs when a mortgage holder agrees to temporarily forego proceeding with their collection efforts, such as canceling a trustee’s foreclosure. During the forbearance period, the property owner takes steps to bring the mortgage payments current.

A loan modification occurs when the mortgage holder agrees to change the terms of the note documenting the mortgage debt. The note itself is not cancelled or newly rewritten since the debt it documents is secured by a trust deed which references the note.

A conventional sale of the property is the most common alternative to foreclosure as the mortgage is paid off using the owner’s sales proceeds.

However, when the property’s value is less than the mortgage amount, the owner’s sale of the property is called a short sale or non-conventional sale.

Short sales become common during recessions. During the Great Recession of 2008-2009, roughly 25% of California multiple listing service (MLS) sales transactions were short sales.

Following the Great Recession, California home prices peaked in 2022. Since then, prices bounced on a flat plateau of pricing which held until 2026 when prices started to decline.

Prices will continue to retract in the years ahead. This means anyone who purchased with a minimal down payment in 2019-2022 will slip underwater. For owners needing to sell property with a value less than the mortgage debt, they will either find a buyer and negotiate a short sale or default and force the lender to acquire it as real estate owned (REO) at a trustee’s sale.

Deed-in-lieu of foreclosure

An option involving the turnover of the property is a deed-in-lieu of foreclosure, commonly called a “friendly foreclosure.” Here, the property owner voluntarily hands the mortgage holder a grant deed conveying title to them, an exchange of property for debt relief. This saves the mortgage holder time and money since they avoid the costs and lost time of a foreclosure sale. Further, mortgage holders sometimes will offer relocation assistance to speed up the process.

When a homeowner cannot avoid foreclosure by negotiating a forbearance or loan modification, or a short sale of the property, the homeowner may be able to arrange a deed-in-lieu of foreclosure with the mortgage holder.

The deed-in-lieu is usually a last resort arranged when:

- the mortgage balance encumbering the property is greater than the property’s value;

- the mortgage is a nonrecourse debt; and

- the owner fails to sell the property through a short sale.

A homeowner who executes a deed-in-lieu acceptable to the mortgage holder essentially conveys their property to the mortgage holder in exchange for canceling the debt.

Both the deed-in-lieu and a reconveyance of the trust deed are recorded, extinguishing the lender-borrower relationship between the mortgage holder and the homeowner.

Analyzing the deed-in-lieu of foreclosure

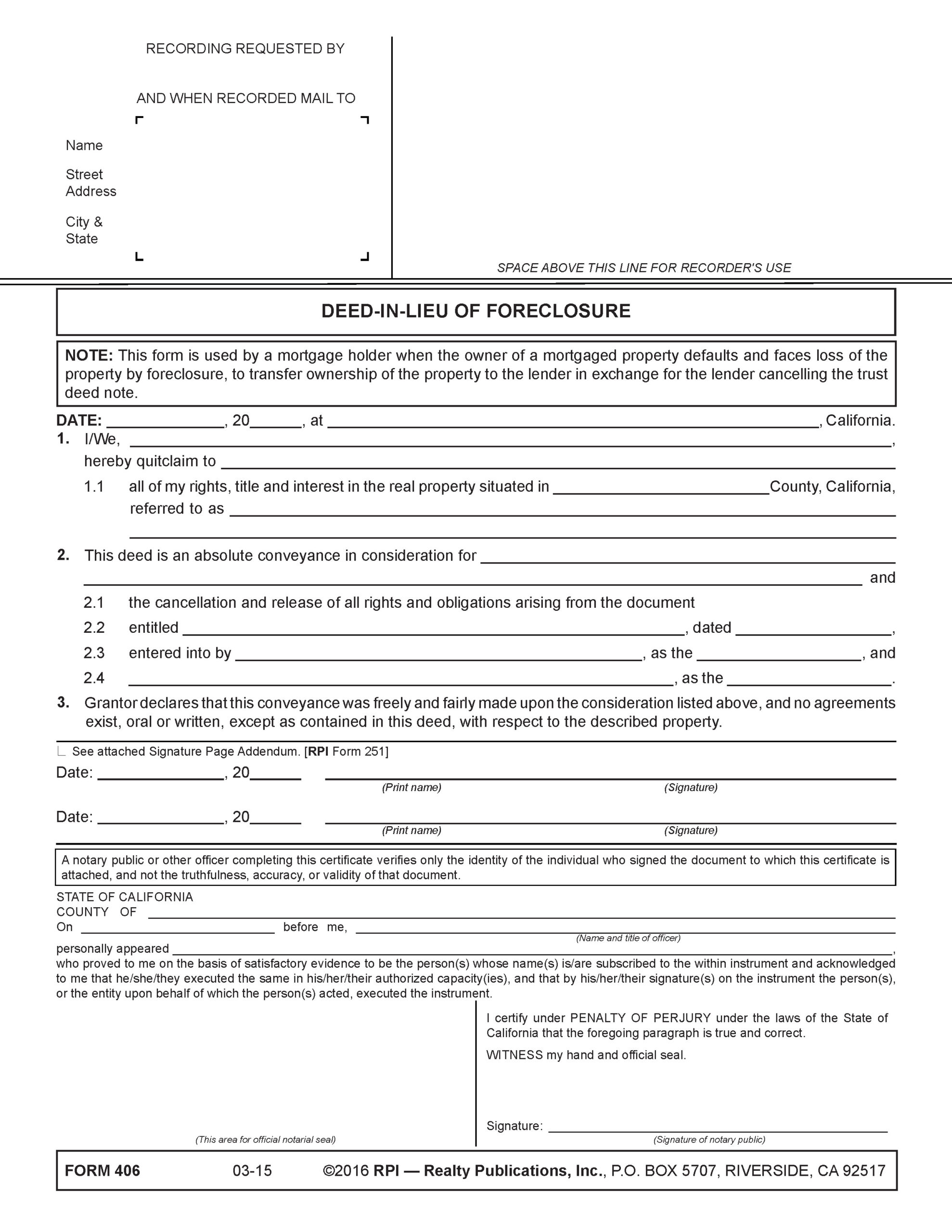

A mortgage holder uses the Deed-in-Lieu of Foreclosure form published by RPI when the owner of a mortgaged property defaults and faces loss of the property by foreclosure. The form allows the homeowner to transfer ownership of the property to the mortgage holder in exchange for the mortgage holder cancelling the trust deed note. [See RPI Form 406]

The Deed-in-Lieu of Foreclosure contains:

- the date [See RPI Form 406];

- owner and mortgage holder’s identities [See RPI Form 406 §1];

- the county and address of the mortgaged real estate [See RPI Form 406 §1.1];

- the requirements the mortgage holder demands in exchange for the conveyance of the real estate [See RPI Form 406 §2];

- the deed is exchanged for cancellation and release of all rights and obligations arising from the mortgage [See RPI Form 406 §2.1];

- the note and trust deed securing and identifying the debt and date it was entered into [See RPI Form 406 §2.2];

- the borrower’s name and identity (trustor or grantor) [See RPI Form 406 §2.3];

- the name of the bank or mortgage servicer as beneficiary on the trust deed [See RPI Form 406 §2.4]; and

- signatures of the property owner(s). [See RPI Form 406]

The form is then notarized to verify the identity of the homeowner conveying the property. [See RPI Form 406]

Form navigation page published 04-2026.

Form updated 2016.

Form-of-the-Week: Purchase Agreement with Short Sale Contingency, and Deed-in-Lieu of Foreclosure — Forms 150-5 and 406

Article: Mortgage delinquencies lead to foreclosures

Article: MLO recession survival guide Part 2: Buyers’ agents and underwater home sellers

Chart: Negative equity and foreclosure

Client Q&A: What are a homeowner’s foreclosure alternatives?

Client Q&A: What is a deed-in-lieu of foreclosure?

Video: The Power-of-Sale Provision