Is anybody in the real estate industry worried about our dangerously low inflation rate? They ought to be.

The liquidity trap revisited

Do you recall the “liquidity trap” everyone was talking about from 2010-2013? With all the excitement of Janet Yellen’s coronation and the buzz about the great real estate comeback, it seems the term has lost its cachet. Perhaps if one is caught in a trap long enough, it starts to feel like home.

Consider this a bucket of ice water splashed over your dazed facade — the trap is real and the U.S. (actually most of the developed world) is still stuck in it. A “liquidity trap” occurs when banks hoard huge cash reserves (i.e. liquidity) rather than putting it into circulation and spurring growth. This hoarding effectively eviscerates the central bank’s attempt at stimulus. Thus, we are trapped on an island surrounded by a sea of cash that we cannot spend.

Further complicating matters is the “zero lower bound.” Interest rates are at zero and the Federal Reserve (Fed) cannot lower them any further to spur growth and break free from the trap. Yes, the 30-year fixed rate mortgage (FRM) rate increased a full percentage point from its low of 3.5% in 2012-2013. But this was due to an increase in the 10-year T-note, the 30-year FRM’s benchmark, resulting from falling unemployment and modest growth in gross domestic product (GDP). The short-term Fed Funds rate remains at zero, meaning lenders still pay nothing for their cash.

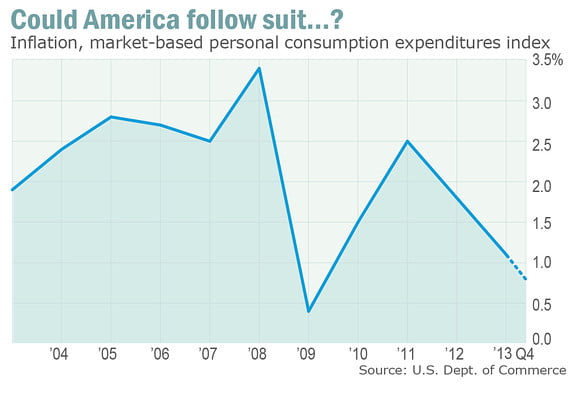

Do you like sushi?

Inflation is dangerously low — which is the natural result of the liquidity trap. Inflation occurs only when cash is in circulation. We call it, too much money chasing too few goods. In order for that to happen, there’s got to be a chase. Right now the global economy looks more like Waiting for Godot than it does Smokey and the Bandit.

Check out this side-by-side comparison of Japan’s deflationary history with our own disinflationary present, courtesy of the Wall Street Journal.

So this is the predicament we’ve been in since the 2008 financial crisis. Widespread amnesia set in, especially among real estate agents who believed the recent speculative mini-bubble was a sustainable home price increase. This will prove to be a red herring in the recovery debate. California real estate prices were inflated due to speculative housing bets by cash investors: both large institutional investors and mom-and-pops looking for a good return on stagnant savings.

This tripartite economic condition of low:

- interest rates;

- inflation; and

- employment

has led many to liken our current malaise to Japan’s so-called lost decade. In a piece we published at the beginning of the year, we noted famed economist Larry Summers’ term, secular (long-term) stagnation, a concept pulled directly from the dire economic diagnoses of Japan.

The Fed’s choice

The Fed announced its inflation target of 2% per annum in 2012 as a result of the alarming disinflation caused by the liquidity trap.

Since that time, inflation has rarely reached the 2% mark. In fact, the Consumer Price Index (CPI) changed at a rate of 1.5% for the year 2013. The Fed projects inflation to come in at a flaccid 1.2% for 2014.

This is getting ridiculous.

The Japanese now explicitly recognize that creating higher inflation is necessary for stimulating growth. Sadly, they’ve only come to this realization after a decade of economy-crippling deflation.

Many economists are now urging the U.S. not to follow suit and better manage inflation before it’s too late. As one editor at The Economist points out, the rate of inflation in the U.S. is a choice. Some analysts are using the case of the zero lower bound and seemingly ineffectual bond-buying program as an example of the impotence of our monetary policy (a decidedly libertarian perspective).

But the fact is, the Fed has a choice, and they’ve chosen to scale back stimulus at a time when inflation remains well below target. Thus, the Fed has decided they are more concerned by inflation running out of control than they are with deflation further eroding employment and GDP. (And we thought Janet Yellen would be a dove!)

Job creation is tied to inflation

The number one fundamental in any economic analysis of the real estate market is this: jobs move real estate. Understanding and embracing this truth will set you free…from believing the California real estate market has recovered. The market activity we’ve witnessed over the past few years has not been thanks to a jobs recovery (with the rare of exception of the booming BayArea, perhaps). Thus, it is not sustainable.

The most recent unemployment rate published by the Bureau of Labor Statistics was 6.7%. But as is widely understood, this is not the “real” unemployment rate. It is what is known in inner-economic circles as U-3. U-3 defines an “unemployed individual” as someone who actively sought work within the previous four weeks.

U-6, on the other hand, includes:

- discouraged workers (those who have given up the job search);

- marginally attached workers (those who still think its possible to get work, but have stopped looking); and

- part-time workers who need and want full time work.

The U-6 unemployment rate was 12.7% as of March 2014. Does that figure inspire the kind of confidence necessary to taper off the monetary stimulus? We think not.

Above all, this dangerously high unemployment figure proves that inflation has been allowed to ride too low for too long.

A formula for recovery

The Fed has a dual mandate:

- ensure price stability; and

- achieve maximum employment.

In order to attain the latter, the Fed has several tools at its disposal. It can no longer stimulate hiring by lowering interest rates — interest rates are already at zero. Thus, its next and most viable option is to allow prices to increase (inflation), which will allow employers to keep nominal wages the same while actually paying workers less (once adjusted for inflation).

But this kind of policy is a tightrope walk. No one wants to see wages fall any further, but this very tactic of allowing wages to “fall” via rising inflation has proven an effective stimulus for employment in the past. Labor market confidence is generally unaffected by this phenomenon since workers primarily pay attention to their nominal wages. Inflation would have to rise very high for an extended period of time for the blow to be felt in the average worker’s pocketbook.

The benefit to employers, however, is significant and almost immediate, since their revenues increase along with the general price level. This allows for more hiring, private business expansion and thus economic growth.

Herein lies the formula for a real real estate recovery. What’s happening instead is a continuation of the long, slow ride to the tune of secular stagnation. The persistence of this liquidity trap gives a whole new meaning to the term “underwater”.

{kind=link}

Right on! It make a lot of sense. What the plan to come out of this cycle?