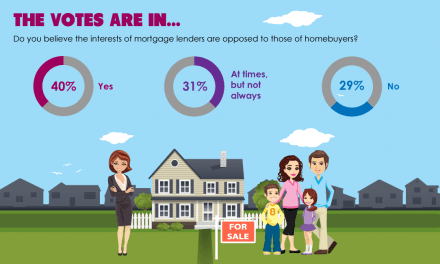

Ability-to-repay rules put in place following the 2008 recession — the disastrous result of years of de-regulated mortgage lending — require residential mortgage lenders to make a “reasonable and good faith effort to verify that the applicant is able to repay the loan.” [12 Code of Federal Regulations §§1026.43 et seq.]

To simplify matters for lenders, the Consumer Financial Protection Bureau (CFPB), along with other federal agencies, introduced the qualified mortgage (QM), a category of loans that automatically meet the rules.

To meet the definitions, lenders need to verify applicant criteria such as income, employment, debt-to-income ratios (DTIs) and assets. Likewise, the mortgage offered needs to meet criteria like limits on the mortgage term, points and fees and payment ratios.

The benefit for originating a mortgage that meets these criteria is, for the lender, greater protection or safe harbor if the homebuyer defaults and, for the homebuyer, a more competitive interest rate and terms.

However, one notable requirement is missing — there is no minimum down payment requirement included in the QM or QRM rule.

Before the QM was adopted as the gold standard, two categories of acceptable mortgages were floated, the QM and the qualified residential mortgage (QRM).

Originally, it was expected that the QRM rules would have stricter rules, including the need for a higher down payment. But when the rules were finalized in 2014, the agencies in charge chose to align the QRM rules with the QM. The potential down payment rule did not make it into the final QRM ruling.

Excluding a down payment requirement was a big miss for overall housing market stability. The federal agencies in charge reasoned a 20% down payment requirement would limit mortgage access for low- and moderate-income homebuyers. But at the same time, any down payment below 20% requires the added expense of private mortgage insurance (PMI), inflating overall borrowing costs for low- and moderate-income homebuyers unable to muster a 20% down payment.

The agencies’ approach — championed by trade associations like the California Association of Realtors (CAR) — was to qualify as many mortgages as QRMs, rather than actually making any changes in the mortgage market. In their words, their aim was “reducing regulatory burden.” Thus, more mortgages will be originated under the current QRM and QM, but this comes at a steep price: lower principal amounts due to PMI and a higher risk of increased defaults due to a lack of skin in the game from low-down-payment homebuyers.

Of course, the agencies were correct: imposing a down payment requirement was sure to have decreased mortgage originations at the start. But it would have meant a more stable housing market over the long-term cycles of boom and bust. Short-term discomfort for long-term stability.

A better, alternative approach would have been for the agencies to have imposed a graduated down payment requirement. first tuesday’s suggestion is to introduce this graduated down payment plan, to increase over several years, giving time for homebuyers to plan and adjust. This might start with a minimum 5% down payment, to increase gradually over the next 7-10 years, at which time the minimum down payment to qualifying homebuyers for the QRM will be set at 20%.

A graduated minimum down payment plan helps avoid the pitfall of lost homebuyers and steep drop-off of sales volume that an immediate 20% down payment requirement would cause. But, unlike the current rules, it would ensure long-term housing market stability, even during future recessions.

{kind=link}

A 20% down payment is over $100k (using the median of $573k) for Californians. I think that a 20% mandatory down payment will actually prevent home ownership for our youngest populations. The time it will take non home owners to amass $100k would be a huge barrier to entry. Equity is not the only reason a person will/will not continue to make payments. When people are in financial straits, sometimes it’s their pride that is their detriment. They are too embarrassed to share their story with the right people in order to put together a plan. Having laws that make home owners with less than 20% equity attend mandatory financially informative classes every few years until they amass 20% equity would be very helpful. They would become educated about what to do during a personal financial crisis. Education has always been the reason American’s are able to rise up. If we are going to push anything on them, let it be more education.

In California, the cost of housing is such that 20% minimum down payments would put home ownership out of reach for many potential Good buyers. There are too few homes for far too many people. The housing supply is to low. Perhaps if the various industries worked

to insure more housing the ability to pay would NOT be such an issue. And, I am witnessing what I describe as extremely biased and perhaps illegal underwriting where ALL are not subject to the same underwriting rules. Variable rules for the “right” demographic is illegal but appears to persist.

It’s not a good idea to comment on things you know absolutely nothing about. It’s obvious that you know nothing about the mortgage industry , and underwriting in particular. I’ve been in the mortgage industry for 25 years and I’ve NEVER seen any “demographic” differences in underwriting. It might happen once in a while, but it is certainly a rare occurrence. There are a couple hundred variations of mortgage loans out there, and each has their own set of underwriting guidelines. Is there a group of people that I choose not to work with? Absolutely, they’re called azwholes. BUT if YOU know of real discrimination on the groups that the government has listed as protected classes, then get your proof and get hold of the appropriated Federal agency. they love nothing more than to get on news that they collected a big fine from some miscreant lender. Do you know how I figured out you are ignorant about this stuff? There is no such thing as “illegal underwriting”. Educate yourself and STOP being a bombthrower like all the crazy liberals on TV these days.

The crazy people are the ones who bring politics into something that has nothing to do with politics