This article is a first in a series covering AB 3088: the Tenant, Homeowner and Small Landlord Relief and Stabilization Act of 2020.

California Governor Gavin Newsom and legislative lawmakers signed a new law to halt evictions for thousands of tenants who are unable to pay rent as a result of the coronavirus (COVID-19) pandemic through January 31, 2021.

Newsom previously issued an executive order in March 2020 placing a moratorium on evictions through the end of May. The order was extended two separate times, with California’s Judicial Council voting in August to end it on September 1, 2020.

Protections for Tenants

AB 3088, also known as the Tenant, Homeowner, & Small Landlord Relief and Stabilization Act of 2020, is helping to provide temporary relief to thousands of Californians. A recent UCLA and USC study found that between 58% and 68% of tenant households in the Los Angeles area lost income since mid-March. Without the new law, renters would have been left more vulnerable since income losses are widespread throughout the state.

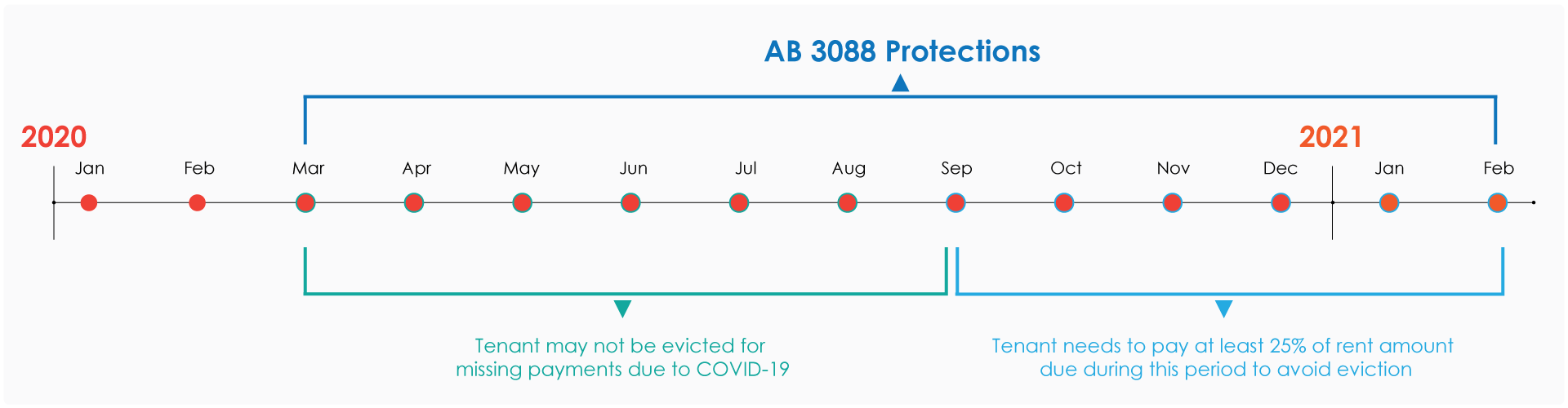

The bill protects renters from being evicted if they failed to make rental payments due to COVID-19-related financial distress between March 1, 2020 and January 31, 2021.

Under the new law, a tenant may not be evicted before February 1, 2021 as a result of unpaid rent related to the pandemic between March 4, 2020 and August 31, 2020. Tenants who are unable to pay rent due to COVID-19 between September 1, 2020 and January 31, 2021 must pay at least 25% of the rental payments due in that time period to avoid eviction.

For example, consider a tenant who losses their job in August due to the pandemic and is unable to pay the full amount due for rent. The tenant continues to pay 25% of their rent to their landlord each month. The tenant may not be evicted since they are paying the correct amount due, under the new law. A tenant may pay 25% each month or pay one lump sum by February 1, 2021 to avoid eviction.

Tenants are still responsible for paying all unpaid amounts to landlords.

To be eligible for the new protections, tenants need to provide a declaration of COVID-19-related financial distress to their landlord. COVID-19-related financial distress refers to:

- loss of income caused by the pandemic;

- increased out-of-pocket expenses directly related to performing essential work;

- increased expenses directly related to the health impact of the pandemic;

- child or elder care responsibilities, disabled or sick family member directly related to the pandemic that limits the ability to earn income; or

- other circumstances related to the pandemic which have reduced income or increased expenses.

Before a landlord may evict a tenant under this law, they are required to give tenants a 15-day notice that informs them of the amounts owed and include a blank declaration form to use to comply with this requirement.

Editor’s Note – RPI is currently drafting new landlord-tenant notice forms to comply with these new requirements. The new and updated forms will be posted to the Forms Download page once they are completed.

It is important for tenants to not ignore a 15-day notice to pay rent or quit or a notice to perform covenants or quit from their landlord. If a tenant is served with a 15-day notice and does not submit the declaration form before the notice expires, they may be evicted.

Tenants who make more than 130% of the area income where they live may also be required to provide additional documentation of financial hardship to their landlord.

Protections for landlords

Tenants who failed to pay rent during the specified period will have their rent balance turned into consumer debt, which can be pursued in small claims court starting March 1, 2021.

Landlords who do not follow the court evictions process will face increased penalties.

Evictions not related to unpaid rent – such as nuisance complaints or health and safety violations – may still take place.

Additionally, landlords who own fewer than four units and do not live in them will receive some foreclosure protections under the Homeowners Bill of Rights, which was passed in the wake of the late 2000’s foreclosure crisis. The rights refer to specific guidelines mortgage servicers need to obey when communicating with borrowers. It also prohibits “dual track” foreclosures, in which lenders pursue foreclosures while simultaneously negotiating loan modifications.

The new tenant and landlord protections will help to momentarily stave off the looming foreclosure crisis. More protections and laws will need to be passed as we head further into the recession.

Check back for more updates as the recession continues to impact tenants, landlords and the housing market.

Related article: Foreclosure moratorium extended by FHA, Fannie Mae, Freddie Mac

{kind=link}

This is all very confusing. As I read this voluminous law all I can see is things that apply to Tenants or owners who can not pay their rent/mortgage obligations. Where does that leave a landlord who just wants to have possession of his/her single family home property, do extensive remodel and maybe sell it, and the tenant is current with the rent, no contract violations and does not appear and or has not given notice of being affected by the pandemic? In such case is a 30/60 day notice to vacate against the law and or subject to outrageous penalties?

These laws combine to create a forced lender/borrower relationship between landlords and tenants, without borrower qualification and regardless of the borrower’s future ability to repay. It seems that government, acting as a middle-man, is on the edge of an unconstitutional taking from the landlord and wealth transfer to the tenant. To avoid such status, government says the landlord can eventually get a judgment against the tenant for the full amount due. But does that really avoid a taking?

In most cases where such rent postponements are deployed, the tenant already meets the legal qualifications of bankruptcy (liabilities exceed assets). So now we have an orchestrated scenario where the landlord is being forced to systematically loan more money by making future monthly advances to an already bankrupt tenant/borrower. It is absurd how government already paired up each rightful tenant borrower with an involuntary lender. It was determined that the mandated lender must be the landlord and the borrower is whomever he was renting to at a point in time. This is not how government typically funds mandates. How is government going to justify this through an ending scenario?

Landlords should not expect government to socialize all this tenant debt so landlords can be made whole. Instead, government will seek out some rationale why landlords should pervasively absorb such bad account receivables as a business expense. I predict there will become a new simplified mini-bankruptcy procedure, perhaps a one-page form that gets rubber-stamped. Then government will contend that tenant bankruptcies are a risk that all landlords freely accepted.

Thank you! Elderly Landlords who rely upon the income from their rentals/tenants cannot necessarily cover these loses.