Foreclosure is a procedure to recover the amounts owed on a debt by way of an orderly sale of property pledged as security for the debt. The foreclosure process is triggered by a default in payment or a breach of terms.

On the owner’s default, the foreclosure procedure is forced on the mortgage holder (the lender or carryback seller) as a result of the put option provision found in all trust deeds and California’s one-action rule for mortgage remedies. The put option grants an owner the right to default and force the mortgage holder to buy the property through foreclosure.

California is a nonjudicial foreclosure state. Simply, this means that mortgage holders may foreclose by a trustee’s foreclosure procedure, by way of a trustee’s sale. Nonjudicial foreclosures do not involve the court system, unlike judicial foreclosures. Nonjudicial foreclosures take much less time to complete, as the procedure and time periods for the different stages of foreclosure are already established by legislation. Further, nonjudicial foreclosure is usually less costly, as court costs and attorneys are not involved. [More on the nonjudicial foreclosure process on Card 2]

Further, anti-deficiency laws protect all homeowners from being pursued for additional money by the mortgage holder when the mortgage is foreclosed by a trustee’s sale and the property value is insufficient to cover the debt. A completed trustee’s sale becomes the sole remedy for recovering on any mortgage, even if the amount of the high bid accepted is less than the debt owed. [See Card 3]

In these cards, the term foreclosure always refers to California’s nonjudicial foreclosure.

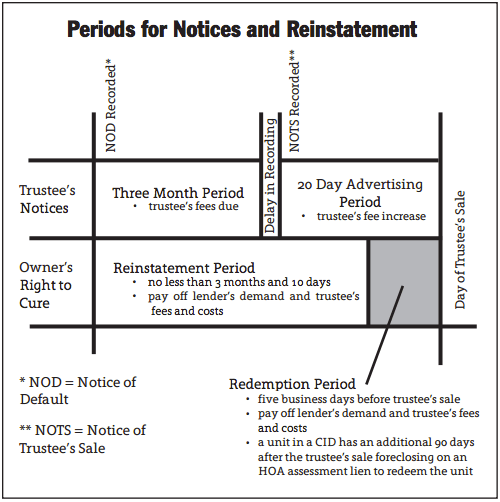

- The property owner is delinquent on their mortgage payments. This means a property owner has missed at least one payment. However, a mortgage servicer is very unlikely to classify a mortgage as delinquent before the payment is at least 30 days past due. On first-lien mortgages secured by a homeowner’s principal residence, the mortgage is to be at least 120 days past due before the mortgage holder may proceed to the next step in the foreclosure process. [12 Code of Federal Regulations §1024.41(f)(1)]

- The mortgage holder causes a notice of default (NOD) to be recorded, sending a copy of the NOD to the property owner. On one-to-four unit residential properties, a separate summary of the NOD is to be attached and sent to the property owner with the NOD. Once recorded, the NOD officially begins the foreclosure process. [See firsttuesday Form 471]

- The property owner’s right to cure money defaults and reinstate the mortgage lasts through the day before five business days prior to the date the trustee’s sale is held. The reinstatement period lasts for a minimum of three months and 20 days. During this time, the owner may halt the foreclosure process by paying the delinquent amounts due (including foreclosure charges). If they are unable to pay the amounts due, the time is used to research foreclosure alternatives. [Calif. Civil Code §2924(3)-(4); see Card 3]

- The mortgage holder causes a notice of trustee’s sales (NOTS) to be recorded any time following three months after the NOD is recorded. This includes posting the NOTS on the property itself and publishing the NOTS in an authorized news publication within the property’s court jurisdiction. On one-to-four unit residential properties, a separate summary of the NOTS is to be attached and provided with the NOTS. The summary is not required to be published.

- The owner’s redemption period begins five business days before the foreclosure sale is to take place, continuing until the sale is completed. During this time, the property owner is able to halt the foreclosure process by paying the remaining balance on the mortgage and all other amounts due, including foreclosure charges.

- The foreclosure sale takes place and the trustee’s deed is recorded, vesting title in the name of the buyer at the trustee’s sale.

In a normal real estate market, it takes four to five months to complete a nonjudicial foreclosure in California, from the recording of the notice of default (NOD)to the trustee’s sale. However, in the aftermath of the mortgage meltdown it took on average two to three times longer to complete the foreclosure process.

Fannie Mae and Freddie Mac require seven years to pass after foreclosure before the homeowner becomes eligible for financing. However, if the homeowner can prove extenuating circumstances (e.g. a job loss or health causes) then the seven-year period is reduced to three years.

No. Antideficiency law prohibits collection of any deficiency in a property’s value to cover the debt when the foreclosure is completed nonjudicially.

If the mortgage holder intends to pursue collection of a deficiency (on a recourse debt), they need to foreclose judicially.

Further, California’s one-action rule prohibits litigation to recover mortgage debt losses on a trustee’s foreclosure sale. Also, the rule requires the mortgage holder to first foreclose on the real estate before taking any other steps to collect.

It all depends on what type of mortgage the homeowner has.

There are two types of mortgage debt:

- nonrecourse; and

- recourse.

Nonrecourse debt, called purchase-money debt, includes:

- purchase-assist funding of money or services used to purchase or construct a homebuyer’s one-to-four unit owner-occupied residence secured by a mortgage of any priority on title (first, second or even third trust deeds); and

- seller-financing, also called an installment sale or carryback mortgage, on the sale of any type of real estate when the debt is secured solely by the property sold. [Calif. Code of Civil Procedure §580b]

Recourse debt is every other type of mortgage. This includes mortgages secured by:

- second homes;

- property containing five or more units; and

- nonresidential property.

Further, if a home equity line of credit (HELOC) was taken out and used for purposes other than the purchase, construction or remodel of a one-to-four unit, owner-occupied residence then it is considered recourse debt.

Refinancing of a purchase-money mortgage retains its purchase-money nonrecourse status barring collection by a money judgment if:

- the mortgage holder of the original purchase-money debt is the refinancing lender [Union Bank v. Wendland (1976) 54 CA3d 393];

- the refinanced debt is substantially the same debt as the original purchase-money debt [DeBerard Properties, Ltd. v. Lim (1999) 20 C4th 649]; and

- the refinanced debt is secured by the same property as the original purchase-money debt. [Goodyear v. Mack (1984) 159 CA3d 654; CCP§580b]

In absence of any of the three conditions (e.g., cash-out refinances), the refinanced debt is considered recourse debt. Thus, the refinancing as recourse debt is subject to a mortgage holder’s money judgment for any deficiency in the value at the time of their judicial foreclosure sale. Remember, a money judgment is not permitted on any type of mortgage following a trustee’s foreclosure sale.

One exception: the Federal Housing Administration (FHA) and Veterans Administration (VA) have recourse against the homebuyer who signed an FHA or VA guarantee agreement. The FHA and the VA rarely pursue deficiency judgments; however they have the legal right to do so. [Carter v. Derwinski (9th Cir. 1993) 987 F2d 611]

The most significant thing to remember is: mortgage holders are only able to pursue a deficiency under a recourse debt if the mortgage holder chooses to complete a judicial foreclosure action.

Thus, the homeowner need not fear further collection efforts by a mortgage holder so long as the mortgage holder pursues and completes a nonjudicial foreclosure by a trustee’s sale.

The most common alternative to foreclosure is to sell the property and pay off the mortgage with the net sales proceeds. However, when the property’s value is less than the mortgage amount the owner’s sale of the property is called a short sale.

To dispose of a property in a short sale, the owner needs the mortgage holder to agree to accept the net proceeds from a sale of the home at its current fair market value (FMV) as satisfaction for the remaining mortgage amount owed. To start the process, the property owner hires a real estate agent to list their property for sale.

The benefits of a short sale are twofold:

- for the mortgage holder, a short sale saves money as the process tends to be quicker and often the amount received is higher than at a foreclosure sale; and

- for the property owner, a short sale usually results in less harm done to their credit score, as they spend less time in default than when their home is in the foreclosure process. Also, they avoid any “moral shame” they may feel from a foreclosure (though financially the result is nearly the same for the owner).

However, a short sale still results in the property owner losing their property. On a recourse mortgage (such as with a commercial property or a home mortgage that was refinanced), they will also be dealing with the possibility of reporting discharge of indebtedness income when reporting the sale at tax-time.

Another option also involving the loss of the property is a deed-in-lieu of foreclosure, commonly called a “friendly foreclosure.” In this case, the property owner voluntarily hands the mortgage holder a grant deed conveying title to them. This saves the mortgage holder time and money since they don’t have to deal with the costs of a foreclosure sale. Further, mortgage holders sometimes will offer relocation assistance.

For assistance in keeping a home, Keep Your Home California is a state- and federally-funded resource for California residents facing foreclosure. They provide alternatives such as:

- unemployment mortgage assistance;

- mortgage reinstatement assistance;

- principal reductions (cramdowns); and

- transition assistance when the homeowner has completed a short sale or deed-in-lieu of foreclosure.

The California Homeowner Bill of Rights, enacted January 1, 2013, provides protections for homeowners going through the foreclosure process. These protections are in place through January 1, 2018, and include:

- Dual track foreclosures are restricted. This prohibits a mortgage servicer from continuing the foreclosure process if the homeowner has applied for a loan modification. The foreclosure process may only resume only if the loan modification application is formally denied in writing. [CC §2923.5(B)]

- Single points of contact are to be provided by mortgage servicers to homeowners pursuing foreclosure alternatives. [CC §2923.7(a)]

- Verification of foreclosure documents is required. A mortgage servicer who records and files “multiple” unverified foreclosure documents may be fined up to $7,500 per violation. These documents include an NOD, an NOTS, assignment of trust deed or substitution of trust deed. Each of these documents must be verified by review of substantial evidence of the mortgage servicer’s right to foreclose. [CC §2924.17(c)]

- Tenants of foreclosed homes are also protected by the Homeowner Bill of Rights. Upon completion of the trustee’s sale, the new owner must honor an existing lease if it has a fixed-term. If the home is to be occupied as a principal residence, the new owner may serve the tenant with a 90-day eviction notice. [CC §2924.8(a)(1); see Card 6]

The Homeowner Bill of Rights also provides relief for after a foreclosure sale has taken place.

Violations of foreclosure law by mortgage servicers may result in money paid to the homeowner, sufficient to cover “economic damages.” This amount may include the cost of attorney fees and court costs. [CC §2924.12]

Residential tenants have several protections when their rented residence is sold at a foreclosure sale to a new owner, called an owner-by-foreclosure.

The Protecting Tenants at Foreclosure Act (PTFA), enacted in 2009, aims to protect residential tenants caught between their defaulting landlord and the mortgage holder.

During this time, the tenant has the right to enforce the terms of their rental or lease agreement entered into with the prior owner. Further, a tenant at the time of the foreclosure sale is entitled to live out the remainder of the lease term if:

- the tenant holds a bona fide lease agreement;

- the lease agreement was entered into before title was transferred to the owner-by-foreclosure; and

- the owner-by-foreclosure is not going to occupy the property as their primary residence. [Public Law 111-22 §701, §702, §703]

A lease agreement is bona fide “only if the rental or lease agreement calls for rent that is substantially the fair market rent for the property.” [12 United States Code 5220]

On the other hand, the owner-by-foreclosure (whether the mortgage holder or a different person) may choose to occupy the property as their primary residence, or they may sell the property to buyers who will occupy the property. When a buyer will occupy the property, the tenants are then served with a 90-day notice to quit due to foreclosure. [CC §2924.8(a)(1); see firsttuesday Form 573]

When the home is encumbered by a mortgage insured by the Federal Housing Administration (FHA) the tenants receive further protection. A mortgage holder in the process of foreclosing an FHA-insured mortgage serves the tenants with a Notice of Pending Acquisition (NOPA) within 60-90 days prior to the scheduled foreclosure sale. PTFA protections also apply to FHA-insured mortgages.

When a property sells at a foreclosure sale for less than the amount owed on the mortgage, the difference is initially considered taxable income. This difference is called discharge-of-indebtedness income by the Internal Revenue Service (IRS), and cancellation of debt by California’s Franchise Tax Board.

From 2007-2013, individuals whose homes were foreclosed upon were able to skip reporting this “gain” as taxable income due to a federal and state exemption (called the Mortgage Forgiveness Debt Relief Act). This exemption expired at the end of 2013.

However, nonrecourse debt under California mortgage law is not taxable. When a mortgage is nonrecourse, the homeowner wiped-out by a foreclosure sale does not report any discharge-of-indebtedness income when filing their state and federal tax returns. [More on recourse and non recourse debt on Card 3]

Strategic default is when a homeowner intentionally defaults on a mortgage even though they have the capacity to pay. The default forces the mortgage holder to foreclose to collect the mortgage debt.

Typically, homeowners who benefit most from strategic default are deeply underwater, owing significantly more on their mortgage than their home’s current FMV. Their underwater homes (black hole assets) are a drag on their financial situation and the broader economy as they are unable to relocate for jobs, education, health purposes and like circumstances. Thus, a strategic default allows them to get rid of the home, move and start over.

The owner-by-foreclosure is responsible for maintenance of a property following a foreclosure sale. If the owner does not maintain the property, California law authorizes local agencies to assess penalties.

If a property owner receives notice of a maintenance violation, they are required to commence corrective maintenance within 14 days of the notice. All maintenance is to be completed within 30 days of the notice. Failure to commence or complete maintenance within these timelines subjects the property owner to a fine of up to $1,000 a day. [California Civil Code §2929.3]

Further, if the property acquired through foreclosure is already in a state of disrepair, the new owner has 60 days to correct any health and safety violations on the property. However, the local agency may shorten the 60-day time period when the violation poses an immediate threat to the health and safety of the public. [Health and Safety Code §17980]

Foreclosures are an indicator of the financial condition of state, regional or local housing markets. The economy is in a state of recession (or stagnant recovery) when foreclosures compose a significant portion of the housing market’s activity.

During the 2008 recession, foreclosures peaked at nearly 140,000 foreclosure home sales completed in a single quarter in California. For historical reference, the average number of home foreclosures completed per month in a healthy California housing market is 3,000-3,500. [To view a chart displaying historical and current trends in foreclosure sales, see Card 11]

The clearest effect a large number of foreclosures have on the housing market is the drag on home prices. Initially, a huge increase takes place in the multiple listing service (MLS) supply of homes. Following the 2008 recession, low buyer demand caused listings to linger and prices to dwindle.

Buyers tend to pay less per square foot for properties which have been foreclosed because of the poor condition in which the properties are often left. Homeowners who know their property is going to be lost to foreclosure generally neglect maintenance when they default.

Some homeowners even commit intentional waste of the property, an action which can lead to an impairment of the mortgage holder’s security in the home. Here, the mortgage holder is allowed to sue the homeowner and obtain a money judgment for lost property value due to waste committed by the owner in bad faith.[Cornelison v. Kornbluth (1975) 15 C3d 590; see firsttuesday Form 550 §6.8 and 552 §7.4]

Further, the end of the foreclosure process is not the end of its negative effect on the housing market. These foreclosed homes continue on as shadow inventory, made up of homes foreclosed but not yet listed on a MLS. During periods of massive foreclosure activity in their mortgage portfolios, mortgage holders delay listing and selling foreclosed homes to avoid reporting the loss on their balance sheets.

The shadow inventory was a big concern from about 2008-2012. The concern abated in 2012 when a wave of speculators began buying up REOs, then buying homes at foreclosure sales reducing the shadow inventory of REO properties.

True, mass speculator purchases reduced the REO shadow inventory resulting from foreclosures. But in reality, this shadow inventory was merely shuffled from the hands of mortgage holders to short-term absentee owners. Speculators are in it for the quick profit. Thus, the REOs they purchase will simply re-emerge for sale shortly after the speculator’s purchase.

- For a brief pamphlet on foreclosure from the Bureau of Real Estate (BRE), see: Foreclosure information for homeowners.

- For a more detailed explanation on foreclosure from the BRE, see: A homeowner’s guide to foreclosures in California.

- To read about foreclosure trends and view charts displaying past and current trends in foreclosure sales and notices of default, see the firsttuesday article NODs and trustee’s deeds: almost back to normal.

- For more on anti-deficiency protections, see the firsttuesday article Cover for your homeowner: an anti-deficiency primer.

- For more on the different effects a foreclosure and short sale have on credit scores, see the firsttuesday article: Fair Isaac Corporation score: effects of foreclosure vs. foreclosure alternatives.

- For more on tenants’ rights after foreclosure, see the firsttuesday article: Case in point: Is a lender who forecloses and acquires residential property required to defend an existing tenant’s right to their unit with another tenant interferes?

- For more on tenant’s rights after foreclosure of an FHA-insured mortgage, see the firsttuesday article: Tenants retain rights on FHA foreclosures, and more.

- For more on required maintenance of owners-by-foreclosure, see the firsttuesday article: Maintenance of property acquired by foreclosure.

- For more on negative equity, see the firsttuesday article: Underwater homes decrease in California.