This form is used by a trust deed broker when employed by the holder of a trust deed note, to act as their exclusive agent to locate an investor and negotiate the terms for the sale of the note.

The trust deed broker’s investment opportunities

Trust deed brokers solicit individuals who invest their cash funds in interest-bearing assets to consider investing in trust deed notes. With yields higher than mortgage backed bonds (MBBs), individuals invest directly in the ownership of trust deed notes, sometimes called paper, secured by real estate in low-risk loan-to-value conditions rather than purchasing MBBs or dividend stocks.

A trust deed investor, acting independent of Wall Street’s MBB market, invests in trust deed notes. To invest in trust deed notes, this class of investor uses a trust deed broker, rather than an investment banker, to assist them to:

- arrange a business-purpose mortgage evidenced by a note in favor of the investor making the loan and secured by a trust deed lien on real estate, a process called origination (distinguished from origination in the context of a consumer-purpose mortgage);

- purchase an existing trust deed note, called an absolute assignment; or

- make a mortgage-backed loan (MBL) evidenced by a note in favor of the investor secured by an existing note and trust deed held by the borrower, called hypothecation or collateral assignment.

Stages of trust deed investment

Whether an investor purchases a trust deed note or makes a loan collaterally secured by a existing trust deed note held by the borrower, a prudent investor and a competent trust deed broker undertake a due diligence investigation. This effort determines the sufficiency of the borrower’s creditworthiness and the property value as sufficient to justify funding the origination or purchase of a trust deed note or collateralized note. [See RPI e-book Mortgage Loan Brokering & Lending, Chapter 43]

The loan broker’s due diligence effort is a condition met for every trust deed investment as an agency duty owed the investor to document and analyzes the risks of loss which may be present in the investment, including:

- the creditworthiness of the signatories to the trust deed note for propensity to repay amounts when due;

- the real estate provided as security described in the trust deed (physical condition, title profile, location, rental value, property value) to enforce satisfaction of the note;

- the payment history on any trust deed note purchased or collaterally assigned; and

- title insurance guaranteeing the trust deed status and position on title.

An investor’s use of a trust deed broker retained under an employment agreement to perform the due diligence investigation and analysis determines the investor’s risks in funding the origination or purchase of a trust deed investment. Also, a trust deed broker typically has an inventory of listed trust deed notes available with a complete marketing package delivered under a transmittal letter for an investor to consider. [See RPI Form 233]

The trust deed listing agreement

Trust deed noteholders, particularly carryback sellers, often decide to sell their trust deed notes. The task of cashing out a trust deed note investment requires a trust deed investor to be located who is interested in acquiring the note.

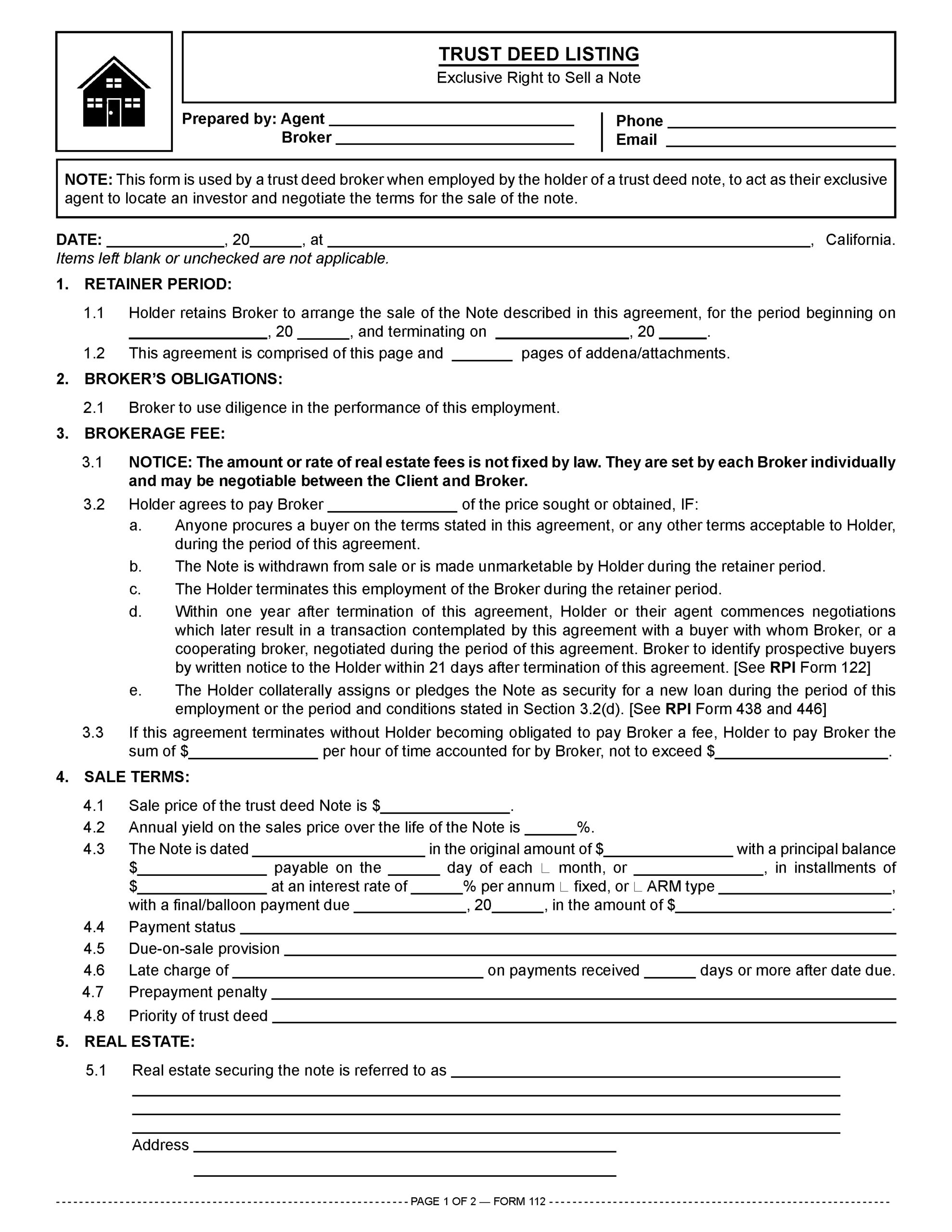

Here, a trust deed broker is employed to locate an investor and negotiate the sale of a trust deed note for a fee. To achieve this employment, the broker enters into a trust deed listing agreement with the noteholder. [See RPI Form 112]

The listing agreement spells out what the noteholder can expect the broker to do and provides the broker with the necessary written fee agreement to provide certainty about employment activities and enforcement of the fee. [See RPI Form 112]

The broker employed always has the general duty to disclose to both transaction participants all facts and terms of the debt to be evidenced by the note and trust deed or a trust deed note to be sold. The disclosures include information that may affect the willingness of the noteholder or the investor to enter into a transaction for the sale or hypothecation of the trust deed note, collectively called material facts. [Barry v. Raskov (1991) 232 CA 3d 447]

The listing agreement calls for the noteholder’s disclosure of all material facts regarding the trust deed note to be assigned. In turn, the broker is duty bound to disclose these facts to a prospective trust deed investor on commencement of negotiations — up front — to acquire or originate a the trust deed note.

When a broker enters into an agreement with a trust deed noteholder to be employed to act as their sole agent for a fixed period of time, the broker uses the Trust Deed Listing — Exclusive Right to Sell a Note published by Realty Publications, Inc. (RPI). The form allows the broker and their agents to locate a trust deed investor and arrange a sale of the note and trust deed. [See RPI Form 112]

The Trust Deed Listing — Exclusive Right to Sell a Note discloses:

- the terms of the trust deed note, including:

- the asking price for the trust deed note [See RPI Form 112 §4.1];

- the annual yield on the asking price over the remaining life of the note [See RPI Form 112 §4.2];

- the original amount, principal balance, payment terms and interest rate of the note [See RPI Form 112 §4.3];

- any due-on-sale, late charge and prepayment penalty provisions in the note or trust deed [See RPI Form 112 §4.5 – 4.7]; and

- the priority of the trust deed on title to the described real estate [See RPI Form 112 §4.8];

- the identification of the real estate securing the note [See RPI Form 112 §5.1];

- the amount and terms of all encumbrances on the real estate including property taxes, assessments, trust deeds and judgments [See RPI Form 112 §6]; and

- any personal property included as additional security for the note. [See RPI Form 112 §7]

Form navigation page updated 11-2023.

Form-of-the-Week: Trust Deed Listing, and Purchase Agreement for Note and Trust Deed — Forms 112 and 241

Form-of-the-Week: Trust Deed Listing – Exclusive Right to Sell a Note and Consent for Use of Electronic Documents and Digital Signatures – Forms 112 and 109

Feature Article: MLO recession survival guide Part 2: Buyers’ agents and underwater home sellers

Feature Article: Arranging hard money trust deed mortgages

Feature Article: Escrowing a note and trust deed assignment

Book: Mortgage Loan Brokering & Lending, Chapter 43: Note and trust deed assignments