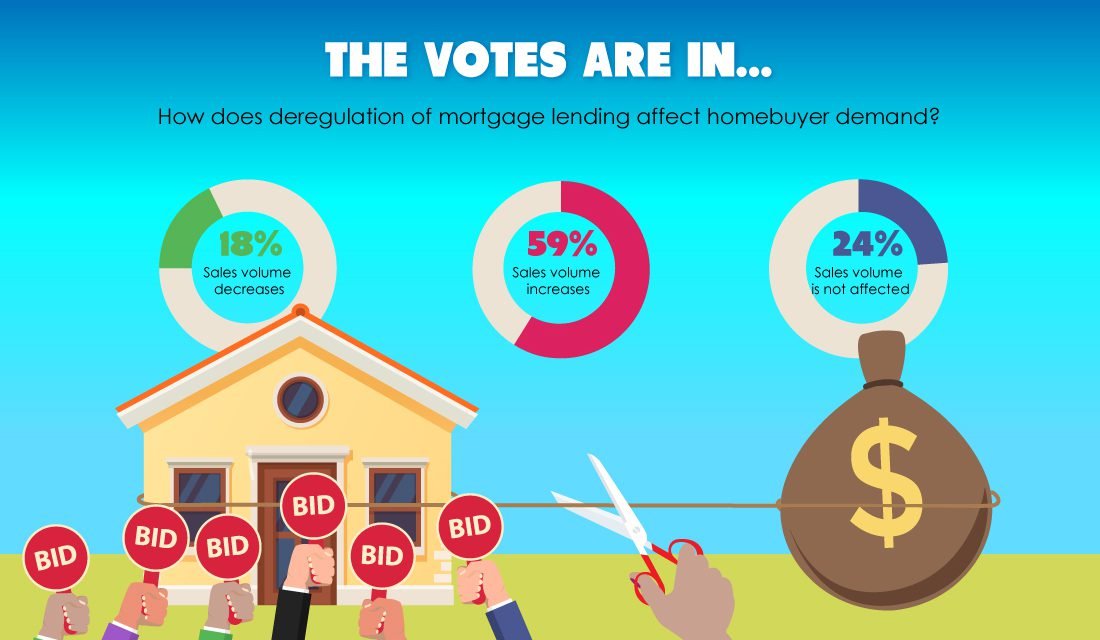

In a firsttuesday poll from May, a question was posed to readers: how does deregulation of mortgage lending affect homebuyer demand?

Of the readers who responded:

- 59% said sales volume increases with mortgage deregulation;

- 24% said sales volume is not affected; and

- 18% said sales volume decreases.

More than half of respondents firmly believe deregulation of mortgage lending causes sales volume to rise, while the remaining 42% are split between seeing no impact — and the minority of respondents, who expect sales volume to decrease with deregulation.

For comparison, a similar poll was conducted in 2019. The responses fell roughly along the same lines, displaying an unwavering attitude toward the effects of mortgage deregulation on sales volume.

With small disparities in percentages, these poll answers were eerily similar — indicating little change on stance within the last three years.

Related article:

Deregulation may boost sales volume — but at what cost?

Deregulation of mortgage lending often leads to an increasingly fluid market, driving up the volume of sales. Loosening mortgage credit enables more people to qualify for mortgages — often forcing big risk on the market.

Mortgage regulation was at an all-time low at the point during the Millennium Boom. During the early-2000s, lenders were eager to qualify anyone with a pulse for a mortgage. As a result, many ended up defaulting once home values plummeted. At the time, lenders were not under proper supervision, and thus were able to harm consumers through predatory lending schemes. More harm than good was done, as the Boom was a major cause of Great Recession and foreclosure crisis, which eliminated trillions of dollars in asset wealth across the nation.

Our firsttuesday readers are correct: sales volume did rise during the Boom when regulation was nonexistent. It was, however, to the housing market’s greater detriment.

Regulation on mortgage lending is what creates a safe mortgage market. When lenders pay no mind to whether applicants have the ability to repay their mortgages, mortgage defaults are a near certainty.

Mortgage deregulation increases sales volume, but at a price not worth paying.

Related article:

{kind=link}