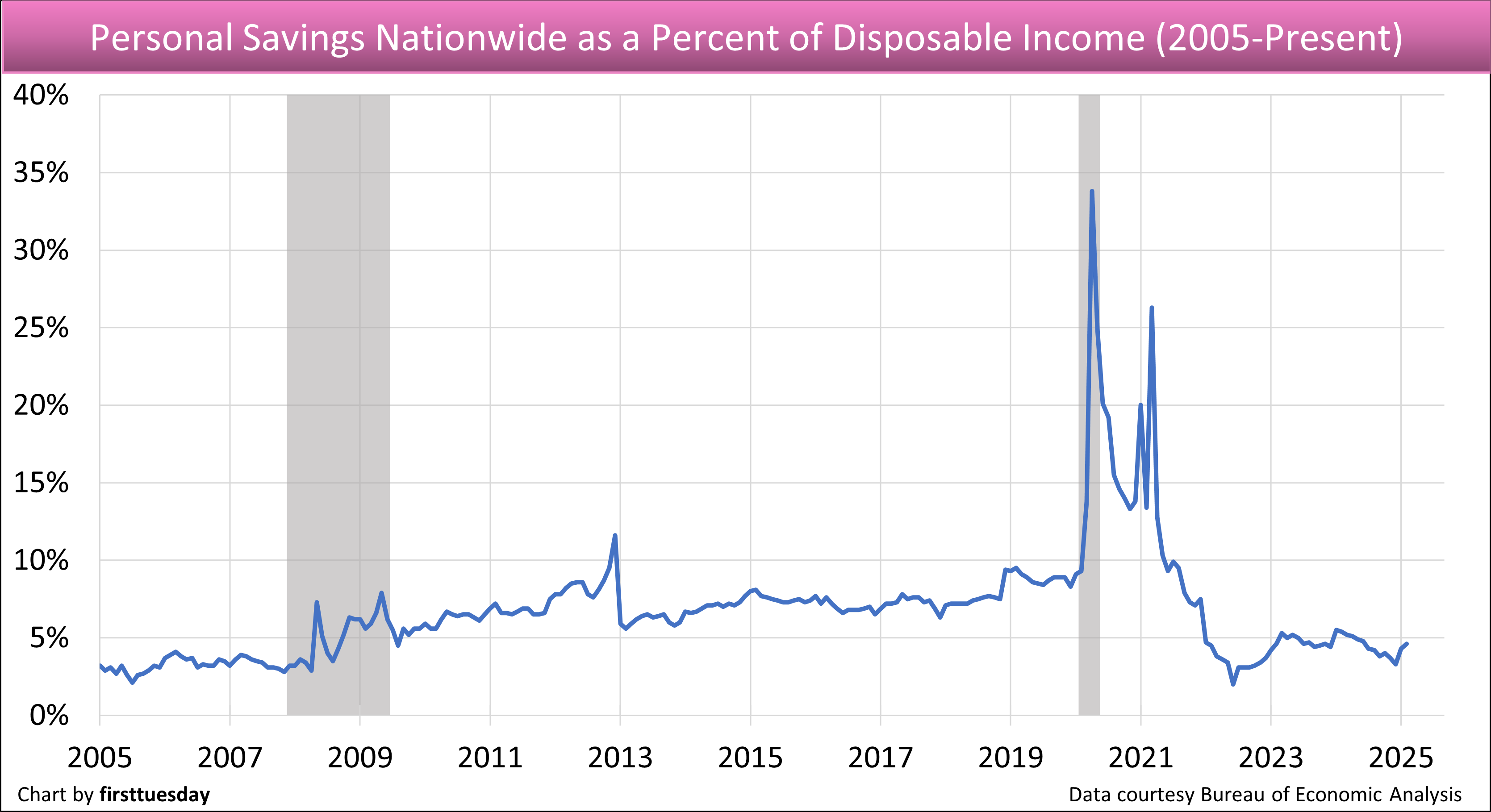

The national personal savings rate is inching back up from 2022’s decade-low 2% rate, at 4.6% in February 2025. An 8% to 10% savings rate would make job holders economically more viable — sufficient to improve standards of living, be less stressed as a population and actually buy a home with more than 20% down — a solvency issue perplexing the typical job holder.

In 2022, the savings rate plummeted by necessity, as households struggled to make ends meet under pressure of the highest consumer price inflation since the 1980s. This followed two years of covid-era volatility, when savings jumped to a record 34% of disposable personal income in April 2020, driven by the first round of stimulus payments, which many put directly into savings.

For perspective, savings bottomed near 2% in 2005 when consumer confidence was high on Millennium Boom fumes, but stayed above 5% in the recovery following the 2008 recession.

Here in California, the room for saving is even narrower due to the high cost of living. While the California savings rate is not available, it is lower than the national average. This disparity chips away at the ability to accumulate savings sufficient to cover emergencies, let alone enough for a down payment on a home.

Looking ahead in 2025, Californians will continue to rein in spending in anticipation of reduced income during the current shadow recession. Further, the current international trade and migration chaos is most likely to bring on widespread job losses and price hikes. Worse, no individual stimulus payments as occurred in 2020 to buoy personal income and business operations are likely to take place.

Watch for job losses to begin by mid-2025 triggered by economic uncertainty over the tariff-induced trade war, a killer of economies large and small, primarily adversely affecting small business operations. Job deterioration and inflation will bring on more savings and less spending.

However, the trade war presently being fought totally interferes with the ability to ascertain just when the coming recession will take place, much less a recovery. But an increase in savings is the result of general uncertainty about the economy.

Updated April 28, 2025.

Chart update 04/28/25

| 2024 | 2023 | 2022 | |

| Annual average personal savings rate | 4.5% | 4.7% | 3.5% |

Chart update 04/28/25

| Q4 2024 | Q3 2024 | Q24 2023 | |

| Personal Savings Rate | 3.7% | 4.1% | 4.5% |

Data courtesy of United States Department of Commerce: Bureau of Economic Analysis

Gray bars indicate periods of recession.

*Data averaged through December 2024.

As mortgage rates trend higher, a cyclical process begun in 2013, real estate demand is driven by how much money potential buyers save. What does this mean for future home sales?

Trends in saving

The 20% down payment was once the gold standard of residential mortgage originations. During the fevered years of the Millennium Boom, the standard became a quaint novelty. Buyers (and lenders) got used to the easy days of purchasing a home with 0% down, and closing costs were either seller-paid or mortgage-lender financed.

Unsurprisingly, this was reflected in the personal savings rates of the period. From 1952 to 1990, personal savings as a percentage of disposable income were around 8-10%, according to the Federal Bureau of Economic Analysis (BEA). During the Millennium Boom, savings dropped to nearly 0%, a 50-year low.

However, the 2008 Great Recession ushered reality back through the front door. The 1,100,000 California homeowners who felt the trauma of the great recession housing crash fast found wisdom in stockpiling cash. The personal savings rate leaped up to 6% within a year.

The personal savings rate was at 3.7% in Q4 2024, close to double the 2022 low, but still down from the same quarter a year earlier.

As we head into a recessionary period, expect to see a greater reliance on savings emerge, with households saving when possible to cushion themselves from the expected economic turbulence of a recession.

Related article:

Savings to continue?

Over the last few decades, savings has followed a path conversely proportionate to consumer confidence. When consumer confidence runs high, the rate of personal savings falls as people spend more than they earn by taking on debt, forgetting the lessons of the most recent past recession. When consumer confidence is relatively low, personal savings rises. A financial “comfort zone” is accommodated either way, until it isn’t.

Related article:

Homebuyers feel ready and willing to buy, but not financially able

{kind=link}