Why rent when you can buy?

Renters get into the homeownership game for many reasons, whether to fulfill the almost genetic American Dream ideal, simply to own the space they occupy or to place a bet on the future of real estate. For real estate agents, one convincing tool readily available is to share the concrete financial benefits of homeownership with those who presently rent their shelter.

Real homeownership numbers talk more loudly than broad assumptions and pro forma generalizations about:

- tax savings from interest deductions;

- equity buildup through mortgage amortization;

- an inflationary hedge; and

- appreciation profits.

And how do forward-thinking agents provide this higher level of concrete data? Get functional. Act smart and show potential homebuyers the actual dollars and cents they accumulate through homeownership — the same dollars and cents you will help them put in their pockets. Thus, persuasively illustrate the benefits of buying by factual, written evidence.

Here, we outline a straightforward way for you to efficiently compare monthly costs of owning versus renting by use of an interactive form. This includes a presentation of the dollar mortgage deductions and tax savings attained based on your buyer’s home price, down payment and tax bracket. All critical data contained in the form is presented as monthly and annual figures that your buyers will quickly comprehend.

Monthly costs and savings

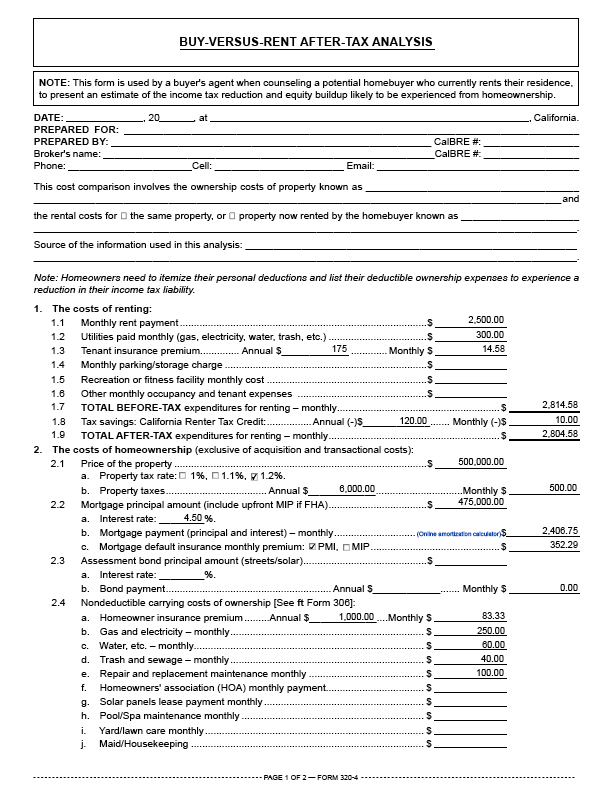

To start, prepare the Buy-Versus-Rent After-Tax Analysis published by RPI (Realty Publications, Inc.). With it you compare the future homebuyer’s current costs of renting against likely homeownership costs (and savings). [See Figure 1, pre-filled RPI Form 320-4]

In application, you use the Buy-Versus-Rent form in one of two ways:

- As a hypothetical situation when your potential buyer currently rents and does not have a clear vision about owning a home. In this case, review with them the costs of homeownership section to show the estimated operating and ownership costs for a home similar to the one they now rent. [See Figure 1, pre-filled RPI Form 320-4 §2]

This application of the form is best suited for first-time buyers who are on the fence about graduating into ownership, but are willing to start the process of looking for a property.

- Use the form to summarize a particular home your prospective buyer actually envisions buying. Then, use the price the homebuyer intends to pay for the property and the interest rate (plus the rate of any mortgage default insurance premiums (MIPs/PMIs)) they will pay on a mortgage. The actual operating costs for a home under consideration are readily available from the seller, and if they are not willing to cooperate, an estimate will do.

This application of the form is best suited for buyers who have already selected a property or have a specific type of property in mind.

As the future homebuyer will see in the analysis, the biggest savings from homeownership come initially from annual tax savings – a direct government subsidy to encourage homeownership and mortgages. Over time, equity buildup and growth predominate to develop long-term wealth.

This financial knowledge allows the homebuyer to wrap their head around the idea that even if their total mortgage payment will be higher than their current rental payment, they will likely save money by owning. This savings concept needs to be illustrated with dollars so buyers fully grasp this somewhat unintuitive fact — the tax-subsidy produces the savings.

Finally, the form concludes with a total financial benefit analysis and a summary of wealth accumulation over ten years of ownership. Thus, the buyer is left with a long-term perspective which exhibits all the financial benefits of owning versus renting. [See Figure 1, pre-filled RPI Form 320-4 Summary Section]

Using the form

A pre-filled copy of Form 320-4 which provides a sample scenario is provided below. In the example, the future homebuyer pays monthly:

- $2,500 in rent;

- $300 in utilities; and

- $14.58 in renter’s insurance.

The home they are interested in purchasing is $500,000 and they have been approved for a fixed rate mortgage (FRM) at 4.5%. Their down payment is $25,000, or 5% of the purchase price. Therefore, they need to purchase MIP/PMI, which is also included in the sample situation.

Plugging in the relevant information into the form (including the property tax rate of 1.2% and the estimated costs of utilities) produces the comparison of the cost of renting versus owning.

The calculations assume a 3.5% annual gain in property value (an historical average) which will oscillate above or below each year. The calculations further assume the homebuyer will own the home for ten years before selling.

The initial comparison is based on out-of-pocket cash expenditures of renting and owning. It shows that owning costs $5,333 more initial cash expenditures each year than renting. In contrast, when tax savings are reduced from out-of-pocket costs, the homebuyer immediately goes from red to green, saving a total of $3,395 in the first few years. The tax savings decrease over time as principal is paid down, reducing interest deductions, but the cash savings after taxes over ten years exceeds $30,000.

To calculate the costs and savings of your client’s own potential home purchase, all you need to gather and enter is information about the:

- purchase price;

- property tax rate;

- utilities;

- mortgage information; and

- the homebuyer’s current housing costs for comparison.

Armed with this data, and the form will do the math for you.

Figure 1

Mortgage points, interest recovered at the buyer’s tax rate

The discount — points — paid to obtain a mortgage to fund the purchase of the homebuyer’s primary residence are tax deductible. In turn, taxable income is reduced and the amount of income tax paid is reduced. Generally, the tax savings is the percentage amount of the deductions at the buyer’s tax bracket rate. [See Figure 1, pre-filled RPI Form 320-4 §6]

When the points paid on a purchase-assist mortgage for the purchase of the buyer’s primary residence are identified as points on the closing statement, the buyer may deduct the entire amount in the year of purchase.

The Internal Revenue Service (IRS) has prepared a handy flowchart to help homeowners and their agents with the calculations. However, the RPI form does the calculations automatically on the entry of the critical base information on a proposed purchase and mortgage transaction.

Property taxes and assessments

An agent also needs to inform their potential homebuyer about property taxes. Property taxes are another deductible cost permitted for ownership of a personal residence. These are paid based solely on the real estate’s purchase price and the local annual tax rate, and future consumer inflation with a 2% cap, regardless of future value.

For example, someone who purchases a home today for $500,000 will pay nearly twice as much property tax as someone who purchased a similar home in that neighborhood for $250,000 years earlier. For more information, see Proposition 13, explained. [See Figure 1, pre-filled RPI Form 320-4 §2.1(b)]

However, while property taxes are a cost of ownership, they also come with a tax deduction, a further government subsidy to encourage homeownership. [See Figure 1, pre-filled RPI Form 320-4 §4.1(d)]

The property tax deduction reduces the homeowner’s taxable income under the standard income tax (SIT) rules. In turn, the homeowner saves money by the resulting decrease in the amount of income taxes paid to the state or federal government. For wealthier homeowners who are subject to alternative minimum tax (AMT) payments, the property tax deduction is not available.

On the other hand, special assessment bond payments are not taxes (though the installments of principal and interest are paid to the tax collector). Rather, they are liens imposed on real estate to repay bonds that financed the construction of public improvements that added value to the property and surrounding area. These typically include sidewalks, sewers, streets, parks, etc. [See Figure 1, pre-filled RPI Form 320-4 §2.3]

Special assessments are not based on the property’s value, but on the proportional benefit the adjacent and area-wide improvements grant to the property. Further, special assessments are principal and interest payments on bonded debt, the interest accrued and paid being deductible since the assessment lien is a mortgage on the home. [See Figure 1, pre-filled RPI Form 320-4 §4.1(b)]

Annual mortgage interest tax deduction

The mortgage interest deduction essentially reduces the homeowner’s combined state and federal taxes by an amount ranging from 15% to 35% of their monthly mortgage payment (based on the owner’s tax bracket). [See Figure 1, pre-filled RPI Form 320-4 §4.1(a)]

Interest deductions on home mortgages are only allowed for interest which has accrued and been paid, called qualified interest. [Internal Revenue Code§163(h)(3)(A)]

To qualify for interest deductions, the home mortgage needs to:

- fund the purchase price or finance the cost of substantial improvements on the owner’s principal residence or second home; and

- be secured by either the homeowner’s principal residence or second home. [IRC §163(h)]

To qualify as a principal residence, the home needs to be:

- the place of residence for the homeowner or the homeowner’s immediate family during the majority of the year;

- located close to the homeowner’s place of employment and banks which handle the homeowner’s accounts; and

- the same address used for tax returns. [IRC §§163(h)(4)(A)(i)(I), 121]

A second home is defined as any residence selected by the homeowner from year to year, which may include mobile homes, recreational vehicles and boats. The homeowner qualifies for the mortgage interest tax deduction for the second home as long as they do not rent out the second home too much of the time.

When the second home is rented out for portions of the year, the homeowner still qualifies for the mortgage interest deduction if they occupy the rental property for the greater of:

- 15 days or more; or

- 10% of the number of days the residence is rented. [IRC §280A(d)(1), 163(h)(4)(A)(iii)]

Finally, home improvements qualify as substantial if they:

- add to the property’s market value;

- prolong the property’s useful life; or

- adapt the property to residential use. [IRC §163(h)(3); Temporary Revenue Regulations §1.163-8T; Internal Revenue Service Publication 936]

If the home qualifies for the deduction, interest on the first and second home mortgages (and property taxes) is deducted from the homeowner’s adjusted gross income (AGI) as an itemized deduction. Thus, the mortgage interest deduction directly reduces the homeowner’s taxable income, the amount on which taxes are calculated under different brackets and paid.

The exception is for high income earners. Interest paid on mortgages used to purchase or substantially improve the homeowner’s first or second home is deductible up to a ceiling amount on mortgage balances up to:

- $1,000,000 for an individual or couples filing a joint return; or

- $500,000 for a married individual filing separately.

Interest accrued and paid on home equity loan amounts up to $100,000 which were used for purposes other than home improvements are also deductible.

The mortgage interest tax deductions apply under both the SIT and AMT reporting rules for setting the amount of income tax due.

Editor’s note — For more on the mortgage interest deduction, current first tuesday students can access Tax Benefits of Ownership Chapter 1: Home loan interest deductions from the Realtipedia within their Student Homepage.

Mortgage default insurance is deductible

When a homebuyer puts down less than 20% of the purchase price, they need to provide the lender with mortgage insurance coverage to protect against the risk of default and foreclosure.

If the homebuyer has a Federal Housing Administration (FHA)-insured loan, this coverage is called mortgage insurance premium (MIP). The mortgage insurance on Department of Veterans Affairs (VA) loans is called a funding fee.

Private mortgage insurance (PMI) is mortgage insurance covering conventional mortgages.

The premiums paid by the homeowner on mortgage insurance are tacked onto the homeowner’s monthly mortgage payment. Thus, the homeowner essentially experiences a higher mortgage rate to cover the lender’s risk of loss due to the homeowner’s default. Importantly, mortgage insurance payments are deductible, another form of government subsidy similar to the mortgage interest deduction. [See Figure 1, pre-filled RPI Form 320-4 §4.1(c)]

However, mortgage insurance is only deductible by the less wealthy among us — if the homeowner has an AGI greater than $109,000 (or $54,000 if married and filing separately), the mortgage insurance premium is not deductible. Further, if the homeowner’s AGI is $100,000-$109,000, the amount of mortgage insurance they deduct is reduced. [IRS Publication 936]

Time to sell: principal residence profit tax exclusion

It’s also important to tell your potential homebuyer about the principal residence profit exclusion (also called the §121 profit exclusion). This allows an owner of their principal resident to take a profit due to an increased price of the property on a resale and avoid paying taxes on the profit – up to $500,000 in profit for a couple.

On a resale, the sellers are required to have owned and occupied the property as their principal residence for at least two years during the five-year period prior to closing the sale to exclude profit up to $500,000 from income taxes. [IRC §121(a), 121(b)(1)]

To calculate the amount of profit taken on a sale, the seller subtracts their cost basis in the property – usually the price they paid for the property – from the net sales price, using the following formula:

sale price – cost basis = profit

Each owner who qualifies for the exclusion may avoid tax on up to $250,000 of their profit on the home sale. Co-owner spouses may qualify for profit exclusion up to $500,000.

Some rules and exclusions to the rule apply for those with home offices, and those who move due to personal difficulties without satisfying the two-out-of-five-years requirement. For more information, see The principal residence profit exclusion, explained.

{kind=link}