What’s the main reason your first-time homebuyers choose to buy instead of rent?

- Pride of ownership. (45%, 10 Votes)

- To save money. (32%, 7 Votes)

- For investment purposes. (18%, 4 Votes)

- Other. (5%, 1 Votes)

Total Voters: 22

Homebuyers who own their home for two years or longer save money over renting. This analysis compares homeownership costs like taxes, interest rates and acquisition costs — along with home equity growth in healthy housing markets — with renter costs like security deposits and rent payments. The nationwide breakeven horizon averaged 1.9 years at the end of 2015, according to Zillow.

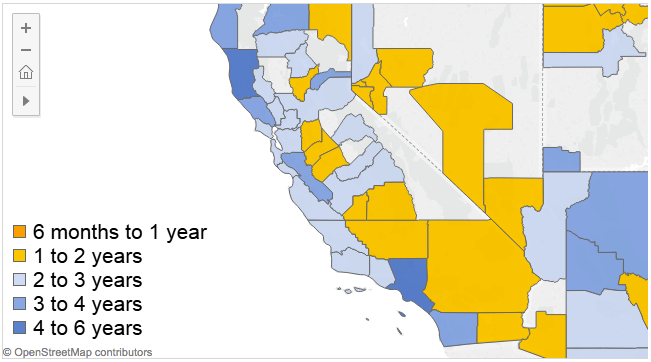

In California, the story is a little different.

Statewide, the average breakeven horizon is about 3.3 years. This is broken down regionally to:

- 4.4 years in Santa Clara;

- 4.1 years in Los Angeles;

- 3.7 years in Santa Barbara

- 3.3 years in San Francisco;

- 3.1 years in San Diego;

- 2.7 years in San Bernardino; and

- 2.0 years in Riverside.

Clearly, how long it takes to breakeven on buying rather than renting depends on where you are in the state. Further, zip codes within these metropolitan areas have varying breakeven horizons, which can be viewed on Zillow’s page.

Areas experiencing the most rapid home price increases tend to have the highest breakeven horizons — and also tend to be located along the coast. Inland places like Riverside and San Bernardino see home purchases pay off the quickest since homes are relatively cheap to begin with.

Image courtesy Zillow.com

Compared to this time last year, the breakeven horizon has come to more of a consensus across the state. In Los Angeles, it has decreased from 5.1 years at the end of 2014 to 4.1 years at the end of 2015 — whereas, in Riverside it has increased from a low 1.5 years at the end of 2014 to 2 years in the most recent report.

Breakeven horizons everywhere will rise significantly once mortgage interest rates increase. With the Federal Reserve’s (the Fed’s) announcement about increasing rates late last year, time is running out for the low mortgage rates experienced today. Interest rates on fixed rate mortgages (FRMs) are expected to increase later in 2016, or perhaps early in 2017. This will result in lower buyer purchasing power across the state.

Further, since more of the homebuyer’s monthly payment will go toward interest and less toward principal, their investment will take longer to accumulate equity. Thus, the breakeven horizon will grow in step with increasing mortgage rates.

The advice for homebuyers and their agents: buy in 2016, before interest rates increase. Not only will the homebuyer be able to gain equity more quickly with a low rate, but they will also qualify for a larger principal amount. Those who wait until after rates increase will have to deal with higher and higher interest rates in the coming years as we enter the next 30-year rate cycle.

{kind=link}