This article analyzes the negative impact of information asymmetries existing between buyers, sellers and their agents in the California real estate market.

Quantity vs. Quality: from boom to crash

In an ideal real estate marketplace, each individual negotiating to buy a home possesses all the relevant information necessary to making the best decision possible. Theoretically, home prices depend on accepted standards of quality (i.e. sound architectural design, valuable land, good neighborhoods) which lead to desirability and thus demand.

In the practical operations of the real estate marketplace, pricing often seems to be determined in the reverse order of operations — demand determines the price, which then sends a misleading signal of the quality of the goods or services they are considering for purchase. This begs the question: where does this demand come from if not a perceived level of quality on behalf of the consumer?

Demand appears to materialize out of nothing — an economic phenomenon that seems to be a gift to sellers, real estate professionals and lenders alike reflected in the inflated prices (and thus brokerage fees) during boom times.

This crude supply and demand approach to pricing, wherein the buyer’s perception of quality is emptied out of the equation and replaced with a false urgency to buy based on purported scarcity, creates a dangerous instability in the real estate marketplace. All this everyone has witnessed during the fallout in real estate ownership after the Millennium Boom.

In the midst of a phenomenal real estate market boom, agents and brokers quickly jettison the notion of quality. Be it the quality of the material goods they sell (read: used homes) or the material facts about those goods they are contracted to communicate to clients before deciding to buy, the boom-time mentality is solely driven by the unsubstantiated urgency generated from scarcity in the housing supply (perceived or actual).

After the inflated prices and sales volume of a market boom fade, real estate professionals are left wondering how to sell without the illusion of false urgency in their vest pocket — in a buyer’s market, the quality of real estate and real estate services become paramount. This is why recessions are productive. They force real estate agents, brokers (and maybe even some lenders) to return to the fundamentals of quality-based pricing for the material goods they sell and the personal services they offer.

Editor’s note — The issue of pricing for real estate services is further complicated by the standard of brokerage fees as a percentage of the price paid for a property. The quality of a real estate agent’s services cannot be determined by the fee they charge and the demand for brokerage services is only reflected in the price of the real estate itself. Thus, in a real estate market boom, the price of an agent’s services increases commensurately with the price of real estate, often while the quality of such services declines. [For more information on the decline in quality of real estate professional services during boom times, see the December 2010 first tuesday article, The rabbit and the greyhound: DRE disciplinary action and broker supervision.]

A new paradigm in real estate markets has emerged from the Great Recession. The traditional lines between a seller’s market and a buyer’s market, from boom to bust, will remain forever blurred if brokers and their agents get it right this time around.

The consciousness of homebuyers has heightened to the point that emotion and peer pressure are no longer the prevailing factors in an agent-induced decision to buy. Especially as Generation Y emerges as the dominant contingent of homebuyers, a generation born and bred on the virtues of information, the success of operators within the new real estate market paradigm will depend on their ability to close the information gap. [For a detailed analysis of the new real estate paradigm, see the May 2010 first tuesday article, Looking through the window towards recovery: a real estate paradigm shift Part I and Part II.]

Information asymmetry: a pernicious residue from the boom

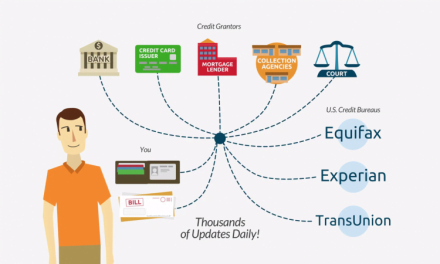

In the always-evolving world of California real estate sales, leasing and lending there exists an information asymmetry facing the buyer (and the buyer’s agent) that deliberately deprives the buyer of facts known to others when weighing their options to purchase property.

The signal example of information asymmetry in the real estate market culminated in the 2008 financial crisis of the mortgage industry. The catalyst for the crash in the housing market was a radical divergence in the information known to mortgage lenders and unknown to homebuyers — if only homebuyers had known, before purchasing a home, what the lenders and investors (and quite possibly their agent) knew.

Although all pertinent formulas, terms and conditions for the performance of a home loan were fully agreed to in the loan agreements, homebuyers were left ignorant of the unwritten financial risks inherent to the loans they negotiated— even when they were represented by a real estate agent to advise and act on their behalf in their purchase, which of course was contingent on obtaining financing.

This information asymmetry led to an omnipresent trend in mortgage defaults the likes and effects of which the California real estate market has never seen. The fact that homebuyers are not trained, much less experienced or educated, in the art of interpreting and applying the legal jargon used in standard loan agreements has become woefully obvious.

Worse yet, homebuyers do not have the time required to surmount the steep learning curve to research and analyze the consequences of taking on a mortgage — a formidable barrier to sufficiently educating themselves so they may make the right choice when financing the purchase of a home. Simply because taking out a mortgage is a “standard” practice for everyone else, this does not suffice as a reason for every homebuyer to go leveraged. The excuse for conduct because it is standard is nearly always an unjustifiable reason for failure to advise on the risks involved — everyone else’s conduct is not relevant information for decision making in real estate transactions. [For more information in trends in notices of default (NODs) and notices of trustee’s sale (NOTs), see the January 2011 first tuesday article, NODs and trustee’s deeds: grim signs of real estate’s present condition.]

Many states will not let a buyer go under contract until an attorney is involved on their behalf. The purpose: to insulate the principals against the agent’s failure to properly advise. However, California brokers and agents have the statutory authority and duty to advise, negotiate and close a sale without any attorney involved in the transaction, as is the case with nearly all home transactions in California.

The risk of losing one’s authority to exclusively represent a buyer or seller to attorneys is raised every time a broker and his agents fail to fully advise on the facts and consequences of a real estate transaction in which they are to receive a fee for providing services. An agent foolishly advising clients they are not an attorney (a patent fact) and then stating they cannot advise on the legal aspects of the transaction they are negotiating (a misrepresentation of their services) will only lead logically to pulling attorneys into home sales. If that is what brokers and agents want, then create the vacuum for more advice and see who powers their way into your deals. [Stay tuned for the upcoming first tuesday article on the misconceptions of real estate agents and the offering of legal advice.]

Information asymmetry in the real estate market does not only apply to the lender/borrower relationship. Rather, it is pervasive throughout all levels of real estate transactions negotiated by real estate agents, particularly in recent boom years. The culture of seller dominance, as maintained by over-confident, if not arrogant, listing agents and fostered by the mischievous Multiple Listing Service (MLS) environment, is founded upon the intentional withholding of information from the buyer until the buyer has reached the point of no return (read: the offer has been accepted). Only after escrow is opened is the buyer given value-related property information, known as untimely disclosure, a breach of the listing and buyer’s agents’ duties owed a prospective buyer.

Agency case decisions such as Jue v. Smiser and the recent and timely Holmes v. Summer presage the urgent replacement of this arrogant approach to real estate transactions. In the new real estate paradigm, only total transparency of adverse property and loan information which might alter a buyer’s purchase and financing decisions and the timely disclosures of such critical data by the seller and his listing agent (and buyer’s agent if he is able to get the information) will be tolerated by the increasingly informed and persnickety group of California homebuyers.

Homebuyers are now sensitized to the need for more information by the prevalence of family, friends and neighbors in destroyed real estate transactions flowing from this financial crisis and recession. They now know what to expect, if not what to ask. [For more details on how these recent case decisions have affected California’s real estate landscape, see the November 2010 first tuesday article, Holmes v. Summer: Dilatory disclosures and the damage done.]

A market for lemons: real estate licensee conduct in the new paradigm

Information asymmetries between all participants in real estate transactions pose the last remaining barrier to the creation of a sustainably functioning real estate market.

The squaring of information asymmetries in real estate transactions has long been a legal imperative for real estate agents and brokers. This, after all, is why a license for dealing in real estate exists. The license is a signifier, a material representation of a professional’s education and commitment to share the information they have and that they can readily gather with their buyer, then advise on the consequences of actions their buyer decides to take. This is all part of the employment that the buyer’s agent undertakes by expecting a fee on closing.

In the new real estate paradigm, the balancing of information asymmetries has become necessary to maintaining fair market prices and thus protecting the consistent flow of fees to real estate agents and brokers from year to year, not just boom time frenzy and bust year insolvency. The deleterious effect of agents maintaining information asymmetries in the real estate market is the risk that homebuyers will perceive all real estate professionals as bad actors — hucksters to be wary of and undeserving of their trust.

In George Akerlof’s Nobel Prize winning piece, “The market for lemons: quality uncertainty and the market mechanism,” he describes a marketplace where even commodities of genuine quality lose their value as a direct result of information asymmetries.

Akerlof presents the used car market as his example. The notion that a used car could possibly be a lemon pervades amongst prospective buyers in the marketplace since used car salesmen became notorious for withholding information from their buyers in order to close a deal. Thus, the used car market came to be perceived as a market for lemons, where simply by virtue of the fact a car is “used” its value plummets even though it may be only a few years old with minimal miles.

Editor’s note — In a successful effort to mitigate the damaging effects of their unsavory reputation on the used car market, used car dealers learned to have their goods certified by third parties and provide buyers with a full history of each car’s repairs, accidents and so on. “Used” real estate dealers (MLS brokers and agents) have yet to develop such a solution for inspiring greater consumer confidence in the real estate market.

Due to the negative image of real estate professionals and mortgage lenders that is still growing rapidly as more fraud is uncovered every day, the real estate market is dangerously close to becoming a market for lemons. As the consequences of bad actors in the real estate industry continue to cause homebuyers to suffer, the value of even the most ethical, responsible and thorough real estate agent’s services will diminish – as will the demand for homeownership.

What can real estate agents and brokers do to turn this tide of ill will to all those involved in the real estate industry and thus protect the legitimacy of their fee? They must first devote their best efforts to education and the process of property investigation. Gone are the days of churn and burn real estate sales, where every fee was only a signature away. Once the proper education about the management of a real estate transaction is acquired, the culling and sharing of both specific property conditions and general market conditions with a client in counseling sessions will be vital to every successful agent.

{kind=link}

Information – this is why I blog. Buyers and sellers need greater access to more info. In the process of sharing info with people, I have found it to help me as well.