It’s not surprising really. The zeitgeist in the U.S. right now is one of economic malaise and negative consumer sentiment, according to an NBC News/Wall Street Journal Poll.

The poll found that 57% of American adults still consider the U.S. economy to be in recession. This is despite the fact that the last recession, known as the “Great Recession”, technically ended in June of 2009.

The technical indicator of recession is two consecutive quarters of falling gross domestic product (GDP). Once GDP increases, presto: the recession is over. But people don’t live their lives by textbook definitions. Instead, they judge the health and wealth of the economy based on their standard of living.

While GDP is technically growing and 2013 was a banner year for the stock market (some say a bubble year), the lion’s share of these gains are not going to the majority of Americans. 95% of income gains from 2009 to 2012 (four post-recession years) went to the top 1% of income earners, according to Berkeley economist Emanuel Saez.

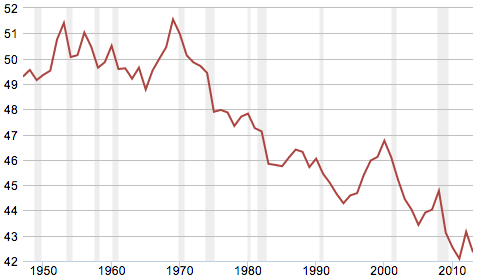

A most disconcerting long-term trend, wage gains have not kept up with economic growth for the past four decades. Wages were at their highest level relative to GDP in the late 1960s, peaking at 51% of the total economy. They fell to 45% by the beginning of the Great Recession, and have continued to fall throughout the recovery, to just 42% of GDP.

Check out this chart of veritable wage destruction:

Chart courtesy of the Federal Reserve Bank of St. Louis

The real heartbreaker here is that the trend continues and nothing is being done to turn the tide. As we’ve harped on time and again, there are really two viable options: allowing for more inflation before the Fed even thinks about tapering stimulus (the monetary policy approach) and/or aggressive social engineering, à la the New Deal. This includes reforming the regressive tax regime built into U.S. and California housing policy.

It’s no coincidence that home sales volume continues to fall in the face of wage erosion. The reason California real estate hasn’t felt more of a blow from wage erosion is because its effects were masked first by the sub-prime credit bubble, then by the speculator mini-bubble. Well, both of these illusory economic phenomena are definitively over now and consciousness of the actual state of the real estate market is rising. Is it time to finally address the imbalance, or do we just cross our fingers and hope for another bubble to delay the inevitable a few more years?

{kind=link}