A listing agent’s perverse custom

As Department of Real Estate (DRE) licensees, real estate brokers and agents are governed by agency law in their conduct with members of the public. They follow a very specific code of conduct in order to fulfill both their general duty owed to the public they interface with while acting as licensees, as well as their specific duty owed to their clients. However, a culture exists in the real estate industry out of which has evolved a curious set of customs that often supersede and run counter to the rule of law.

For example, an arrogance of seller dominance has imbued the culture of real estate brokers and agents with a particularly noxious custom: the deliberately dilatory disclosure. The seller is all-too-often erroneously considered the power-player in real estate transactions — a perversion of the old “win-win” attitude reshaped as the “win-lose” attitude prevailing today.

Consequently, the lowly buyer and his agent struggle to acquire information about a property that is, at a minimum, necessary for the buyer to make an informed decision. All the while, the seller and his listing agent remain perched upon the industry’s high horse of seller dominance, stoically withholding information until an offer is accepted. Only after the emotional process of negotiating a purchase is complete, with the buyer finally under contract, is the critical information handed over to the buyer who is now past the point of no return. [For more information on seller dominance, see the October 2010 first tuesday article, The demographics forging California’s real estate market: a study of forthcoming trends and opportunities.]

The laissez-faire culture of seller dominance is perpetuated by customs that have supplanted the rule of agency law — so much so that they are integrated into widely-used trade union forms and pronounced as “standard operating procedure” by selling agents, listing agents and sellers alike. These insidious customs critically compromise the buyer’s ability to rely on real estate professionals as the gatekeepers to the American dream.

Holmes v. Summer is a precise example of how the culture of seller dominance and the attendant and deliberate dilatory disclosures have gone awry, rendering the previously acceptable “standard operating procedure” virtually criminal. Certainly the willful withholding of facts, which are necessary for the buyer to determine a fair price and that the property is suitable to be purchased, is reprehensible conduct deserving of suspension or revocation of a license for dishonest conduct.

Holmes v. Summer provides a watershed moment in case law for brokers and their listing agents. Holmes reestablishes proper conduct for listing agents and their brokers regarding the timing of property disclosures (specifically title condition disclosures in the Holmes case). Holmes mandates that all disclosures of material fact about the property, known to either the seller or the listing agent, which might influence any of the buyer’s decisions about purchasing the property must be made to the buyer by the listing agent prior to acceptance of an offer, not after an offer is accepted and escrow is opened, as has become the generally accepted custom amongst brokers and agents today.

Listing agents are on notice: you must now Holmes-proof yourself and your seller in order to mitigate exposure to liability – up front risk reduction – and ensure that you are fully performing both your specific duty to your client as well as your general duty to the buyer.

Buyer’s selling agents beware: the listing agent’s custom is deeply ingrained and you will need to insist on full disclosure prior to preparing and submitting an offer. Market conditions with a dearth of buyers, such as we are currently experiencing, demand selling agents be more vigilant in securing the proper disclosures for their buyer. [For more information on the Holmes v. Summer case, see the November 2010 first tuesday Recent Case Decision.]

The precedence of disclosure: Holmes v. Summer and the listing agent’s duty

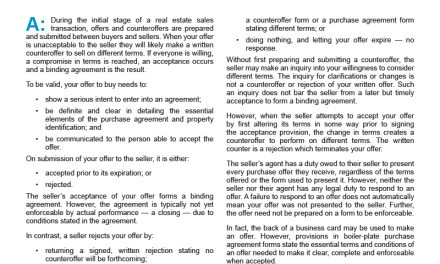

Consider a buyer’s selling agent who represents a prospective buyer of a one-to-four unit single family residence (SFR). The selling agent makes an inquiry on behalf of the buyer into a home he locates on a multiple listing service (MLS). The seller’s listing agent responds by advising the property is still for sale as listed.

The selling agent and the prospective buyer inspect the property and determine that it meets all of the buyer’s needs. The selling agent requests a property marketing package from the listing agent in order for the buyer to make an informed decision about price and terms, or that he even wishes to buy the property, before preparing an offer. The listing agent refuses to provide the selling agent with a marketing package detailing the listing agent’s diligent inspection and investigation into the property he is marketing. The selling agent is informed all disclosures will be made according to standard operating procedure, as provided in the trade union purchase agreement, after an offer is accepted and escrow is opened.

Frustrated but deferring to the listing agent’s operating procedure, the selling agent prepares and submits an offer on behalf of the prospective buyer. The seller rejects the offer as unacceptable and the listing agent prepares a counteroffer on behalf of the seller, bargaining for a better price while making no disclosures about facts which may adversely affect the buyer. The listing agent does not disclose any conditions affecting the property, including his knowledge of liens encumbering title which may interfere with the seller’s ability to deliver title at the offered price.

The counteroffer provides a second opportunity for the listing agent to disclose the existing liens, which he again fails to do. In addition to his failure to perform his general duty owed to the buyer in providing a complete marketing package to the selling agent, the listing agent likewise fails to protect his seller from liability resulting from the undisclosed liens on the property by including a short sale contingency addendum with the counteroffer.

The buyer accepts the counteroffer, which was structured as a cash-to-new-loan sales transaction, and escrow is opened. In reliance upon his right to acquire the seller’s home and unaware of recorded facts about the property’s condition that might interfere with his expectations for purchasing the property, the buyer closes escrow on the sale of his primary residence. He incurs expenses related to his preparation for taking ownership and possession of the seller’s home.

Information about the clouded condition of the property’s title, known to the listing agent prior to the seller’s contracting with the buyer, is discovered by the buyer in a preliminary title report (prelim), obtained and handed to his selling agent by escrow. It details lien amounts on the property in excess of the negotiated price set in the purchase agreement. The seller is unable to perform his obligations to deliver title and close escrow since the seller’s lenders will not accept his net sales proceeds for reconveyance of the trust deeds.

Due to the seller’s insolvency, the buyer is unable to force the seller to perform and deliver title, which would require the seller to pay the shortage. Thus the buyer exercises his right to cancel due to the seller’s material breach of the purchase agreement. On cancellation, the buyer suffers losses due to the seller’s inability to convey title free and clear of all encumbrances.

The buyer then makes a demand on the listing agent to recover the money losses he incurred after selling his home based on expectations set by the listing agent’s conduct when the purchase agreement was entered into that the seller would be able to perform — nothing to the contrary was disclosed.

The buyer claims the listing agent is liable for his losses since he had a duty to disclose all property conditions that might have an adverse effect on the buyer, including the existence of liens encumbering the property for amounts in excess of the contract price – and do so prior to acceptance of an offer.

The listing agent claims he is not required to disclose the seller’s clouded title condition as encumbered with mortgage liens prior to the acceptance of an offer since to do so would require him to breach his fiduciary duty owed exclusively to the seller by revealing confidential financial information — a violation of his trade union’s code of ethics. [For more information on the rules governing client confidentiality, see the January 2009 first tuesday article, Confidentiality of information: by agency or by agreement.]

Is the seller’s listing agent liable for the buyer’s losses if he fails to disclose, prior to acceptance of an offer, that the title is encumbered by liens in excess of the contract price, rendering the seller possibly unable to deliver title as agreed?

The listing agent in this case fails to perform his general duty owed to the buyer to disclose his knowledge of material facts, information that might possibly affect the buyer’s decisions regarding an offer. It is the listing agent who sets the buyer’s expectations for the desirability of the property and the ability of the seller to deliver the property in the condition as disclosed prior to the moment an offer is accepted. These expectations are set by both the information the listing agent does and does not provide. In other words, the absence of information about adverse conditions, either known or readily available to the listing agent, is as powerful in forming the buyer’s expectations of a property as an explicit and timely disclosure. The buyer must be put on notice of adverse property conditions and the notice is to take place before acceptance.

In Holmes v. Summer, the listing agent has knowledge of property facts concerning the seller’s inability to convey title to the property free and clear of encumbering liens. Rather than informing the buyer’s selling agent of this very material fact prior to the acceptance of an offer, the listing agent takes refuge in the deceptively conceived cloisters of his custom: withhold material facts until the buyer is under contract in order to accomplish the seller’s objective of selling the property (read: collect a broker fee).

Happened with my last transaction…also the listing agent insisted that I had to use CAR forms. The items that were not disclosed by the listing agent wound up being paid for by the listing agent, as the buyer and myself refused to pay for them. Seller was out of state.

Great article. Reading this allows me to be a little better at my craft as a real estate consultant, especially since I have always suscribed highly to my duty as a DRE fiduciary.

What a timely article!

I am having exactly similar experience from seller and his agent on a transaction now in escrow.

I hope I don’t end up in court…….

The buyer went directly to the listing broker – this was a dual agency deal. Which makes it doubly damning that she failed to disclose the short sale situation until after the buyers had sold their home. She was just chasing the dollar signs, looking to double end a $750K transaction, and willing to act totally without scruple to make it happen.

This isn’t anything new … this is why we have the short sale listing and sales addendums. In reality, the buyer’s agent also screwed up for not added the sales addendum to their offer.

Hey, Steve, When CAR decides to follow the Real Estate laws of disclosure which are required of any material fact which may affect price and the agents and sellers abide by the law, closings will go smoothly. The buyers’ advisor is meaningless when the agent’s DRE license is a fiduciary. They cannot waive their representation. My feeling is agents need to know the law.

As far as lenders go, I agree and it a dream world, lenders should have to answer to the buyer before the offer is made. See if we can get a law passed. In the meantime, on the CAR agreement , it needs to be stated all conditions to fund are in the hands of the lender and cannot be removed as a contingency. This is a way to protect the buyer.

I appreciate this article, and the one that preceded it. However, we do have “CAR” forms that delineate the potential for additional liens (short sale addendum, disclosures in the MLS, etc.), and at least alert the buyer and his agent to the possibility for lien issues. I agree with the spirit of the article, though, and a GOOD property profile (includes open deeds, etc.) should provide the necessary title information; I can’t think why the seller’s agent argued that this data was confidential, since it’s all public record, and clearly understandable from the recording data. What MIGHT not be public record is delinquency that’s not yet resulted in the filing of an NOD, and that certainly needs legal clarification, because it IS confidential information. I recently suggested to one of the agents in our office that we prepare a standard “authorization form” to cover the legalities of communicating things like credit status, so that the buyer and his agent may know the full circumstances of property they are attempting to purchase. I intend to make that suggestion office-wide in our next office meeting.

A larger problem is the fact that lenders (not a party to the transaction) can “pull the plug” in underwriting after everything is “done” on the seller’s and buyer’s side. They often do this, for reasons that are easily discoverable up front, yet the courts have never really taken them to task for this behavior. I believe that the lender ought to have an independent duty to discover information up front, ON ITS OWN (without effort from agents on either side), and underwrite the loan in advance. The lender, after all, makes its decision at the last minute, and the issue of loans being approved and then later “disapproved” looms quite large at the present moment.

Just my opinion.

Steve Bradley

My cousin recommended this blog and she was totally right keep up the fantastic work!