This form is used by a prospective junior lender or carryback seller when the real estate is encumbered by an existing first mortgage containing a due-on clause, to obtain consent from the lender holding the mortgage to further encumber the property with a second mortgage.

The due-on waiver

A typical carryback sales transaction involving an existing mortgage is structured as either:

- a regular second mortgage carried back by the seller when the existing mortgage holder consents to the conveyance of an interest in the property and the recording of a carryback second mortgage by waiving the lender’s due-on clause in exchange for an assumption fee and modification of the note by the buyer, called a formal assumption; or

- an all-inclusive trust deed (AITD) and note, or another wraparound security device such as a land sales contract, with the underlying mortgage holder consenting to the conveyance to the buyer and the carryback AITD by waiving their due-on clause in exchange for a modification of the note and payment of fees by the seller — all in lieu of the buyer’s assumption of the mortgage, an activity labeled a reverse assumption.

After the mortgage holder consents to the carryback sale and escrow closes, future events beyond the carryback seller’s control can again trigger the due-on clause.

Without the mortgage holder’s prior written waiver of their due-on enforcement rights triggered by future transfers after closing a carryback sale transaction, the mortgage holder can call their mortgage due on a later transfer of the buyer’s interest in the property.

With some exceptions for a principal residence, a transfer subject to due-on enforcement rights include a:

- resale;

- further encumbrance;

- lease for a term greater than three years;

- court ordered transfer;

- foreclosure; or

- death.

A written waiver of the mortgage holder’s future enforcement of the due-on clause bars the mortgage holder from calling the mortgage due so long as the carryback mortgage remains without a reconveyance. Thus, the waiver protects the carryback seller as long as the seller has any interest in the property.

The waiver agreement assures the carryback seller they can protect their security interest in the property without interference from the underlying mortgage holder, which will otherwise take place when FRM rates trend higher. [See RPI Form 410]

To best protect the seller’s security interest created by the carryback trust deed, the seller needs to have the mortgage holder waive their right to call the mortgage:

- on the conveyance and further encumbrance of the property on the close of the carryback sale;

- for as long a period as the carryback mortgage remains of record; and

- on the carryback seller’s reacquisition of title to the property when the seller completes a foreclosure on the property or accepts a deed-in-lieu of foreclosure.

To be enforceable against the mortgage holder, the waiver agreement needs to be in writing as do any other commitments or promises made by a lender. [12 Code of Federal Regulations §591.5(b)(4)]

Analyzing the Further Encumbrance Consent

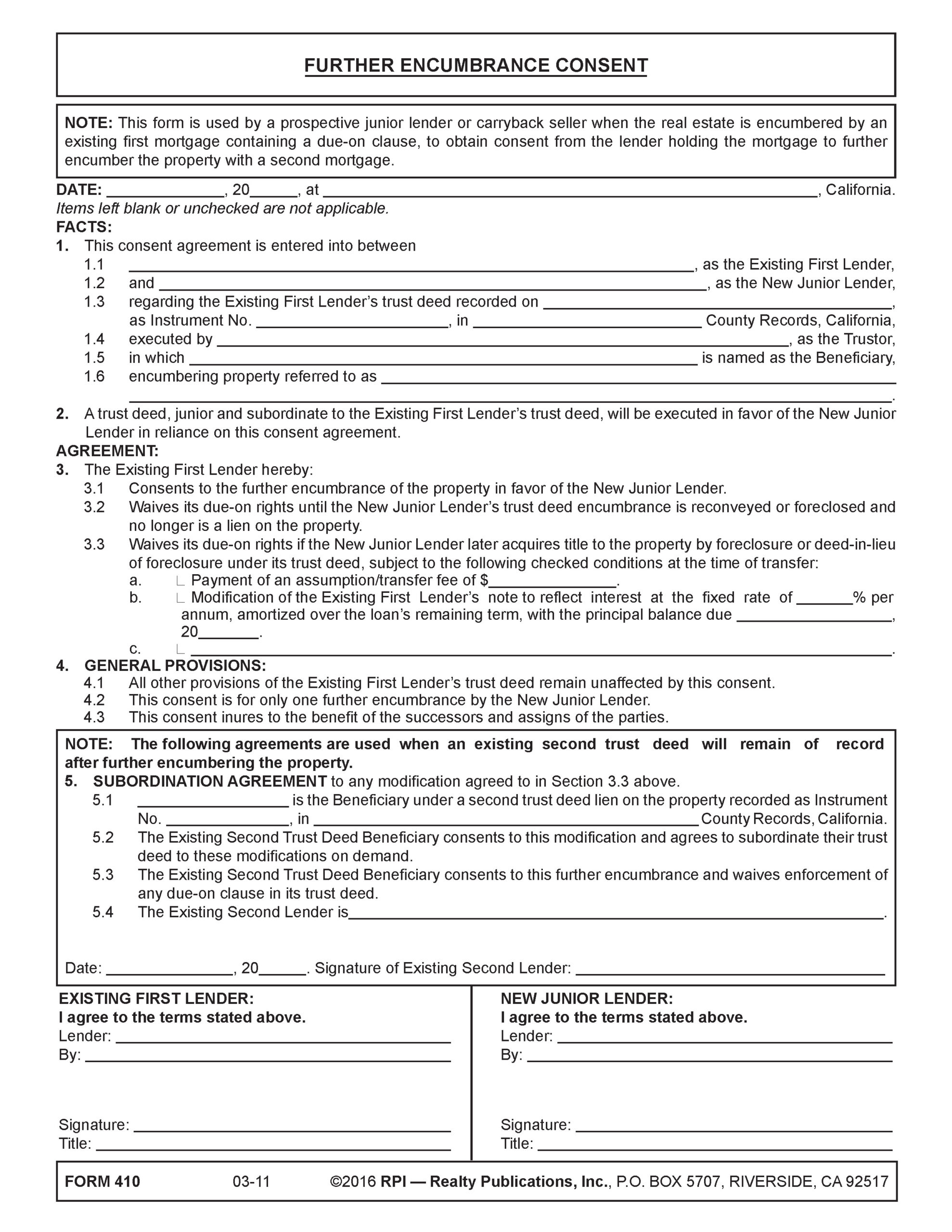

A prospective junior lender or carryback seller uses the Further Encumbrance Consent published by RPI when the real estate is encumbered by an existing first mortgage containing a due-on clause. The form allows the junior lender or carryback seller to obtain consent from the lender holding the mortgage to further encumber the property with a second mortgage. [See RPI Form 410]

The Further Encumbrance Consent includes:

- facts covering the identity of the existing first lender, the new junior lender, the lender’s trust deed and its trustor, beneficiary and property address [See RPI Form 410 §1];

- the existing first lender’s consent in the agreement to the further encumbrance of the property in favor of the new junior lender, waiving the lender’s due-on rights in exchange of their exaction of a negotiated assumption fee [See RPI Form 410 §3.1-3.2];

- general provisions stating the existing first lender’s provisions remain unaffected, that the consent is for only the one identified further encumbrance by the junior lender and that successors and assigns of the parties are controlled by the consent [See RPI Form 410 §4];

- subordinating language [See RPI Form 410 §5]; and

- signatures of the existing first lender and new junior lender. [See RPI Form 410]

Editor’s note – Expect stonewalling by the lender when negotiating a waiver agreement, as it is in to their financial benefit to stall when others are eager to close a deal. Some mortgage holders may simply call when the owner has entered into an agreement to sell or grant an option to buy since the buyer then has an equitable ownership interest in the property.

Form navigation page published 12-2023. Updated 01-2026.

Form last revised 2016.

Form-of-the-Week: Form-of-the-Week: Further Encumbrance Consent, and Note Enforcement Provisions — Forms 410 and 418-5

Form-of-the-Week: Guarantee Agreement for Rental or Lease — Form 553-1

Article: Special provisions in a note

Client Q&A: What is a “due-on clause”?

Further encumbrance notes always feel like there’s more depth and detail behind the system than you first expect.

thanks for sharing!!