Conflict of Interest Disclosure – bias to be declared in writing

A conflict of interest arises when a broker or their agent, acting on behalf of a client, has a competing professional or personal bias which hinders their ability to unreservedly fulfill fiduciary duties on behalf of their client.

In a professional relationship, a broker’s financial objective of compensation for services rendered is not a conflict of interest. However, fees and benefits derived from professional courtesies, familial favors, and preferential treatment by others is compensation a broker needs to disclose to their client. [See RPI Form 119]

A conflict of interest addresses the broker’s personal situations which are potentially at odds with the agency duty of care and protection owed to the client. This creates a fundamental agency dilemma for brokers. Thus, a conflict of interest is not a compensation or business referral issue.

A conflict of interest disclosure creates transparency in the transaction. It reveals to the client the possible bias held by the broker which, when disclosed, allows the client to take the bias into consideration in negotiations. The disclosure and consent do not neutralize any inherent bias. However, it does neutralize the element of deceit which breaches the broker’s fiduciary duty when left undisclosed.

A conflict of interest exists when:

- a broker has a positive or negative bias toward the opposing party in a transaction or a person not directly involved in the client’s transaction; and

- that bias in favor of or against the other person might compromise the broker’s ability to freely recommend an action or provide guidance to their client.

Related video:

Analyzing a Conflict of Interest

Unless disclosed and the client consents, the conflict is a breach of the broker’s fiduciary duty of good faith, fair dealing and trust owed to their client when the broker continues to act on the client’s behalf. [See RPI Form 527]

Potential situations from which a conflict of interest may arise include:

- the broker or their agent holds a direct or indirect ownership interest in the real estate involved in the transaction;

- the broker or their agent is directly or indirectly a buyer of the property in the transaction, including a partial ownership interest in a limited liability company (LLC) or other entity which owns or is buying, leasing or lending on the property [Whitehead Gordon (1969) 2 CA3d 659];

- an individual related to the broker or one of their agents by blood or marriage holds a direct or indirect ownership interest in the property or is the buyer [Sierra Pacific Industries Carter (1980) 104 CA3d 579];

- an individual with whom the broker or a family member has a special pre-existing relationship — such as prior employment, significant past or present business dealings or deep-rooted social ties — holds a direct or indirect ownership, leasehold or security interest in the property or is the buyer;

- the broker’s or their agent’s concurrent representation of the opposing party, referred to as a dual agency situation; or

- the unwillingness of the broker or their agent to work with the opposing party, or others, or their brokers or agents in a transaction.

Ultimately, a conflict of interest needs to be disclosed to the client when the broker has a pre-existing relationship with a person other than the client which might hinder their ability to fully represent the needs of their client. Notice that the potentiality itself creates a conflict – even if in practice the agent’s duties are not compromised.

This pre-existing relationship may be based on any form of:

- kinship;

- employment;

- partnership;

- common membership;

- religious affiliation;

- civic ties; or

- any other socio-economic context.

A broker or their agent uses the Conflict of Interest form published by RPI (Realty Publications, Inc.) when representing a buyer or seller to disclose the potential conflict of interest which may interfere with their ability to represent their client as agreed. [See RPI Form 527]

This disclosure is serious business. The client’s tardy discovery of the conflict and their complaint to the Department of Real Estate (DRE) for failure to make the disclosure and obtain consent before continuing to advise or act on behalf of the client are grounds for the DRE’s suspension or revocation of the broker’s license. [Calif. Business and Professions Code §10177(o)]

Dual Agency – a conflict of interest between opposing parties

A dual agent is a broker who simultaneously represents the best interest of opposing parties in a transaction, e.g., both the buyer and seller. This encompasses both the broker and the agents they employ.

The dual agency alone creates a conflict of interest, which needs to be promptly disclosed to each client.

A dual agency relationship may exist in any brokered transaction, such as a:

- sale;

- rental or leasing transaction; or

- mortgage origination or assignment.

In sales transactions, the conflict of interest in a dual agency typically evolves when the buyer:

- is an existing client as they have received information from the broker or their agents on qualifying properties listed by other brokers; and

- is now exposed to or express interest in property listed by the broker.

Dual agency has always been proper brokerage practice. It is a situation that arises naturally in the course of representing buyers and sellers. However, the existence of a dual agency is to be promptly disclosed to each client. [CC §2079.17]

Related video:

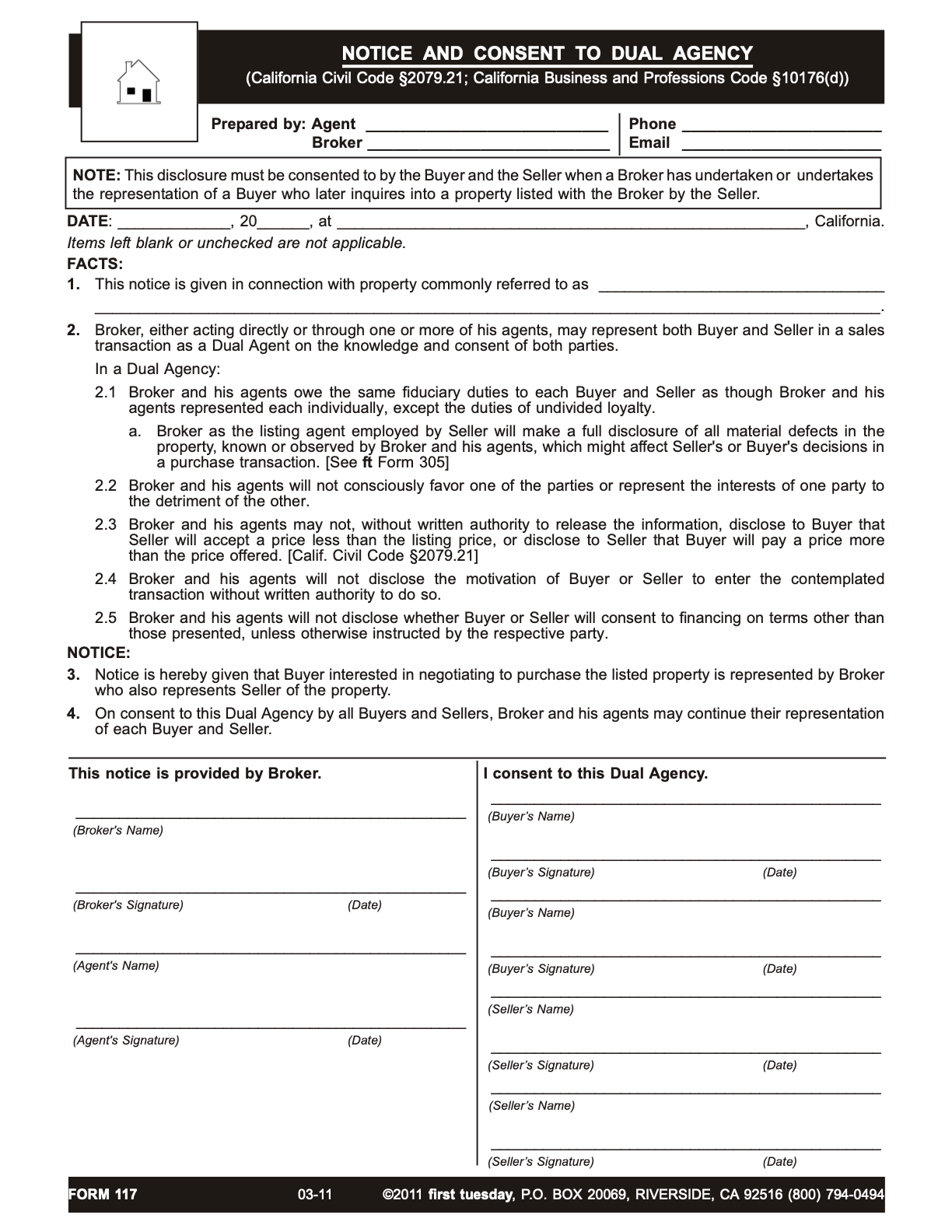

With RPI’s Notice and Consent to Dual Agency form, a broker may disclose their dual agency relationship to both the buyer and seller and obtain written consent from each of them to continue services. [See RPI Form 117]

The contents of the Notice and Consent to Dual Agency form includes:

- the address of the property [See RPI Form 117 §1];

- information regarding the broker’s responsibility in the dual agency [See RPI Form 117 §2];

- a notice which contains a declaration that the buyer negotiating to purchase the listed property is represented by the broker who also represents the seller [See RPI Form 117 §3]; and

- a notice which states the broker and their agent may continue to represent both the buyer and seller. [See RPI Form 117 §4]

Each participant then signs the form, including the buyer, the seller, the broker and the broker’s agent. [See RPI Form 117]

A broker who fails to promptly disclose their dual agency at the moment it arises is subject to:

- the loss of the brokerage fee;

- liability for their principals’ money losses; and

- disciplinary action by the DRE. [BPC §10176(d)]

This article was originally published November 2013 and has been updated.

{kind=link}

Dear Patricia,

A real estate broker and their agents may earn a fee for providing both real estate services and loan services on the same transaction, so long as they are actually providing both services, not just referring them. However, in both these cases, the fees must be disclosed to the client.

In addition, a referral fee can only be earned if no service is being rendered by the referring broker on that transaction. Thus, a business or brokerage involved in the closing of a home sale or refinance is prohibited from paying brokers and their agents a fee of any type for a referral when the broker is already receiving a fee on the broker services they render on behalf of the client, unless the broker performs significant services on behalf of the third-party provider in the delivery of their service. Thus, a second fee cannot be paid to the broker, much less their agent, by anyone if it is received by the agent for activity limited merely to referring the client to the third party provider.

Obtaining a broker’s license is the ultimate step in any agent’s career. If you perform sales and mortgage activities under another broker, it does not create any additional liability for you. If you conduct activities as an independent broker or form your own brokerage, it is then that you take on the liability for your activities, however, with no restrictions limiting your ability to do both the sale and the mortgage.

See related articles:

first tuesday case in point: RESPA “no-new-service, no-second-fee” rule applies only to fee splitting

Brokerage Reminder: Kickbacks can run but they can’t hide

Is it correct, now that I have an NMLS No. I can get paid for introducing clients to reverse mortgage Brokers?

BUT does having a Loan Officer license means I cannot do real estate?

Is it within the law, to sell a property as a Realtor/Broker and ALSO find the mortgage money for the Buyer?

I have my real estate license for approximately 15 years in good standing and am considering taking the Broker licensing exams, as I do have a partial Law Degree, and a BA in Business Science, is that a good idea?

Look forwards to your response Thank you for your time, Patricia