So, you want to originate consumer mortgages? Read on for an explanation of the different MLO licensing schemes available in California, and the steps you take to obtain and maintain your MLO license or endorsement.

California BRE or DBO license

In the aftermath of the 2007 mortgage meltdown and financial crisis, Congress passed the Secure and Fair Enforcement for Mortgage Licensing Act of 2008 (SAFE Act). The SAFE Act requires any person who, in anticipation of consideration, accepts a consumer mortgage application or arranges a consumer mortgage secured by a one-to-four unit residential property to:

- register with the public database of mortgage loan originators, the Nationwide Mortgage Licensing System (NMLS); and/or

- obtain a state-issued mortgage loan originator (MLO) license or endorsement. [12 Code of Federal Regulations §§1008 et seq.; Calif. Business and Professions Code §10166.01(b)(1); Calif. Financial Code §§22100, 50002]

Editor’s note — A consumer mortgage is a consumer loan that funds a primarily personal, family or household use and is secured by an interest in a one-to-four unit dwelling, owner-occupied or not. Dwellings include individual condominium units, cooperative units, mobile homes and trailers if they are used as a residence. [Bus & PC §10166.01(d); Fin C §§22012(e), 50003(p)]

In contrast to consumer mortgage activity, the making or arranging of business, investment and agri-business purpose mortgages secured by any type of real estate, or consumer loans secured by a mortgage on other than one-to-four unit residential property are controlled by different licensing rules under the California Bureau of Real Estate (CalBRE) and California Department of Business Oversight (DBO).

The registration and licensing details are recorded in the NMLS database. The NMLS not only holds the information about each MLO in the U.S., but it also administers the federal registration and state licensing processes. [12 United States Code §5102(6)]

The SAFE Act established two classes of MLOs:

- registered MLOs, who are individuals employed by federally chartered banks, credit unions or other federally regulated financial companies; and

- state-licensed MLOs, who are individuals registered with the NMLS and regulated by state agencies. [12 United States Code §5103(a)]

In California, two state agencies regulate MLOs:

- the CalBRE, which issues MLO endorsements to real estate licensees [Bus & P C §10166.02(b)]; and

- the DBO, which issues MLO licenses under the California Finance Lenders Law (CFLL) and the California Residential Mortgage Lending Act (CRMLA). [Fin C §§22100(a), 50120]

MLOs may obtain authorization to originate residential mortgages under one, two or all three of these schemes. Why choose one scheme over the other? It depends on many factors, including the related activities you want to engage in and whether you are employed or self-employed.

NMLS requirements for all MLOs

All persons seeking to become an MLO (or, if an MLO company, the responsible individuals designated by each scheme) need to submit an application to the NMLS which includes:

- personal residential and employment history;

- fingerprints for a criminal background check;

- an authorization for the NMLS to obtain a credit report; and

- an authorization for the NMLS to obtain information about administrative, civil and criminal proceedings against the licensee. [12 CFR §1026.36(f)(3)(i); Bus & P C §10166.04(a); Fin C §§22105.1, 50121]

At a minimum, individual MLOs and responsible individuals for MLO companies need to show they have:

- demonstrated financial responsibility and fitness to operate honestly, fairly and efficiently; and

- not been convicted of, pled guilty or pled no contest to a felony in a domestic, foreign or military court:

- for registered MLOs, CalBRE MLOs and individual DBO MLOs, during the seven-year period preceding the date of the application or at any time, if the felony involved fraud, dishonesty, a breach of trust or money laundering [12 CFR §1026.36(f)(3)(ii); Bus & P C §10166.05; Fin C §§22109.1(a)(2), 50141(a)(2)]; and

- for DBO MLO companies, during the ten-year period preceding the date of the application. [Fin C §§22109(a)(2), 50126(a)(2)]

In addition to NMLS minimum MLO honesty requirements, the CalBRE and DBO each set their own requirements for MLO qualification.

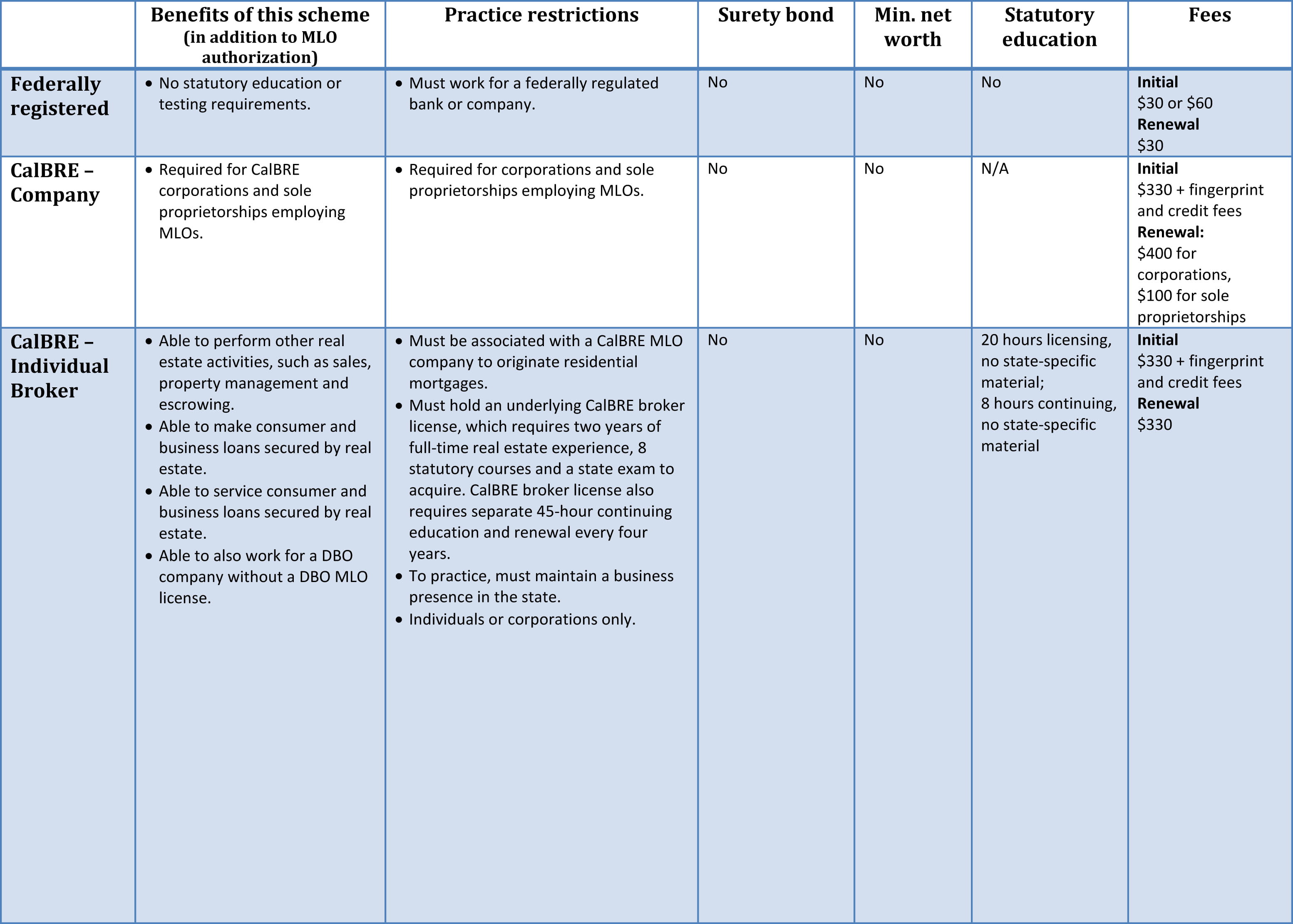

The tables below summarize some of the requirements for each type of license/endorsement. Click on the images to expand each page of the table, or download the PDF file here.

A more in-depth discussion of each license/endorsement type follows.

Under the federally-registered MLO scheme

Practice

If you originate residential mortgages as an employee of a federally regulated bank or credit union, such as Wells Fargo of Bank of America, you are required to register as a federally registered MLO.

Obtain

The first step is to get a job at a federally regulated banking institution working in a residential mortgage position.

If you don’t already have an NMLS ID, the banking institution will create an NMLS account for you in the NMLS federal registry. You’ll then need to fill out an application and submit to credit and background checks. [See NMLS Application Form MU4R]

Fees are involved, and depending on how your new employer works, they may require you to pay the fees, or foot the bill themselves. The initial set-up fee for an MU4R filing is $30 if registration occurs between January and June, and $60 if registration occurs between July and December.

Maintain

As an employee who is a federally registered MLO, you will renew your registration each year during an annual two-month window period of November and December. Your employer, as a federally regulated banking institution, is required to have policies and procedures in place to ensure you keep your registration, and the information contained in your NMLS record, current. [12 CFR §1007.104]

Prior to the renewal, your employing bank will give you a request to renew reminder. This requires you to confirm and attest the information in your NMLS registration is current. The renewal fee for a federally registered MLO is $30.

Under the CalBRE

Practice

Being an MLO who is state-licensed under the CalBRE endorsement scheme allows a broker or your employing broker to collect compensation for arranging residential mortgages secured by real estate. The activities you may perform under this CalBRE license / MLO endorsement combination include:

- mortgage brokerage;

- mortgage servicing;

- the negotiation of mortgage modifications; and

- short sale negotiations. [Bus & P C §10131(d)]

Editor’s note — The endorsement is only triggered by a mortgage modification if you’re paid for the negotiations specifically, rather than completing negotiations simply as the seller’s agent.

If you’re a CalBRE broker with an MLO endorsement or a CalBRE sales agent under a broker with an MLO endorsement, you’re able to broker residential mortgages to:

- CalBRE lenders;

- CFLL lenders;

- CRMLA lenders; and

- state and federally chartered institutions.

In addition to these MLO-specific activities, the CalBRE licensing scheme authorizes you to enter into purchase and listing agreements, and engage in property management, escrow and other activities which require a CalBRE license. [Bus & PC §§10000 et seq.]

Obtain a CalBRE license

Commensurate with the wide range of activities a CalBRE licensee may perform come relatively rigorous licensing and MLO endorsement requirements.

Before seeking an MLO endorsement from the CalBRE you need to hold a valid CalBRE real estate license. CalBRE issues licenses to individuals and corporations only. [Bus & P C §10130]

The CalBRE license comes in two forms:

- the real estate salesperson license, also called a sales agent license; or

- the real estate broker license. [Bus & P C §10131]

To obtain a CalBRE sales agent license, you need to:

- be at least 18;

- complete three college-level licensing courses;

- submit fingerprints for a background check;

- prove legal presence; and

- pass a state examination. [Bus & P C §10153.4]

Fees for obtaining a sales agent license include:

- course fees payable to an approved course provider;

- a $60 examination fee;

- a $49 fingerprinting fee plus a fingerprint rolling fee of $20-$40; and

- a $245 license fee.

Once issued, the sales agent license is good for four years.

A CalBRE sales agent is only able to perform activities requiring a license when employed by a CalBRE broker. [Bus & P C §10132]

For an individual to obtain a CalBRE broker license, you need to:

- be at least 18;

- have at least two years’ full-time experience as a real estate sales agent (or equivalent experience) OR a bachelor’s degree with a major or minor in real estate;

- complete eight college-level licensing courses (less any courses taken when qualifying as a sales agent);

- prove legal presence;

- provide a place of business in the state; and

- pass a state examination. [Bus & P C §10153.2]

Fees for obtaining a broker license include:

- course fees payable to an approved course provider;

- a $95 examination fee;

- a $49 fingerprinting fee plus a fingerprint rolling fee of $20-$40; and

- a $300 license fee.

The broker license is good for four years.

Obtain a CalBRE MLO endorsement

Several CalBRE MLO endorsements exist, depending on your licensing status:

- individual salesperson endorsement;

- individual broker endorsement;

- company (sole proprietorship) broker endorsement;

- corporate broker endorsement; and

- branch office endorsement.

Company and branch endorsements require the designation of a qualifying individual or branch manager who is a broker with an individual broker endorsement. Thus, the core endorsements are the individual endorsements.

To obtain an individual MLO endorsement to your CalBRE license, you first register for an NMLS ID number.

Then, you’ll need to:

- complete 20 hours of pre-endorsement education [Bus & P C §10166.06(a)];

- successfully pass a written exam administered by the NMLS on federal and state mortgage lending laws [Bus & P C §10166.06(d)]; and

- submit an application for the MLO endorsement through the NMLS. [Bus & P C §10166.04(a)]

In addition to the minimum requirements to be met by all MLOs, CalBRE licensees may not have had an MLO license revoked in any governmental jurisdiction.

CalBRE doesn’t enforce a minimum credit score. Likewise, negative financial events, such as bankruptcies are not cause for an automatic denial of an MLO endorsement.

Instead, CalBRE looks for a history of liens, judgments, mishandling of trust funds, or financial or personal conditions which indicate a pattern of dishonesty on the part of the applicant. The credit report is used to verify or refute the financial history you provide in the application. [Bus & P C §10166.05(c); 10 Calif. Code of Regulations §2758.3]

CalBRE MLO-endorsed licensees do not need to post a surety bond, or meet minimum net worth requirements.

Only the individual endorsements require education, background checks and fingerprinting.

The corporate broker endorsements require only application and renewal. CalBRE MLO endorsements are good through December 31st of each year if issued prior to November 1st. Endorsements issued on or after November 1st are valid through December 31st of the next year.

Endorsements and fees for sales agents

A CalBRE sales agent is only able to originate mortgages on behalf of their employing broker when they and their CalBRE broker both hold MLO endorsements. [10 CCR §2756]

To apply for an MLO endorsement as a CalBRE sales agent, you’ll complete NMLS Application Form MU4 online at the NMLS website.

Fees for obtaining an individual sales agent CalBRE MLO endorsement include course fees payable to an approved course provider, a $300 CalBRE endorsement fee, a $30 NMLS processing fee, a $15 credit report fee and a $36.25 background check fee.

Endorsements and fees for brokers

Initially, as a CalBRE broker, you’ll need to register for an NMLS ID number. Then, your CalBRE MLO endorsement filing depends on how you structure your brokerage business. For endorsement purposes, you’ll either apply as a broker-associate employed by another broker, a sole proprietor or a corporation.

Broker associates

Broker associates are employees of another broker and only need to obtain an individual broker endorsement using NMLS Application Form MU4 online.

Fees for obtaining an individual broker MLO endorsement include:

- course fees payable to an approved course provider;

- a $300 CalBRE endorsement fee;

- a $30 NMLS processing fee;

- a $15 credit report fee; and

- a $36.25 background check fee.

Broker as sole proprietor

A broker who practices as a sole proprietor needs to apply for both:

- an individual CalBRE broker MLO endorsement, using NMLS Application Form MU4 online; and

- a company CalBRE broker MLO endorsement using the NMLS Application Form MU1 online.

In addition to meeting the requirements for the individual CalBRE broker MLO endorsement, a broker practicing as a sole proprietor is required to provide on the application to the NMLS:

- any trade names in use;

- a registered agent for service of process;

- the broker designated as the qualifying individual; and

- an explanation of any criminal convictions.

The fee for the sole proprietor application is $100, payable to the CalBRE through the NMLS website.

Broker as a corporation

A broker who practices under a corporate license is required to obtain both:

- an individual CalBRE broker MLO endorsement using NMLS Application Form MU4 online; and

- a corporate CalBRE broker MLO endorsement using the NMLS Application Forms MU1 and MU2 online.

In addition to meeting the requirements for the individual CalBRE broker MLO endorsement, a broker practicing under a corporation endorsement is required to provide on the application to the NMLS:

- any trade names in use;

- a registered agent for service of process;

- the broker designated as the qualifying individual;

- identification of non-licensed officers or stockholders owning 10% or more of the corporation; and

- an explanation of any criminal convictions.

The fee for the corporate CalBRE broker endorsement application includes:

- a $300 license fee;

- a $100 processing fee; and

- a $15 credit check fee for each of the non-licensed officers and stockholders.

All fees are payable through the NMLS website.

Branches

Branch offices require you to designate a branch manager, have the branch manager explain any criminal convictions on their record and pay a $20 NMLS processing fee.

Maintain

A CalBRE broker or sales agent license is renewed with the CalBRE every four years from the date of issuance. Renewal consists of:

- confirming your CalBRE license is renewable;

- confirming legal presence; and

- completing 45 hours of continuing education. [Bus & P C §10170.5]

Fees for renewing a CalBRE sales agent license on time are course fees paid to an approved course provider and a $245 renewal fee paid to the CalBRE. Fees for renewing a CalBRE broker license on time are course fees and a $300 renewal fee.

The CalBRE MLO endorsements renew every calendar year between November 1st and December 31st. Renewal consists of:

- confirming the information on the NMLS registry is still current and correct;

- completing eight hours of NMLS-approved continuing education [Bus & P C §10166.10(a)-(b)]; and

- paying fees to the CalBRE through the NMLS.

Total fees for renewing a CalBRE MLO endorsement are:

- $330 for an individual salesperson endorsement;

- $330 for an individual broker endorsement, including a broker-associate endorsement;

- $100 for a company (sole proprietorship) broker endorsement;

- $400 for a corporate broker endorsement; and

- $20 for each branch office endorsement.

Under the DBO

Practice

The DBO oversees MLOs who are employees of a DBO-licensed company and make residential mortgages under one of two laws:

- the California Finance Lenders Law (CFLL) [Fin C §§22000 et seq.]; and

- the California Residential Mortgage Lending Act (CRMLA). [Fin C §§50000 et seq.]

The DBO issues company and individual MLO licenses under the CFLL and CRMLA. CFLL and CRMLA MLO companies are only able to make or broker residential mortgages through licensed individual MLOs. Individual DBO MLOs are required to work for a DBO MLO company in order to originate residential mortgages. [Fin C §§22100(d), 50002.5(c)]

CFLL

Additional restrictions apply. The CFLL licenses allow MLOs to make, broker or service residential mortgages, but only to/for other CFLL lenders. [Fin C §22004]

Further, a CFLL MLO making a loan must loan their own funds. They may not fund a mortgage through a warehouse line of credit. [10 CCR §1460]

However, CFLL companies and their employees may make both secured and unsecured consumer and commercial loans.

CRMLA

In contrast, the CRMLA was created to license mortgage bankers whose main business is making and servicing residential mortgages. The CRMLA license is the only license which allows you to service loans which you did not originate or purchase, i.e., service loans for third parties.

The CRMLA MLO license allows you to broker mortgages, but only to other CRMLA lenders, and state and federally chartered institutions.

Additionally, you don’t need a California business address to obtain a CRMLA MLO license. [Fin C §§50000 et seq.]

Obtain

All entities – corporations, limited liability companies (LLCs), partnerships, trusts and sole proprietorships — are eligible to obtain a CFLL or CRMLA MLO license.

The DBO schemes call for the company to obtain a company MLO license, and its employees to obtain individual MLO licenses. The MLO endorsements available under the DBO include:

- CFLL company license;

- CRMLA company license;

- individual MLO license; and

- CFLL or CRMLA branch licenses.

CFLL and CRMLA company licenses

As with all MLOs, the first step is to obtain an NMLS ID.

Then, if you’re starting an MLO company under the DBO scheme, you need to provide on the application to the NMLS:

- any trade names in use;

- a registered agent for service of process;

- identification of the qualifying individual of record;

- a business plan;

- a certificate of good standing from the California Secretary of State (SOS);

- formation or incorporation documents, if applicable;

- a management chart, including a statement that all members, directors and principals are at least 18 years old;

- an organizational chart;

- fingerprints and background check authorization for the company’s controlling members;

- an authorization of disclosure of financial records;

- financial statements showing a minimum net worth of:

- $50,000 for a CFLL license, if you are only brokering loans; or

- $250,000 for a CFLL license, if you are lending as well as brokering loans [Fin C §22104]; or

- audited financial statements showing a minimum net worth of $250,000 for a CRMLA license [Fin C §50201];

- surety bond coverage of $25,000 to $200,000 for each company license, depending on the company’s residential mortgage volume in the preceding year [10 CCR §1437, 10 CCR §1950.205.1]; and

- pay fees to the DBO through the NMLS.

CRMLA licenses need to include proof of federal agency approval if they make or service consumer mortgages subject to the approval of any of the following entities:

- the Federal Housing Administration (FHA);

- the U.S. Department of Veterans Affairs (VA);

- the Farmers Home Administration;

- the Government National Mortgage Association (Ginnie Mae);

- the Federal National Mortgage Association (Fannie Mae); or

- the Federal Home Loan Mortgage Corporation (Freddie Mac).

CFLL and CRMLA branches

Branch offices require you to designate a branch manager, have the branch manager explain any criminal convictions on their record and pay fees of:

- $320 for a CFLL branch; and

- $20 for a CRMLA branch.

Additionally, a CFLL branch requires fingerprinting of the branch manager, and a written agreement between the branch manager and the CFLL company.

Note that a CRMLA branch license is required for an out-of-state office location if it conducts residential mortgage business in California under the CRMLA.

Under the DBO, branch office requests must be made at least ten days before engaging in business at the branch location. [Fin C §22102]

Individual MLO

To obtain the individual MLO license under the DBO scheme, you’ll need to:

- obtain an NMLS ID;

- complete 20 hours of pre-endorsement education, including two hours of DBO-specific mortgage law [Fin C §§22109.2(a), 50142(a)];

- successfully pass an exam administered by the NMLS on federal and state mortgage lending laws [Fin C §§22109.3, 50143];

- submit an application for the MLO endorsement through the NMLS;

- submit a statement of citizenship to the DBO [Fin C §§22100 et seq., 50000 et seq.]; and

- pay fees to the DBO through the NMLS.

In addition to meeting the minimum requirements for all MLOs, you’ll need to show you’ve:

- never had an MLO license revoked by any regulatory agency; and

- obtained employment with a CFLL or CRMLA MLO company. [Fin C §§22109.1, 50141]

Fees for obtaining DBO licenses are:

- $330 for an individual MLO license, plus a $15 credit report fee and a $36.25 background check fee, all paid through the NMLS;

- $400 for a CFLL company MLO license paid through the NMLS, plus $20 per controlling member for Livescan fingerprint processing paid through the DBO; and

- $1,100 for a CRMLA company MLO license paid through the NMLS, plus $20 per controlling member for Livescan fingerprint processing paid through the DBO.

Maintain

Both company and individual DBO MLO licenses are good through December 31st of each year if issued prior to November 1st. Endorsements issued on or after November 1st are valid through December 31st of the next year.

The DBO MLO licenses renew every calendar year between November 1st and December 31st. Renewal consists of confirming the information on the NMLS registry is still current and correct.

DBO MLO renewal processing fees are:

- $100 for companies;

- $30 for individuals; and

- $20 for branches.

DBO MLO companies also pay annual assessment fees based on their mortgage volume in the prior year. The minimum annual assessment is:

- $250 for a CFLL license; and

- $1,000 for a CRMLA license.

Individual MLOs under the DBO are required to:

- complete eight hours of NMLS-approved continuing education, including one hour of DBO-specific mortgage law; and

- pay $330 renewal fees, plus an additional $100 reinstatement fee for late renewals. [Fin C §§22109.5(a), 50145]

All fees are paid through the NMLS.

Next in this article series: Transitioning from one MLO licensing scheme to another — coming soon!

{kind=link}

Thank you Giang Hoang-Burdette for helping to clarify (to some extent) the requirements for a broker to obtain the NMLS endorsement to broker loans. It’s something I have asked First Tuesday about. At one point in time I was an appraiser. Then…the gov’ment decided to form another “bureau” as a middle man between the appraiser and the bank. Then they also required “licensing.” I had already taken a lot of appraisal courses, but again, I bought the required courses, studied some more, took the test and got my “Trainee’s license.” Then the state required that you have a “sponsor” who would review your work and be responsible for what you did. I searched in vain for someone who would sponsor me, with no luck.

All my time effort and money spent was for nothing. Most licensed appraisers did not want: 1. Anyone else coming into the business and taking their work 2. Did not want to be responsible for someone else’s work. (I offered to PAY the sponsor). I am still upset to this day. Now we are looking at the same kind of bureaucracy regarding brokering loans. We must spend more money for study, testing, etc., as if this is going to protect consumers by making dishonest loan brokers more honest. Just sayin’.

Thanks again for clarification. First Tuesday is a valuable asset.

Isn’t organized real estate fun now…please more regulation LOL