Employment numbers in thousands

Data source: State of California Employment Development Department

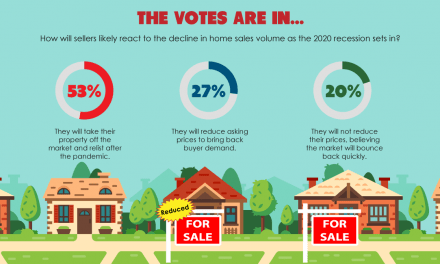

Employment and the real estate cycle

Employment is a necessary condition for those who depend on their daily labor to provide funds to pay for food, shelter, and recreation. For brokers and owners of property for sale, employment (or other income) by a client is required for a sale involving purchase-assist financing.

As the number of people employed increases, more people will qualify to buy homes and become less resistant to taking on the debt of a mortgage.

Conversely, when the number of people employed decreases, fewer ready and willing property buyers are now able to qualify for a loan, resulting in fewer sales. With dropping employment numbers, prospective homeowners become more debt averse. Those with a job and the capacity to carry a mortgage and the operation costs associated with homeownership put off a purchase, running with the herd until there is a clear indication that employment is more stable, indicating a healthier economy.

As employment rises, a cycle of improving sales begins, to once again become a virtuous cycle of real estate and general prosperity among brokers, builders, and sellers, until the next real estate recession occurs and the cycle once again becomes vicious.

Welcome to economic Darwinism.

Analysis

As an employment downturn occurs and foreclosures and bankruptcies rise, the losers during the recessionary period are displaced. They tend to escape the unhappy environment they find themselves in when displaced by relocating, many leaving the state to settle elsewhere in a new economic and social lifestyle. Some remain as tenants in less expensive digs, hostile to the risks posed by homeownership.

California is usually the first in the nation to experience a decline in employment numbers when a recession hits, and the first to show rising employment numbers when the economy recovers.

Small business is said to be the business of California. The remainder of the nation (with the exception of New England) is primarily corporate with large companies and tight small-town social webs requiring smaller employers to hoard employees. Small businesses in a fluid and mobile population like California (with a far smaller rate of homeownership than the mid-western, central and southern states) can and do shed employees at the first sign of a slowdown in their business revenue. Corporations employing large numbers of people are internally inflexible because of regulations prohibiting off-loading excess employees, as are small-town employers.

As a result, California employment quickly adjusts to demand, and redundant employees are released at the earliest sign of a recession trend. Thus, brokers, builders, and sellers of homes begin to feel the pinch of the recession in reduced sales as the California economy begins to implode.

Conversely, as business neutralizes (bottoms out) and an increase in business revenues take hold, employment also turns up and voila, there are more people who qualify for a mortgage because they are employed.