This form is used by a seller’s agent when preparing a listing/marketing package or performing a due diligence investigation on a property, to request information from the Improvement District Office about Mello-Roos assessments encumbering the seller’s property for disclosing the terms of the bonded indebtedness to a buyer assuming the debt.

Funding off-site improvements with Mello-Roos

The subdivision of a property carries with it the need for access to roads and facilities, none of which are located on any of the parcels created for sale.

The parcels created for sale as lots or condominium units are themselves either improved with structures or unimproved.

A subdivider’s financing scheme to fund off-site improvements is called Mello-Roos.

Mello-Roos are deceptively titled a special tax, but they do not function as a tax in actual practice.

However, the tax collection authority for each county is established as the agent for the improvement district agency to collect the installments due on the 20-year amortized payoff of the Mello-Roos bonds.

The annual installment payment is called an “assessment,” also a fabricated misnomer. The assessment is actually the allocation of the total costs of the related off-site improvements to each property. [Calif. Government Code §§53311 et seq.]

The debt secured by each lot to repay the bonds has a principal amount which remains due and unpaid until it is prepaid or fully amortized.

The interest rate on the remaining principal due is set by the rate of the bonds. At any time, the lien for the improvement bonds can be paid off by the owner. When this occurs, the “special tax” lien is released from title to the owner’s parcel.

These infrastructure improvement bond liens are junior to annual property taxes.

The “special tax assessment” misnomer used to label the semi-annual installment payments due on an improvement bond lien is deceptive.

The title as “taxes” leads prospective buyers to believe they are dealing with an annual property tax — which they are not.

Avoiding misleading disclosures

Sellers and their agents, when structuring the terms for payment of the price in a purchase agreement offer, often ignore the principal amount of the bonded indebtedness on the property, except only to prorate the current principal and interest installment on the lien, not the principal balance remaining on the lien.

It is the buyer’s agent who has the duty to further advise their buyer about the lack of an accounting for the bond, rather than simply “going along” with the boilerplate purchase agreement pricing and defective proration arrangements.

The deception associated with these bonds prompted the California legislature to introduce legislation to ensure prospective buyers of real estate receive sufficient information to make an informed decision. [Calif. Civil Code §1102.6b]

Sellers (and thus, sellers’ agents) are mandated to give buyers of Mello-Roos encumbered properties:

- a notice of the lien for the bonded debt and an opportunity to decide whether or not to assume the debt before entering into a purchase agreement [See RPI Form 137]; or

- the right to renegotiate the terms for payment of the price when they have already agreed to buy before receipt of the notice.

When fully informed, the buyer (and thus, the buyer’s agent) may prudently require the bond amount to be credited toward the price paid since its entire principal amount has accrued and cannot be prorated.

Statutory notice of assessment

The sale of property comprised of one-to-four residential units and encumbered by a Mello-Roos or 1915 Improvement Act improvement bond requires the seller to disclose the existence and terms of the bonded indebtedness. [CC §1102.6b]

To comply, sellers need to obtain and deliver to prospective buyers a notice prepared by the improvement district office entitled either Notice of Assessment or Notice of Special Tax. [See RPI Form 137]

Anyone can request a Notice of Assessment from the office of the improvement district at any time, including both the seller’s agent and the buyer’s agent.

No particular manner of request is required since it may be provided either orally or in writing.

The district office needs to deliver the notice to whoever requests it. Delivery is done within five working days of the district office’s receipt of the oral or written request. The maximum charge for the service is $10. [Gov C §53754(b)]

The seller has the primary obligation to request the notice and deliver it to prospective buyers. Thus, the seller’s agent is to advise the seller to request the notice when entering into the listing agreement employing the broker’s office to sell the property. [See RPI Form 137]

The seller’s agent needs to include the notice in the listing package prepared for disclosing to prospective buyers significant relevant information about the property.

Information presented in a listing package is either mandated, as in the case with assessment bonds, or known to the seller and seller’s agent to exist.

When the prospective buyer enters into a purchase agreement with the seller before the Notice of Assessment is delivered to the buyer, the buyer has a statutory contingency allowing the buyer to cancel the purchase agreement.

The buyer has three calendar days after hand delivery of the Notice of Assessment (five days after posting it by mail) to cancel the purchase agreement by handing a Notice of Cancellation to the seller or seller’s agent (not escrow or the buyer’s agent). [Gov C §53754(c); See RPI Form 183]

Whether a buyer receives a Notice of Assessment before agreeing to buy or after, the contents of the notice, without further explanation or information, have fulfilled the seller’s and their agent’s general statutory duty owed to the buyer to disclose the existence of the assessment. [See RPI Form 137]

The Mello-Roos assessment notice contents

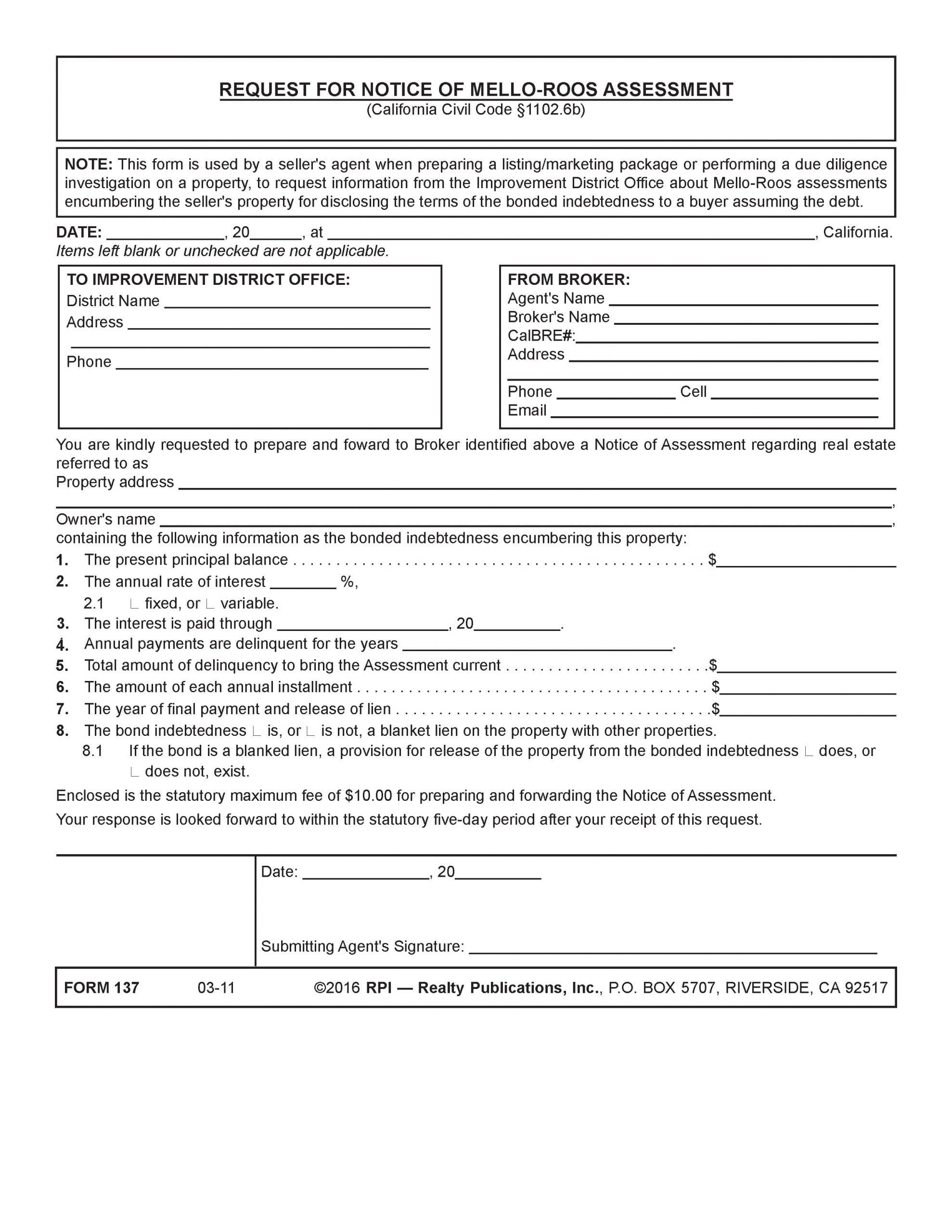

A seller’s agent uses the Request for Notice of Mello-Roos Assessment form published by Realty Publications, Inc. (RPI) when preparing a listing/marketing package or performing a due diligence investigation on a property. The notice requests information from the Improvement District Office about Mello-Roos assessments encumbering the seller’s property. The seller will disclose the terms of the bonded indebtedness to a buyer assuming the debt. [See RPI Form 137]

The contents of the Request for Notice of Mello-Roos Assessment includes spaces for the Improvement District Office to fill out the information, including the:

- present principal balance [See RPI Form 137 §1];

- annual rate of interest as a percentage, and whether it is fixed or variable [See RPI Form 137 §2];

- date or length of time for which the interest is paid [See RPI Form 137 §3];

- years for which the annual payments are delinquent [See RPI Form 137 §4];

- total amount of delinquency to bring the assessment current [See RPI Form 137 §5];

- amount of each annual installment [See RPI Form 137 §6];

- amount on the year of final payment and release of lien [See RPI Form 137 §7]; and

- whether the bond indebtedness is or is not a blanket lien on the property with other properties. [See RPI Form 137 §8]

The submitting agent will then provide their signature at the bottom of the form and enclose the maximum fee of $10.00. [See RPI Form 137]

Form navigation page published 04-2022. Updated 01-2026.

Form last revised 2016.

Form-of-the-Week: Request for Notice of Mello-Roos Assessment and Notice of Your Supplemental Property Tax Bill — Forms 137 and 317

Article: Transparent solicitation of offers via a marketing package

Article: California limits property tax deduction to…well, taxes

Blog: California homebuyers think twice about high homeownership costs

Client Q&A: What are special assessments and Mello-Roos bond payments?

Word-of-the-Week: Encumbrance