The following local markets are overvalued in 2016, according to CoreLogic:

- San Jose, where average home prices have increased 81% since 2012;

- Oakland, where home prices have increased 78% since 2012;

- Riverside, where home prices have increased 56% since 2012;

- Los Angeles, where home prices have increased 54% since 2012; and

- Irvine, where home prices have increased 44% since 2012.

CoreLogic identifies these overvalued California’s housing markets using two metrics:

- the growth of home prices-to-incomes; and

- how fast home prices are rising in relation to area rents.

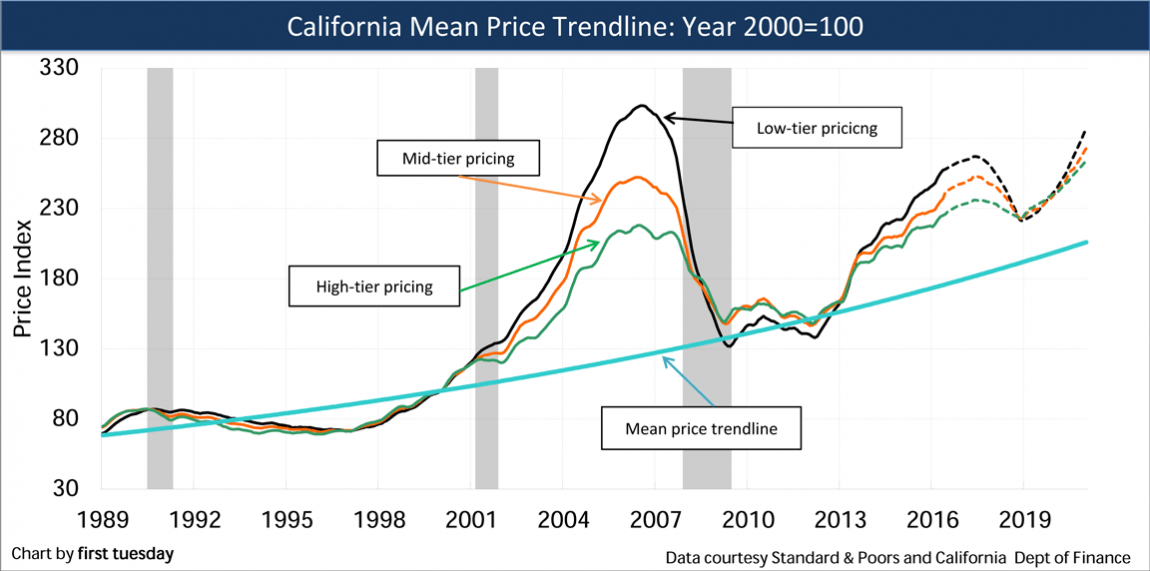

The price-to-income ratio, championed by the creators of the Case-Shiller home price index, is also adapted by first tuesday into the mean price trendline. This trendline shows long-term home prices are limited to a 3% growth rate per year. However, on a short-term scale, prices can rise faster than incomes for several months or even years, as they did during the Millennium Boom and to a lesser but significant extent in the 2013-2016 period. They can also fall, as usually occurs at the conclusion of a boom, likely to be reminiscent of the past three years ending in 2017.

The price-to-income method is signified in the blue line in the chart below:

The chart shows home prices oscillating gently above and below the mean price trendline prior to the year 2000. Then, home prices rose far quicker than incomes during the Millennium Boom, which signified a bubble to anyone who was paying attention at the time. That’s because home prices are ultimately set by homebuyer ability to earn and pay. Further pricing volatility is to be expected for five or more years before the price illusions still held by our California home seller population about past valuations dissipate, and we enter a stable period of sustainable upward sales volume and pricing of real estate and do so in the face of a 30-year half cycle of rising FRM and capitalization rates.

During the mid-2000s housing bubble, the purchasing power of homebuyer incomes was artificially inflated by over-use of adjustable rate mortgages (ARMs), piggyback financing and low-to-no downpayment acquisitions. Lenders and agents told buyers they could always refinance out of their dangerous ARM into a fixed-rate mortgage (FRM) — or sell for a profit — before the rate reset and their payment increased beyond their ability to pay. Resetting usually occurred five years after purchase depending on the type of ARM. However, when the time arrived for homeowners to refinance, the vast majority of those who purchased during the Boom were underwater on their mortgages and unable to refinance as the inevitable bust followed the unregulated boom.

Was the foreclosure crisis a direct result of these adventurous mortgage financing events, or malfeasance by appraisers, brokers, their agents and credit agencies?

Bubbles rise, bubbles pop

Why do bubbles happen?

Bubbles occur in any economic sector when investors overvalue an asset such as real estate. For an example from the stock market, recall the dot-com bubble which popped in 2000. In this case, investors-made-speculators bought up any stock having to do with the internet — dot-coms — in expectation of future rises. This activity rapidly inflated the value of dot-com stocks, based purely on market momentum, not on whether the dot-coms were actually making profits (most weren’t).

Like all bubbles do, the dot-com bubble burst, taking with it the fortunes of many ill-informed investors and heralding the failure of several large internet companies dependent on funding of their negative cash flow business models.

Bubbles occur for similar reasons in the housing market. In California, speculators again became overly active beginning mid-2012, purchasing homes at then-low prices at a rapid pace, buying and selling within a matter of months and profiting on market momentum alone.

While speculator activity has subsided, prices continued to rise faster than incomes across California in 2016. Are we in the midst of another bubble, and if so are we heading for a bust?

It’s possible, but not expected at this time. Advantageously, conditions today in California jobs and personal debt leveraging are the opposite of their positions going into the 2006 boom-to-bust period.

Importantly, California home prices are on average now down to 5% higher than last year for high-tier homes, 6% higher for mid-tier homes and 9% higher in low-tier home sales as of August 2016. While higher than income growth for most Californians, the state’s home price increase has slowed in 2016 as employed wage-earning homebuyers find it more difficult to find suitable homes in their static price range. The good news is, as prices continue to level off and other economic conditions in California will likely remain stable for the foreseeable future, the potential for a sudden burst becomes much less likely.

That being said, a couple of complications are around the corner. The Federal Reserve (the Fed) is set to raise the key short-term rate sometime in the coming months. This movement will ripple through the national economy, causing ARM rates to increase (in California). In the meantime, there is the present shock remaining in the financial markets caused by the election of Trump which has prematurely caused mortgage interest rates to increase swiftly, from 3.49% to 3.73% over the course of election week and up to 3.86% in the week following, according to Bankrate.

Homebuyers reliant on mortgage financing have seen their buyer purchasing power reduced by thousands of dollars overnight due solely to the single event of the election. Some closings will not take place. Since prices are set by homebuyers’ ability to pay, home prices need to adjust downward for homebuyers to buy at today’s higher interest rates. Prices will need to make this adjustment before real estate sales volume will start its recovery, rising to a satisfactory level which will support the current bevy of active agents and brokers with sufficient fees.

The downward price adjustment was going to take place in 2017 anyway without the added asset-devaluating effect of upward FRM rate movement following the election on November 8. Prices have been increasing beyond wage increases for the past three years and year-over-year sales volume has been dropping for over a year now, since October 2015. A sales volume decline itself heralds in a price slippage 12 months later, unless offset by market events not yet experienced (such as dramatic wage increases, cheap mortgage money, inflation, a weaker dollar, fiscal stimulus, etc.).

Still, a downward adjustment is not necessarily the same as a bubble bursting. Recall the gradual price movement that was common before the year 2000, seen in the chart above. It’s natural for any overheated market to take a downturn eventually — that’s why the Fed acts to raise interest rates in times of economic success, to keep the market from becoming overblown and prevent or diminish the inevitable bust that follows.

In this case, the downturn will likely be brief and much more gradual than experienced in 2007-2008. That’s because we’re entering an economic expansion in California, with jobs returning and incomes rising at a healthy pace (which will beneficially be lifted by increased government spending in 2017). Further, the coming demographic shift of Baby Boomers retiring and Generation Y seeking to become first-time homebuyers will add fuel to the next home price rise, anticipated to peak in 2019-2021.

Better yet for California growth is the fact the nation’s better educated, higher skilled and physically healthiest Americans are naturally attracted to the California environment, economically, geographically and culturally. We might also cautiously add, politically. Go west young man, go west.

{kind=link}

So, what type of price correction do you anticipate in Orange County?