Form-of-the-Week: LLC Operating Agreement – for a Self-Directed IRA – Form 372-3

Today’s cyclically low real estate prices coupled with favorable rental occupancy conditions have drawn the attention of individuals with Individual Retirement Accounts (IRAs) who are interested in shifting from stocks and bonds to ownership of real estate.

An IRA owner with a few hundred thousand dollars in their IRA may direct, manage and control the investment of those funds to buy and own real estate. To invest IRA funds in income property, the IRA owner simply establishes and transfers accumulated IRA funds to a separate self-directed IRA (SDIRA).

Related article:

On the advice of their agent, an IRA owner with sufficient funds in their IRA will establish an SDIRA to shift the control of investment decisions from the IRA custodian to themselves. With an SDIRA, a custodian’s primary duty is limited to administer the underlying IRA account on the owner’s behalf.

It is the IRA owner, with the diligent help of their agent, who is responsible for locating and negotiating the terms for acquisition of the income property to be purchased by the SDIRA. This shift in responsibilities significantly reduces custodial fees and cost associated with the custodian’s administrative work for the IRA.

When investing in real estate, a prudent investor practices risk management and asset preservation. As a shield against remote liabilities, they place title to their real estate ownership in the name of a limited liability company (LLC) they establish, which their agent helps them set up.

Establishing an SDIRA LLC provides LLC title protection. The SDIRA LLC entity shields the owner’s other IRA funds and personal assets held outside of the LLC from a loss resulting from the ownership of the property vested in the LLC, and vice versa.

The primary IRA benefit of forming an SDIRA LLC is the IRA owner gains “checkbook control” in addition to investment selection and acquisition control. Checkbook control gives the owner, as the managing member of the SDIRA LLC, direct checkbook access to the IRA funds.

Thus, purchasing a property using an SDIRA LLC allows the owner to simply write a check from the SDIRA LLC bank account opened to hold the IRA funds to close transactions. On acquisition, title to the property is vested in the name of the LLC. The same owner access to IRA funds applies for the payment of any expenses they incur operating the property owned by the SDIRA LLC, including:

- maintenance;

- repairs;

- renovations;

- property taxes; and

- insurance premiums.

Again, no fees are due the IRA custodian since they are not involved in these operating disbursements.

Related article:

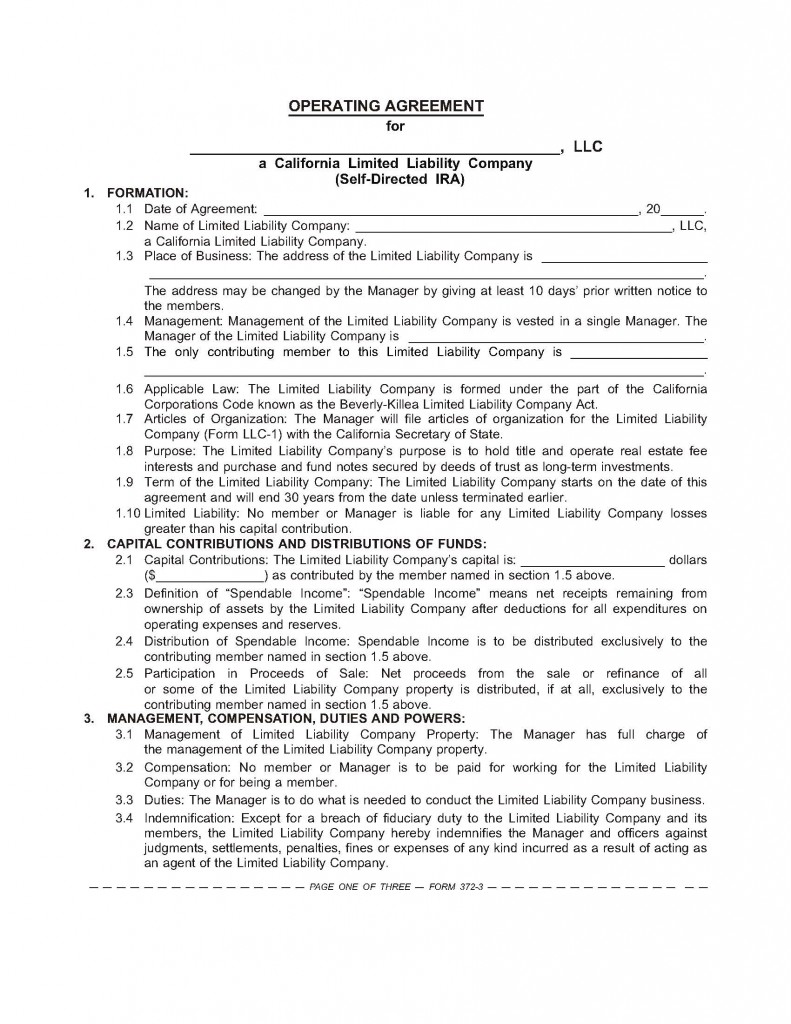

To form an LLC, the IRA owner:

- selects a name for the LLC ending with the words “Limited Liability Company,” “LLC” or “L.L.C.” The words “Limited” and “Company” may be abbreviated to “Ltd.” and “Co.” [Calif. Corporations Code §17052(a)];

- signs and files articles of organization using an LLC-1 form issued by the Secretary of State [Calif. Government Code §12190(b); Form LLC-1];

- appoints a registered agent (usually the IRA owner) to accept service of process in the event the LLC is sued [Corp C §1505];

- prepares an operating agreement detailing the management, membership, special advisors and distribution of monies by the LLC [IRC §408 and 4975; See first tuesday Form 372-3 and 372-4]; and

- files a Statement of Information with the Secretary of State within 90 days after filing the articles of organization for the LLC. [Corp C §17060; Gov C §12190(k); Form LLC-12]

first tuesday’s LLC Operating Agreement – for Self-Directed IRA is designed to meet custodians’ requirements for SDIRA LLCs. For an IRA owner, it becomes a boilerplate form to easily assist in the creation of the LLC. A pdf version and an editable Word document are both available to aid with the IRA owner’s individual needs. [See first tuesday Form 372-3 and 372-4]

The SDIRA LLC is generally a single-contribution-member LLC. The LLC’s sole ownership member will be the IRA which contributed capital to the LLC. The IRA owner contributes no capital to fund the LLC.

Rather, the IRA owner is limited to acting as the managing member of the LLC, with no contribution and no percentage ownership interest in the LLC. Special management provisions stating the LLC is to be managed by the IRA owner are included.

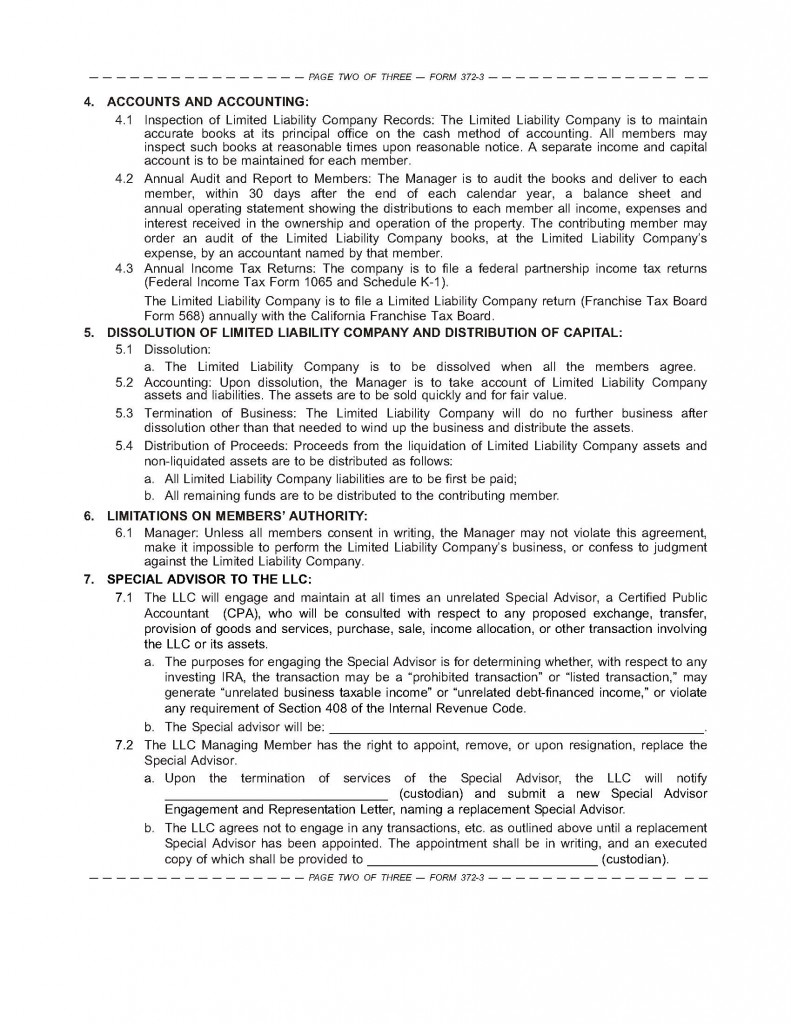

IRA custodians also require the IRA owner to appoint a “special advisor” to the LLC. The LLC operating agreement contains a special advisor provision to implement this requirement along with tax consequences and information regarding prohibited transactions. [Internal Revenue Code §§408, 4975]

A special advisor is a state-licensed certified public accountant (CPA) or attorney in good standing. This person is to be knowledgeable in IRA tax provisions and prohibited transactions. The special advisor appointment is also to be in writing, on a form provided by the custodian.

{kind=link}

Do you have operating agreement and other sample forms for Virginia llc.

Secondly for single member self controlled llc why does it need to file federal 1065 partnership return. If SDIRA llc income is not taxable, then why it need to file tax return.

Can you please send a similar Operating Agreement for TX?

This type of freedom is greatly appreciated! Thank you.

Bina,

Thank you for your inquiry. All first tuesday forms are California-specific and may not be in compliance with the laws and practices of other states. Due to the diversity of each state’s laws and practices, we do not produce forms for use outside of California.

Regards,

ft Editorial Staff

Any chance u have an operating agreement for Virginia?

All first tuesday Forms are 100% legal for use in California, though are not designed to be compliant with the law and practices of other states.

Do you have a sample LLC operating agreement for Michigan?

Thanks Fernando, it’s very helpful. I appreciate if you can send me a similar Operating Agreement for TX. Thanks.

Thsi si great. Do you have a similar Operating Agreement for Colorado?

Thank you