U.S. home values have officially more than doubled from their 2009 low which followed the disastrous post-Millennium Boom crash — but California passed that milestone years ago.

Spurred on by record-low mortgage interest rates, home value growth during 2021 represented a $1.38 trillion or roughly 20% annual increase in California alone. In terms of dollars, California’s largest metro areas contributed the most growth, with first place going to Los Angeles, followed by San Francisco and San Diego, according to Zillow.

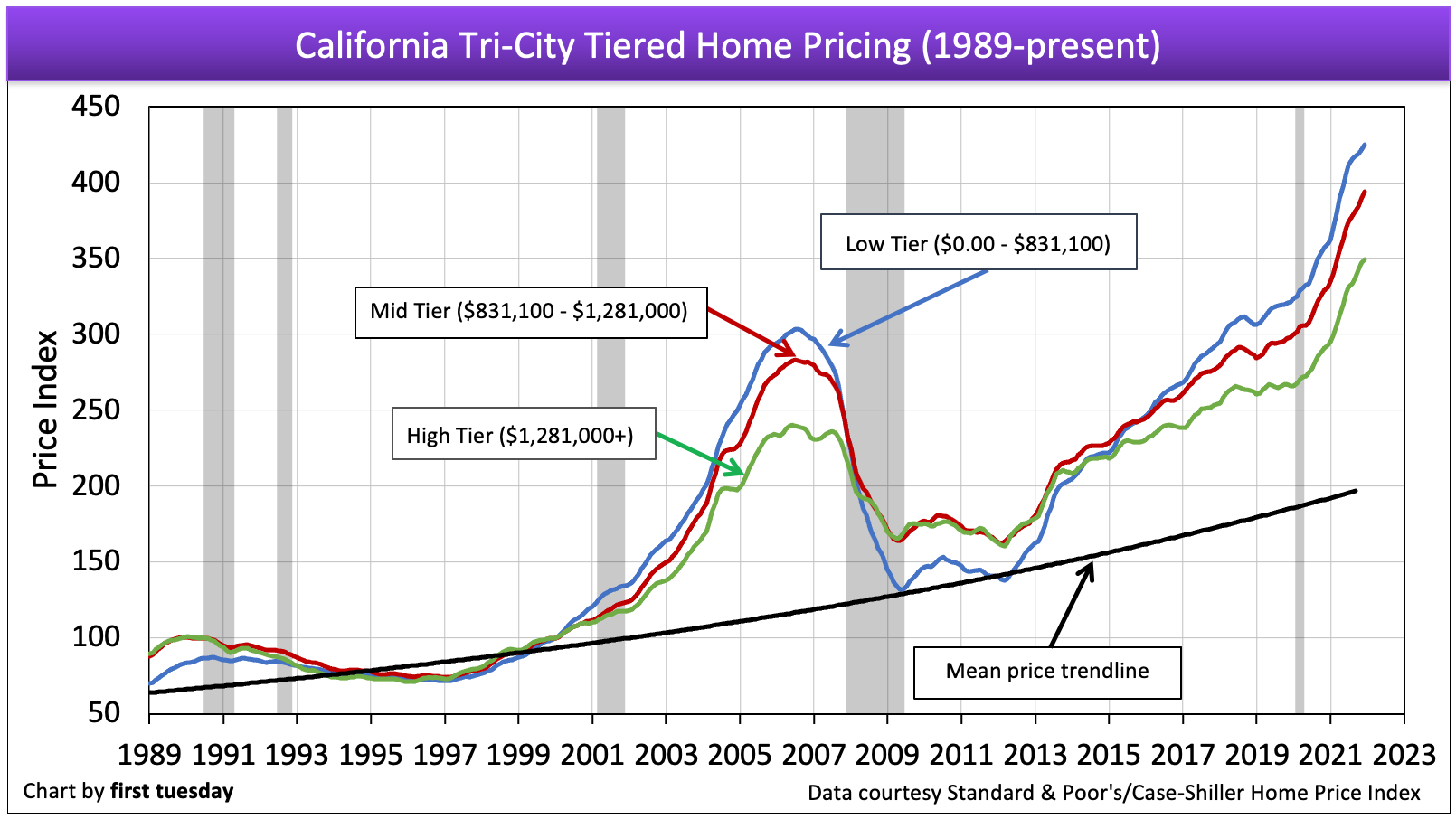

In general, the past two decades have seen more volatile home price movement here in California compared to much of the U.S. For example, since bottoming in 2009, as of December 2021, California home prices have increased a whopping:

- 222% in the low tier (equal to low-tier homes more than tripling in value);

- 154% in the mid tier (equal to mid-tier homes midway between doubling-and-tripling in value); and

- 133% in the high tier (equal to high-tier homes more than doubling).

Here’s how this level of price change can be visualized:

Read more and view metro-level price changes: California tiered home pricing

California’s unequal housing burden

While the Millennium Boom saw home values increase at a faster rate (tripling in the low tier within a span of just six years), California’s more recent home value increases — experienced over the past 12 years — have far surpassed the Millennium Boom rise.

For a look into the dollar-level impact on prices, at the end of 2021, a low-tier home averaged across California’s largest metros is considered to be any home valued under $831,000. Back in 2000, a low-tier home was considered any home under $256,000. This is equal to a 360% increase. For comparison, the typical low-tier home has increased “just” 179% nationwide over the same period of time, according to the Standard & Poor’s CoreLogic-Case Shiller Home Price Index.

Meanwhile, from 2000 to 2020, the typical Californian’s personal income has increased 110%, according to the Bureau of Economic Analysis (BEA). This amount of income increase falls far short of what is necessary to keep up with home price increases.

The direct result has been a decreased homeownership rate for California. For real estate professionals, this translates to fewer transactions to go around, requiring more hustle — and less certainty — to make a living.

California’s homeownership rate was 54.3% as of the fourth quarter (Q4) of 2021, according to the U.S. Census Bureau, down from 57.1% in 2000. The only state with a lower homeownership rate is New York (though both states regularly trade places for last place). In contrast, the U.S. homeownership rate is 65.5% as of Q4 2021.

The “why” behind California’s absurd home prices

The Golden State’s significant price increases can be traced back to one major factor: a severe lack of residential construction.

While homebuyer-occupant and renter demand ought to determine the level of new construction, several obstacles have held builders back from meeting demand over the past decade.

In 2021, construction increased very slightly as homebuyer enthusiasm exceeded the resale market and spilled over into new homes. However, building material shortages and labor shortages have caused delays and soaring costs, pricing out many would-be homebuyers and holding back construction increases.

But the biggest long-term obstacle facing builders continues to be restrictive zoning regulations. Not-in-my-backyard (NIMBY) advocates have long kept a stranglehold on the residential market, preventing density in the state’s most in-demand areas. Now, legislators are working to counter NIMBY efforts and enable more new housing.

For example, in 2021, legislators passed Senate Bill (SB) 9, which allows homeowners to subdivide their lots, smoothing to path for accessory dwelling units (ADUs), duplexes or even fourplexes in what are today single family neighborhoods.

As legislators continue to work to enable more housing in California, the rapid home price increases of recent years will cool, providing homebuyers some relief — and real estate professionals the chance at more transactions. More housing is good for the bottom line, and for anyone who wants a chance at the American Dream.

Related article:

{kind=link}