We asked first tuesday readers whether homebuyers with smaller down payments were growing in number or dwindling. The majority – 56% – said the number of homebuyers with lower down payments is increasing, while 40% witness a decrease. Only 4% say there is no difference.

Not much has changed over the past year. In September 2014, readers told us that only one in four homebuyers managed to save a 20% down payment. The rise in small down payments shows no sign of slowing, a trend mirrored in mortgage originations nationwide.

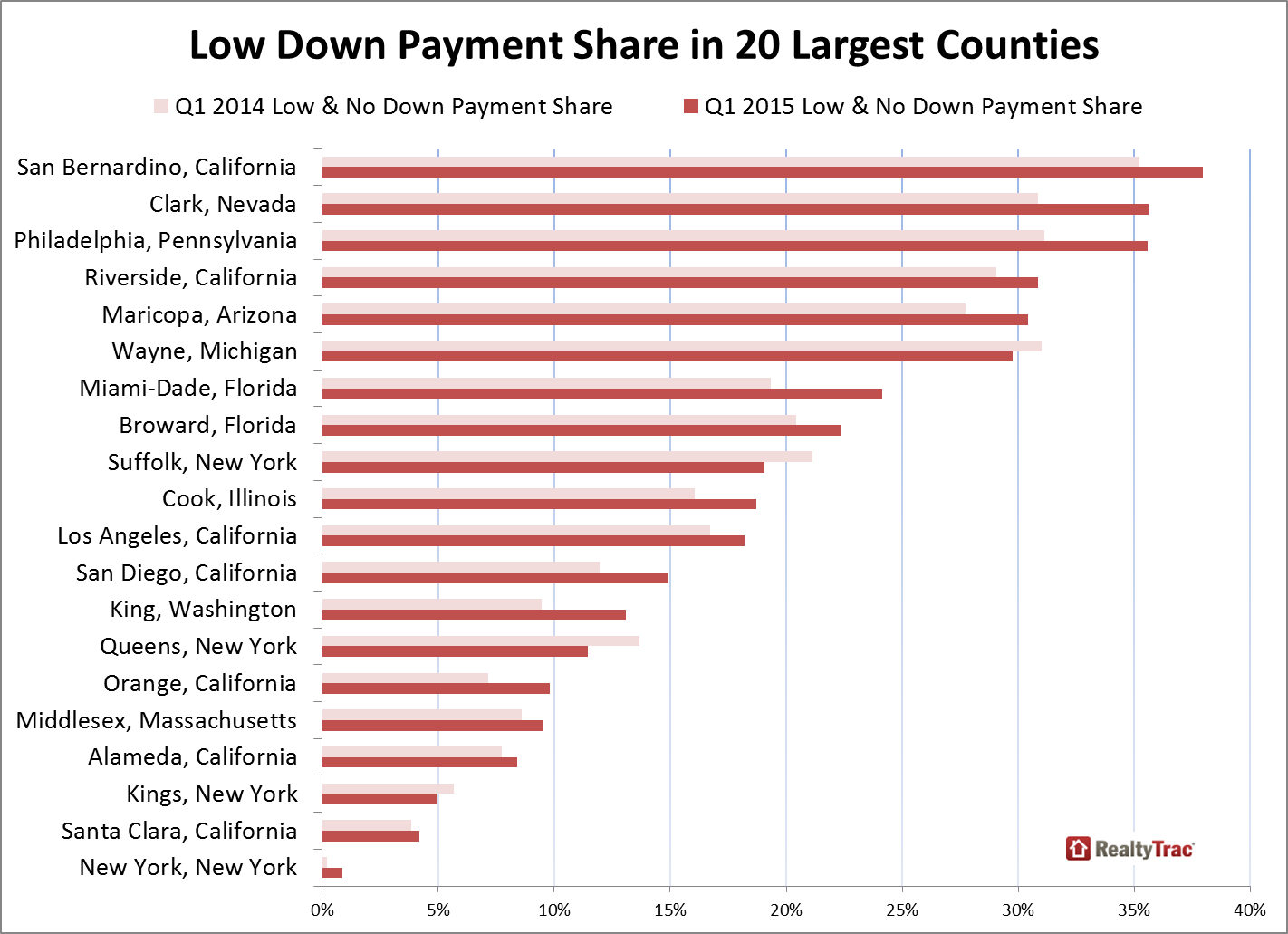

A recent report from RealtyTrac found the average down payment for U.S. residential mortgages was 14.8% in Q1 2015, down from 15.2% in Q4 2014 and 15.5% the year prior. Riverside County experienced some of the lowest down payments in the country, averaging 13.7% in Q1 2015.

Further, mortgages with loan-to-value ratios (LTVs) of at least 97% – involving down payments of 3% or less of the purchase price – accounted for 27% of all mortgages, the highest since 2012. Many California counties – San Bernardino, Riverside, Los Angeles, San Diego and Orange – were among the largest U.S. counties with the highest proportion of down payments of 3% or less.

A slip in personal savings

An increase in transactions involving a less-than-20% down payment is an inevitable result of low savings rates among first-time homebuyers. As of Q1 2015, the national personal savings rate was at 5.5% of disposable income. Though higher than the previous year, the rate is historically low as prospective homebuyers are saving less than previous generations.

The cause? First-time homebuyers in California are confronting steep rental rates and home prices, forcing them to funnel ever larger portions of their income into housing while their savings remain barren – a financially damaging trend. In fact, recent data shows the average renter in Los Angeles is spending 49% of their monthly income on rent, while San Francisco renters are spending 46% – both exceeding the recommended rent-to-income ratio of 33%.

Further, though job numbers are on the rise, employment has yet to reach full recovery and wage increases remain unreasonably low. As California renters struggle to keep up with the rising cost of living, little income remains for the sought-after 20% down payment. Their inability to save leaves them no choice but to put off homeownership, or settle for a smaller down payment and seek lenders who accommodate their limited funds. As a result, home sales have stagnated while pricing has risen on the 3.5% (down payment) bet they will keep rising or at least not drop.

Small down payments – for now

In response to market conditions and homebuyers’ tight budgets, economic policy has adapted to encourage consumer spending and provide an inflationary boost to the economy. The more of their earnings consumers spend, the higher home sales volume and employment trend.

Consequently, some lenders are amending their mortgage guidelines to allow smaller down payments. Just this year Fannie Mae and Freddie Mac launched new programs which accept down payments as low as 3%, reduced from their previous minimum of 5%.

These programs put homeownership within the reach of homebuyers with limited savings and income – inducing a lift to home sales volume by avoiding the added obstacle of a sizeable down payment. It further gives homebuyers a low-down-payment option beyond the one provided by Federal Housing Administration (FHA)-insured mortgages, which already accept down payments as low as 3.5%.

Expect more homebuyers to seek mortgages with down payments of 20% or less – and for lenders to provide them. However, with smaller down payments comes the increased need for private mortgage insurance (PMI). Homebuyers who dole out less than 20% of the purchase price up front need to prepare for the added 0.9% annual cost of PMI, paid through monthly premiums, and a long-term trend of rising mortgage rates – both adjustable rate mortgages (ARMs) and fixed rate mortgages (FRMs).

Further, though low down payments are becoming more commonplace, the greater risk of default and additional underwriting requirements mean some lenders may remain hesitant. Homebuyers still need to shop around for a mortgage as prudent practice and to find the best terms from lenders willing to offer mortgages with LTVs exceeding 80%.

As for what’s ahead in the long-term, the 20% down payment will return as the standard eventually. Once the economy recovers enough to withstand a higher savings rate, economic policy will promote larger down payments to prevent another real estate pricing bubble and bust. In the meantime, prepare to see LTVs rise as 20% down payments take a dive, one part of dealing with years of global secular stagnation.

{kind=link}