Help your homebuyers get the most advantageous mortgage terms available by using first tuesday’s Mortgage Shopping Worksheet. Together, compare mortgages offered by different lenders and contrast the fundamental mortgage variables and costs commonly occurring on origination and over the life of the mortgage.

You gotta shop around – it’s a big deal

One might imagine the majority of prospective homebuyers would spend a great deal of time considering the financing needed to fund the purchase of their biggest asset — their home. But that is not the case. Studies show Americans spend nearly twice as long shopping for and researching their car purchase — at one tenth the price — as they do for a mortgage they need to fund the purchase of a home.

The different types of mortgages, rates and lender fees all play a critical role in the sum of money a homebuyer will ultimately pay to finance their purchase. The difference between one lender’s offer and another’s can easily equate to tens of thousands of dollars over the life of a mortgage.

Remember, an adversarial relationship exists between a lender and homebuyer. The lender is selling a product — a mortgage, if not snake oil — to potential borrowers. Consequently, homebuyers have the liberty to accept or reject a lender’s offer. If the homebuyer does not accept the lender’s terms, they are free to walk away from the lender’s proposal without cost. More should, for their financial well-being.

Thus, homebuyers are to inform themselves by soliciting mortgage quotes from multiple lenders. Armed with this information, the homebuyer and their agent compare the alternative mortgages arrangements and mortgage costs available. Equally as responsible for this comparison shopping taking place is the buyer’s agent. No one else is duty bound to protect the homebuyer’s financial interests.

Balancing deceitful information asymmetry

Agents and brokers are the gatekeepers standing between the consuming population and entry into the real estate marketplace. For most, entry includes mortgages as part of the calculus.

Critically, the buyer’s agent owes a fiduciary duty to their homebuyers to assist them with acquiring the information needed to make an educated choice. Without mortgage information, a homebuyer cannot make a well-informed decision as to which mortgage offers the most advantageous terms.

Confusion exists in the trade-offs between costs and rates and fees and terms, and these are the variables lenders have learned to manipulate to their advantage in order to increase their earnings. Agents, well-versed in real estate fundamentals and lender conduct, are the only ones available to walk their homebuyers though this intentional chaos.

Thus, buyer’s agents are obligated to shepherd their homebuyers through the asymmetry of information created by the buyer’s ignorance and the lender’s silence about the real estate mortgage market and available mortgage options.

Added costs for submitting multiple mortgage applications will be incurred, and properly so. However, this cost is to be viewed as a “premium” paid to ensure the homebuyer they will receive a mortgage at the time of closing that is arranged on the best possible terms and at the least cost.

Editor’s note — Obtaining mortgage pre-approvals and submitting applications to multiple lenders will not have an adverse impact on a homebuyer’s credit score, provided the homebuyer conducts all of their mortgage inquires for comparisons within a 45-day period.

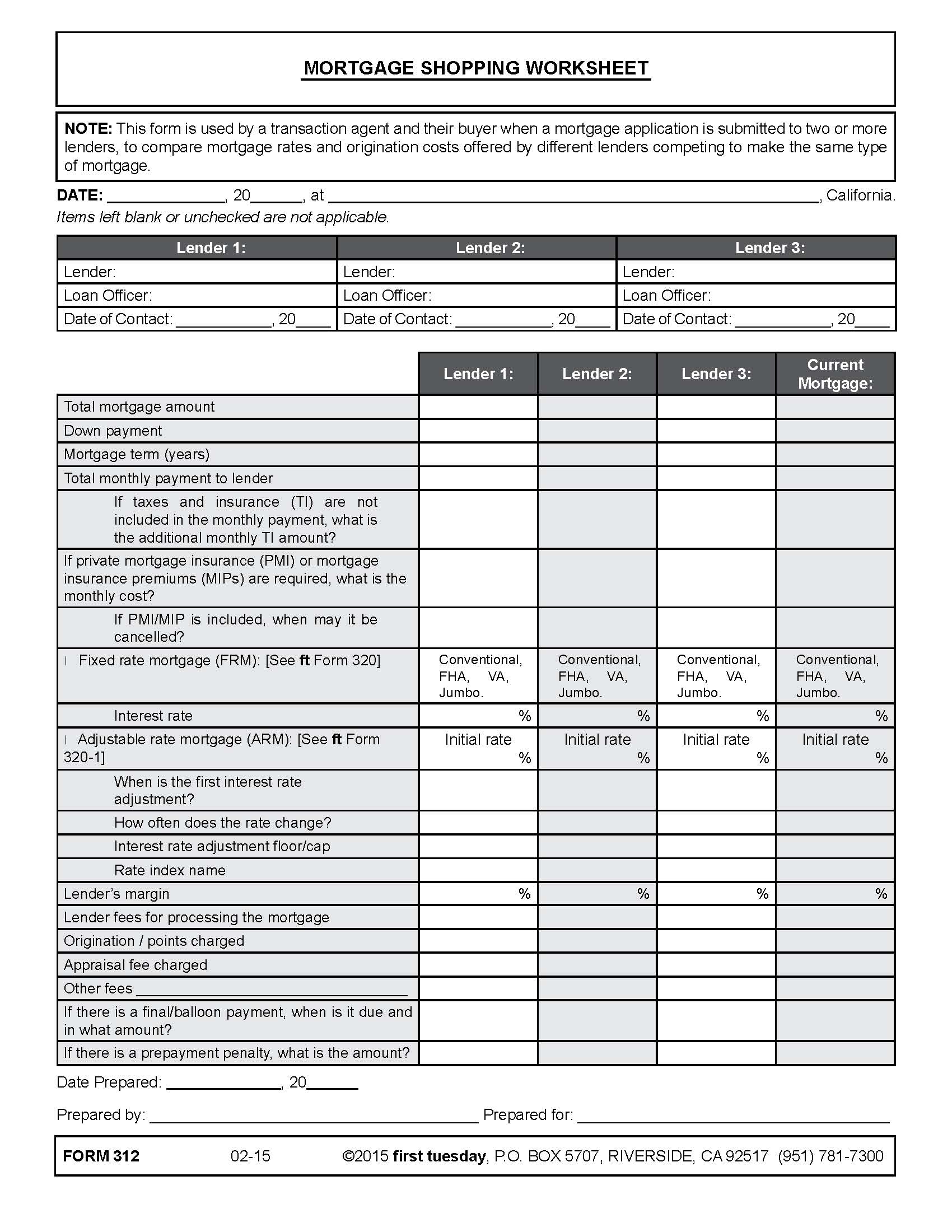

The Mortgage Shopping Worksheet makes comparisons easy

first tuesday’s Mortgage Shopping Worksheet is designed to be completed by the homebuyer with the assistance of their agent. The form contains a list of all the mortgage variables commonly occurring on origination and during the life of the mortgage. Space is provided for the entry of mortgage terms offered by three competing lenders, and the terms of an existing mortgage when an owner is refinancing.

The Mortgage Shopping Worksheet contains the critical details of three different mortgages in friendly columnar format, including:

- the total mortgage amount to be funded;

- the size of the down payment the homebuyer intends to put down;

- the mortgage term in years;

- the estimated total monthly payment the homebuyer will be paying to the lender;

- the monthly cost of private mortgage insurance (PMI) or mortgage insurance premiums (MIPs), if required;

- whether the mortgage has a fixed or adjustable rate of interest, and the associated rates and terms;

- the lender’s margin on the mortgage;

- the total expected lender and origination fees;

- whether the mortgage contains a final/balloon payment, and if so, the amount and when it becomes due; and

- the amount of any prepayment penalty the homebuyer will pay if they pay off the mortgage early.

The worksheet is used to compare the terms of either a purchase-assist mortgage or mortgage refinance.

Once complete, the homebuyer and their agent can quickly compare the terms offered by the competing lenders. If the selected lender sticks by their quote at the time of closing, close with that lender. If not, switch to the backup application in process with the other lender.

{kind=link}