Form-of-the-Week:

Guarantee Agreements – For Promissory Note and For Rental or Lease Agreement – Form 439 and 553-1

Lenders and carryback sellers reduce the risks

When a seller carries back a note secured by a first trust deed or an all-inclusive trust deed (AITD) on the property sold, they assume the role of a lender.

All carryback sellers, like lenders, face the risk a buyer will default, no matter how wealthy, conscientious or qualified the buyer might appear to be. On any default in payments on a carryback mortgage, the seller’s sole source of recovery is the mortgaged property, unless the mortgage is subordinated to a construction loan or additionally secured by property other than the property sold (as it then is recourse debt).

Thus, when the seller carries back a note and trust deed on the sale of their property, they need additional protection against the risk of default by the buyer on note payments. This is particularly critical when the buyer makes little to no down payment.

This protection comes in the form of a guarantee, also spelled guaranty, for a third party to pay the carryback debt on a default by the buyer. The question for the seller and the seller’s agent is how to best document the third party’s liability for the buyer’s debt obligation.

The seller has three basic choices for documenting the promise of repayment from someone other than the buyer. Each has different consequences for the seller and the third party.

The seller may ask the third party to:

- become a co-owner of the property with the buyer, and sign both the note and trust deed the seller will receive;

- co-sign the note only, holding no ownership interest in the property sold; or

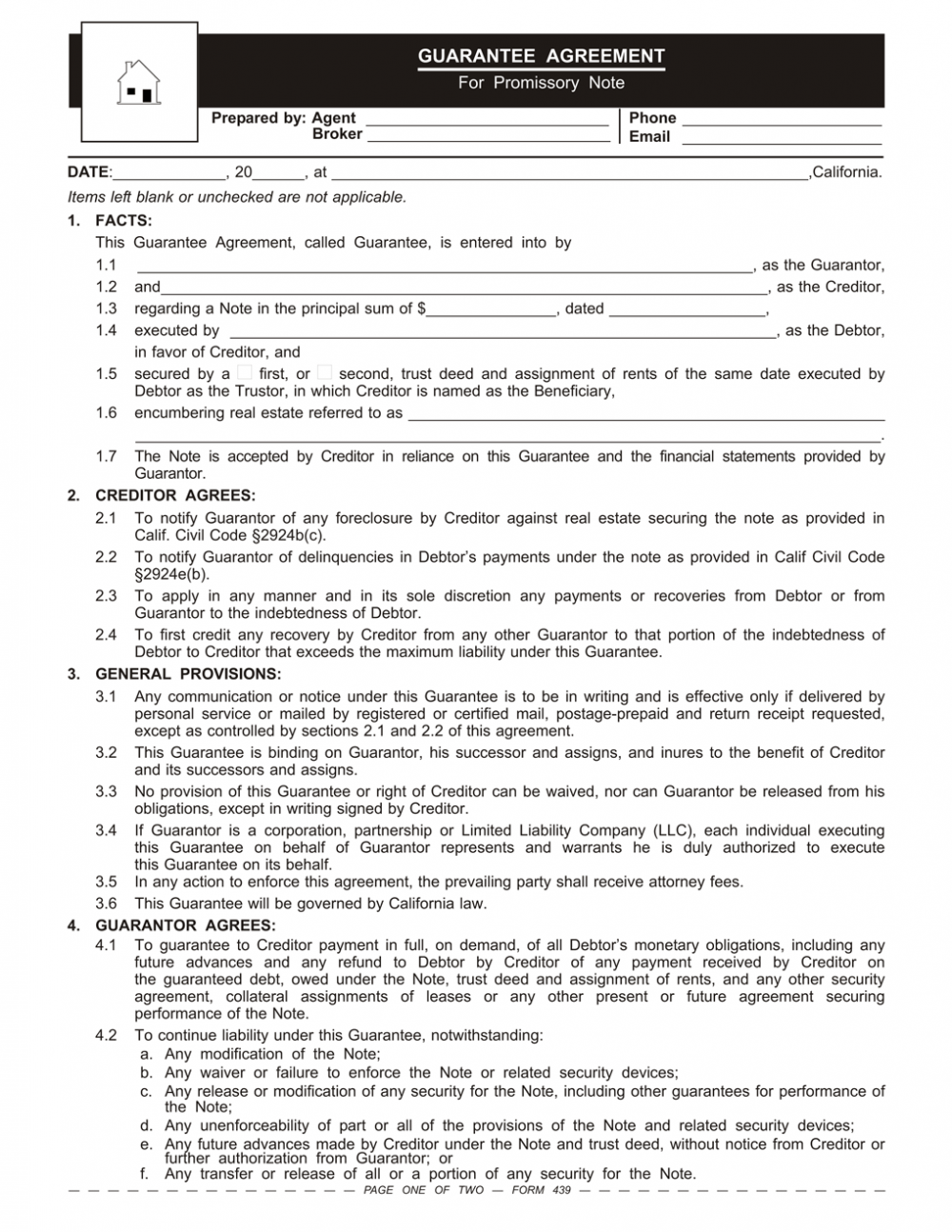

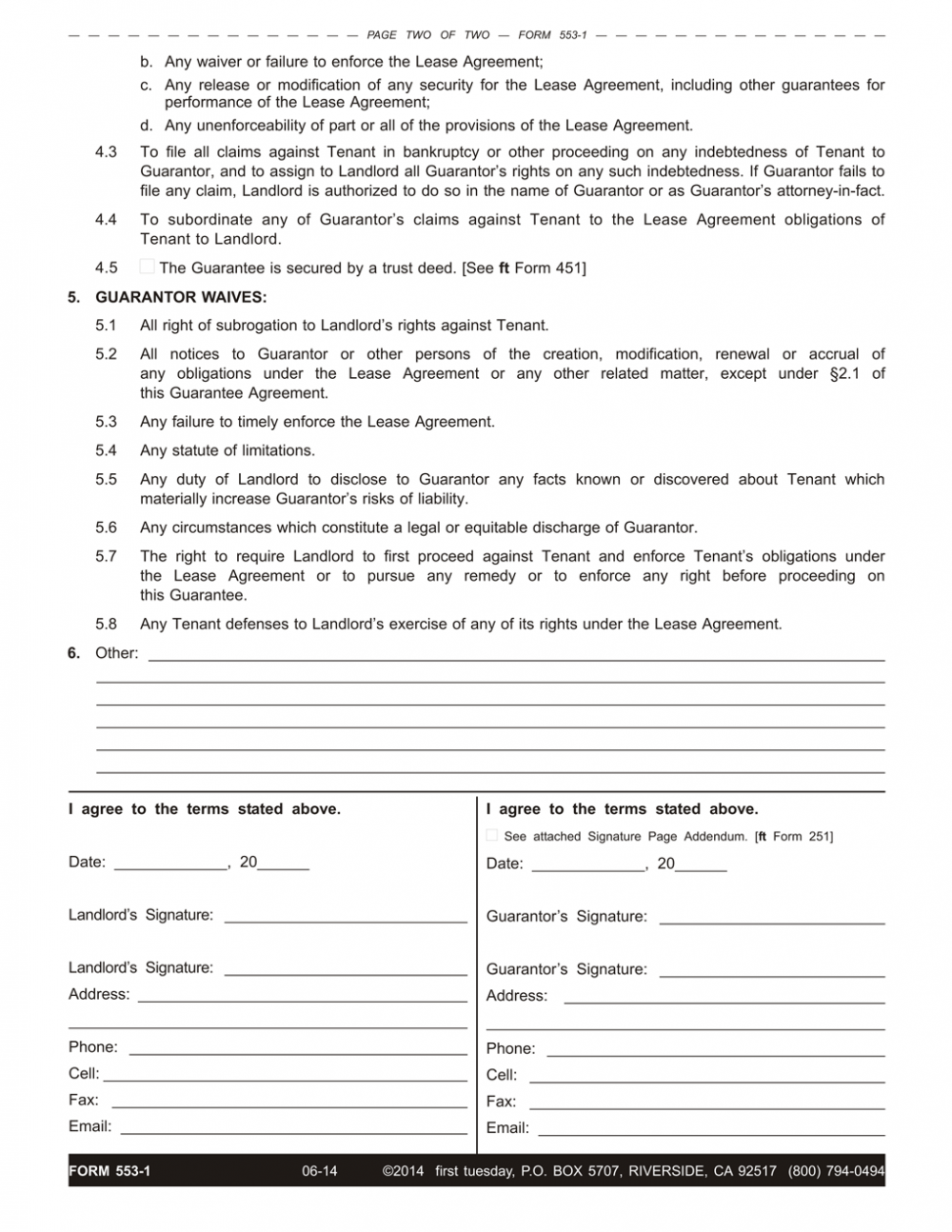

- guarantee the note under a separate agreement with the seller. [See RPI Form 439]

{kind=link}